{kind=link}

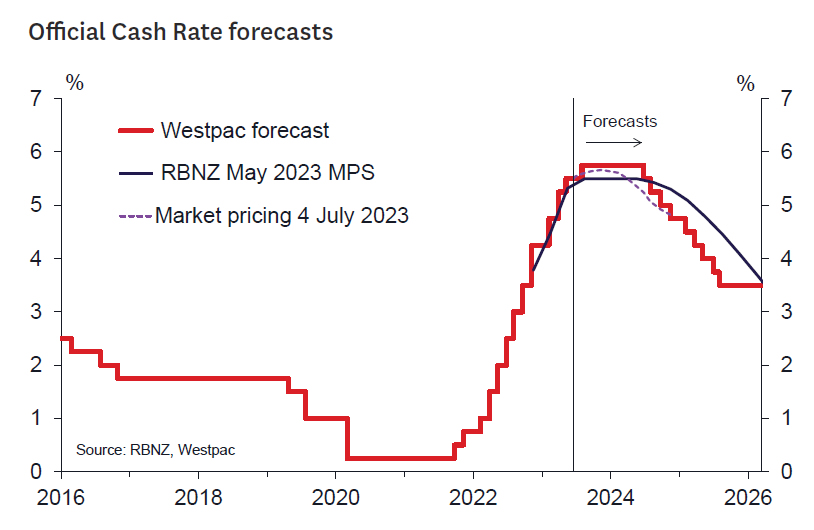

- The Reserve Bank will leave the OCR at 5.50% at its July policy review.

- The RBNZ likely sees recent data as in line with their projected peak in the OCR.

- The accompanying statement should be concise to avoid misinterpretation.

- The RBNZ might take the opportunity to communicate a more data-driven future approach than communicated in the May Monetary Policy Statement.

We expect the Reserve Bank to leave the OCR unchanged at 5.50% at next Wednesday’s monetary policy review. In the May Monetary Policy Statement the RBNZ gave markets a strong steer that it expected that no further increases in the OCR would be required and that now is the time to “watch, worry and wait”. In signalling this ‘end of cycle’ stance, the RBNZ was at pains to emphasize that there was no case to expect any cuts to the OCR for a good while yet. The RBNZ’s forecasts indicated that the first easing in policy would need to wait until late next year.

The data flow since May will likely have given comfort to the RBNZ that its on-hold stance is appropriate – at least for now. The key piece of information was the release of March quarter GDP which came in close to Westpac’s own forecasts but was weaker than the RBNZ’s. Hence from their perspective, the economy started the year in a slightly less overheated position than might have been feared when they produced their May

Statement. Given the RBNZ’s strident on-hold stance this data alone will probably be enough to keep rates unchanged this time around.

Other recent developments paint a mixed picture of the risks for inflation and future interest rates. Some downside risks for domestic inflation and interest rates are accumulating in the form of the weaker than expected bounce back of the Chinese economy, with implications for export demand (reflecting this, in June Westpac revised down its forecast of the farmgate milk price). Many indicators of domestic demand seem consistent with a cooling economy – for example the retail and construction sectors seem to be evolving as one should expect given the interest rate increases that we have already seen. The corporate tax take is also weakening.

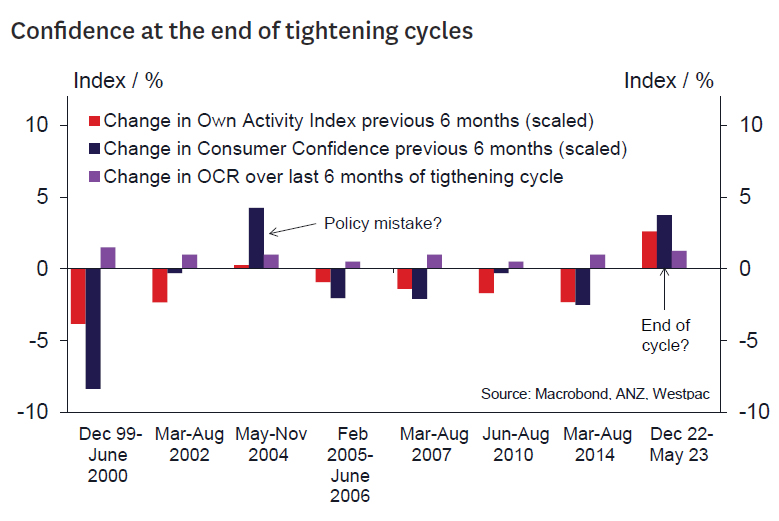

On the other side of the ledger, global central banks are generally finding inflation to be more resilient than anticipated and have upgraded their view of the likely peak in policy rates. The RBNZ will be aware of the risks of repeating the mistake of drawing the tightening cycle to an end too early and having to change tack should the economy and inflation prove more resilient. Some domestic indicators are consistent with lingering economic resilience. In particular, the labour market has not cracked yet – while migration has surged, jobs growth is still outstripping increases in the population. Consumer and business confidence looks to have found a base with the latter seeming quite strong if the top of the tightening cycle is really in place. The housing market has also found a bottom probably somewhat sooner than the RBNZ probably had factored in. Market pricing still reflects a risk of a further increase in the OCR this year (and Westpac retains its call for a 25-point increase in August).

It’s likely the RBNZ’s commentary accompanying the onhold stance will be brief. Saying too much raises the risk of misinterpretation and might lead markets to price in rate cuts or increases that the RBNZ won’t want to endorse right now. The main message we might expect to see is that the future direction of interest rates is data-dependent, so as to to leave room for the RBNZ to shift tack should upside (or downside) risks to the inflation profile accumulate. We think that this “data-dependent” message may have gotten a bit lost in the on-hold messaging at the May Statement.