will conclude its latest meeting at 04:30 GMT Tuesday. Economic developments have been mixed lately, so markets are only pricing in a 20% probability for a rate increase. As for the Australian dollar, the most crucial variable might be the power and scope of China’s stimulus measures, instead of any domestic developments. ){kind=link}

The Reserve Bank of Australia (RBA) will conclude its latest meeting at 04:30 GMT Tuesday. Economic developments have been mixed lately, so markets are only pricing in a 20% probability for a rate increase. As for the Australian dollar, the most crucial variable might be the power and scope of China’s stimulus measures, instead of any domestic developments.

Mixed news

The Australian economy has displayed some mixed signs lately. On the bright side, the labor market is exceptionally tight, with the unemployment rate hovering near its lowest levels in five decades.

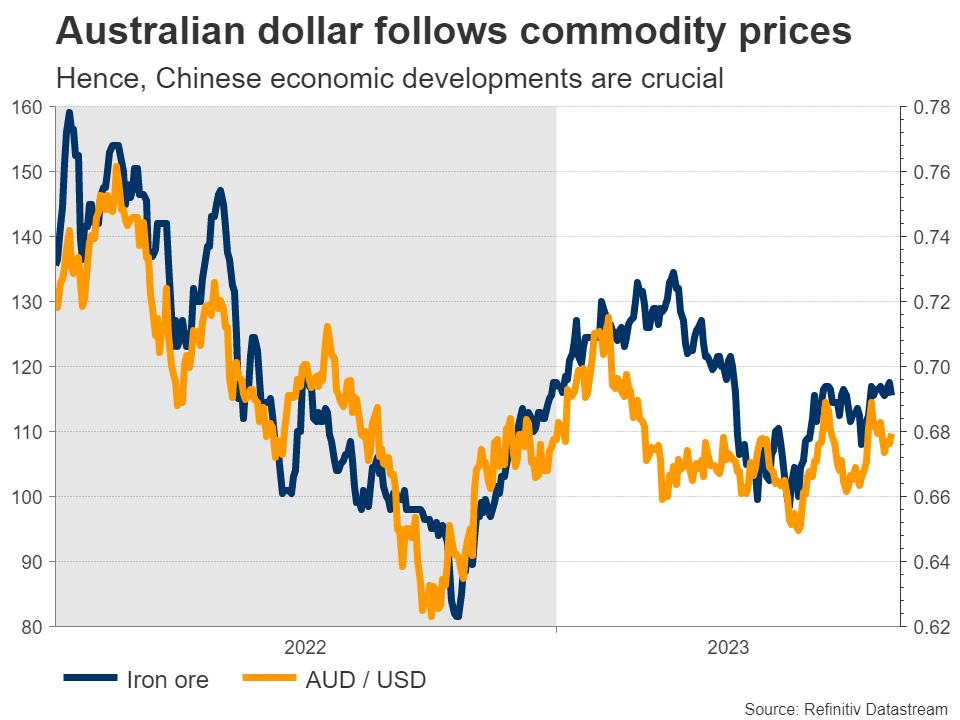

In addition, the prices of commodities that Australia exports have started to recover, encouraged by the promise of new stimulus measures in China, who is the world’s largest consumer of commodities and also Australia’s biggest trading partner.

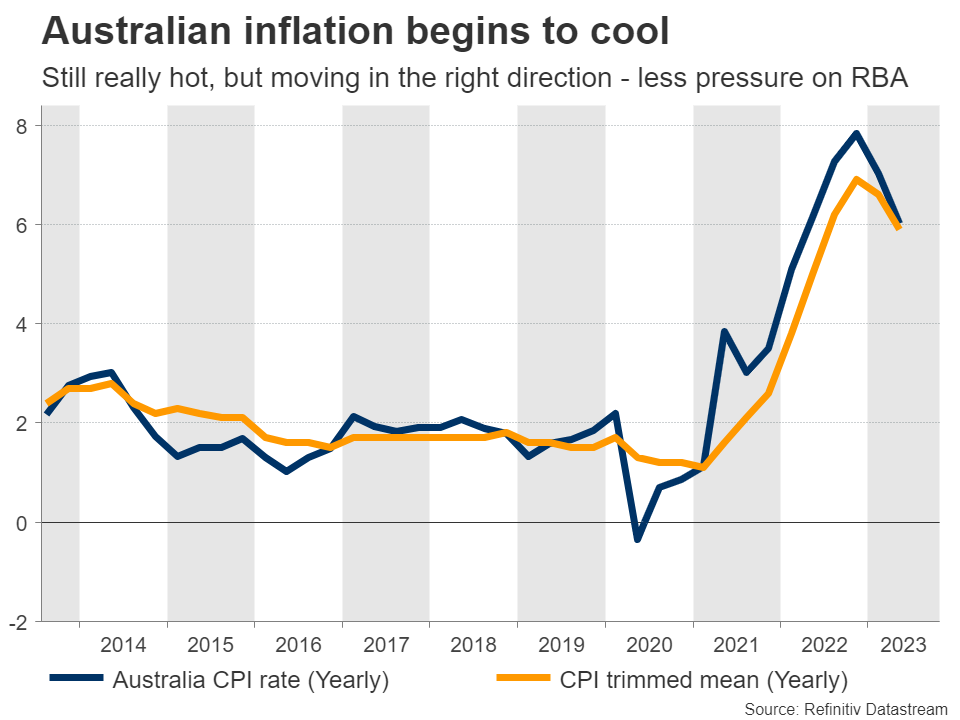

Meanwhile, inflation seems to be cooling down. The CPI rate for the second quarter clocked in at 6%, which is still very elevated but a clear improvement from the 7% in the previous quarter. While services inflation and rents remain extremely hot, those pressures have been partially negated by a sharp cooldown in the prices of goods.

The problem is that business surveys point to a slowdown in economic growth moving forward. In July, the composite PMI fell into contractionary territory – a warning sign that economic activity is losing steam as higher borrowing costs begin to bite consumers.

RBA decision

Turning to the upcoming meeting, market participants think the most likely outcome is that the RBA does not raise interest rates, with the implied probability for no action standing at around 80% and the chance of a rate hike near 20%.

This pricing seems fair. Inflation is cooling off and business sentiment is worsening, so there doesn’t seem to be any real urgency for the RBA to push the rate-hike button again.

Yet, the central bank might strike a relatively hawkish tone, keeping the prospect of future action alive. With the labor market so tight, there’s a concern that wage pressures could intensify, keeping the inflationary fire burning for some time. Similarly, there’s a risk inflation could receive a second wind if China rolls out a strong stimulus package.

Bearing everything in mind, the most sensible strategy might be for the RBA to keep rates unchanged but signal that the tightening cycle is not over yet. Such a combination could inject volatility into the markets.

The initial reaction in the aussie might be negative in case rates are kept unchanged, although any weakness could be short-lived and even reverse if the RBA strikes a hawkish tone.

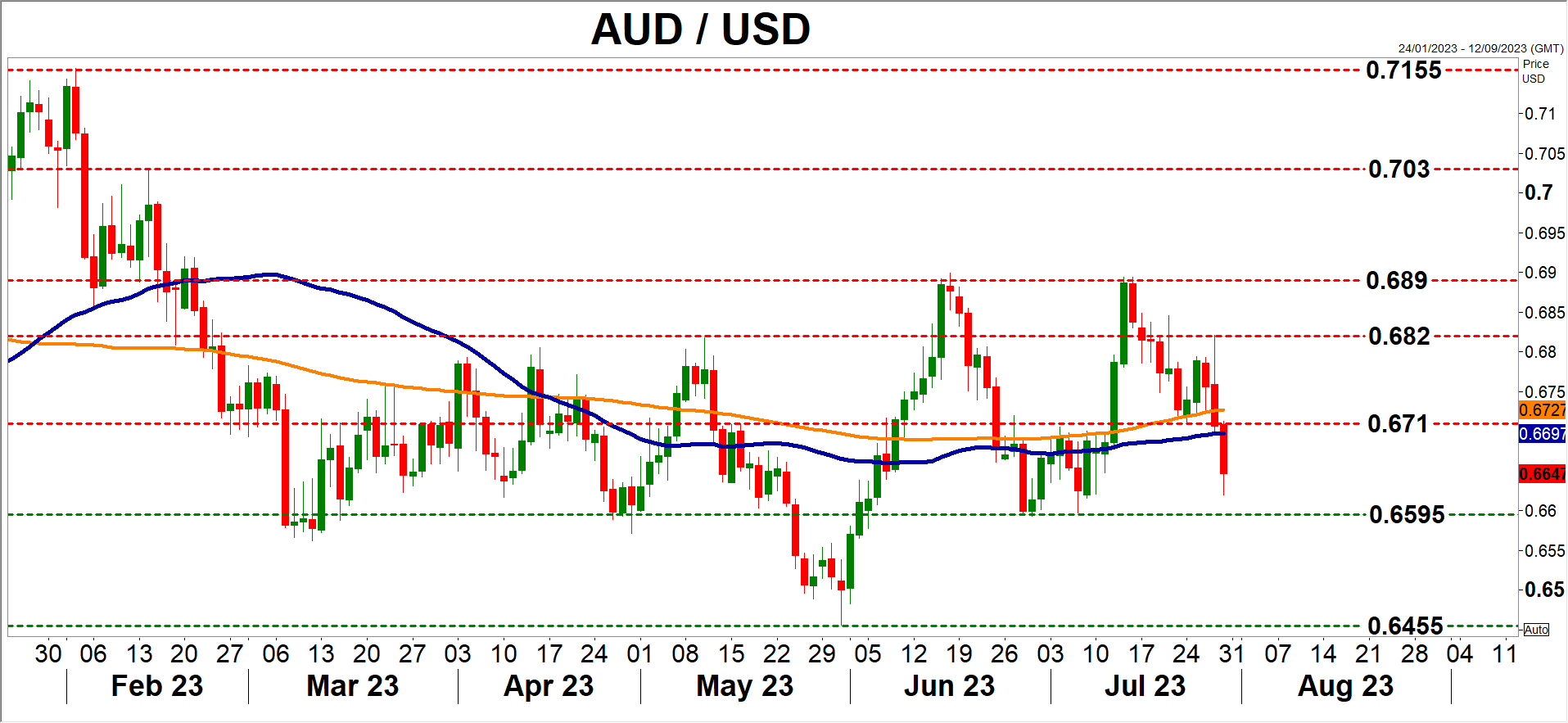

Looking at the charts, the levels in aussie/dollar that could come into play in this scenario are 0.6710 on the upside and 0.6595 on the downside. Overall, the pair has been in a downtrend since early 2021 and it would take a clean break above 0.7160 to change that.

China matters most

In the big picture, the main driver for the aussie might be how the Chinese economy evolves, not what the RBA does. Markets know that the central bank is close to the end of its tightening campaign, even if it raises rates one final time.

On the other hand, there’s a lot of uncertainty surrounding China. Beijing has promised stimulus measures to boost domestic consumption, as the economy struggles with a slowdown in the manufacturing and real estate sectors, but hasn’t announced anything specific yet.

The details and scope of these measures will be extremely important for commodity prices, and by extension, for the commodity-sensitive Australian dollar. A round of powerful stimulus would likely propel the currency higher, but if Chinese authorities underwhelm, the aussie could suffer collateral damage.

Until there is some clarity on this subject, it’s difficult to get too excited about the aussie.