{kind=link}

Another month has started but the discussion about the BoJ still revolves around the same issues. With the largest central banks globally ready to pause their hiking cycle, can the BoJ map a way out of its ultra-loose monetary policy and finally boost the ailing yen?

What has been happening lately?

As we have been highlighting in recent previews, the BoJ remains in an uncomfortable position. With the largest central banks being very close to completing their rate hiking cycle, the BoJ is still looking for the light at the end of the decade-long tunnel. Its outlook was looking brighter a couple of months ago but, unfortunately for the BoJ, inflationary pressures globally appear to be abating. This was also evident at the recent Tokyo CPI print for May that surprised on the downside. So, how can the BoJ embark on some sort of monetary tightening with inflation on a downwards path?

BoJ Governor Ueda has repeatedly highlighted the fact that the Japanese inflation rise is due to external, cost-push factors. Domestic demand has been playing a secondary, much weaker role, compared to what we have seen in other countries, tying the BoJ’s hands. The way out of the current deadlock is the consumer sector, thus raising the importance of the recent strong, above-inflation wage increases. The BoJ is expecting these increases to have a material impact on consumer spending and consumer sentiment going forward.

Amidst this challenging environment, there is increased nervousness about the BoJ’s next move. The market has gotten used to the ultra-loose monetary stance with the yen being the traditional funding currency for carry trades. Therefore, a change of policy by the BoJ or even adoption of a more hawkish stance is expected to have a stronger impact, especially on the FX markets. The ECB was quite vocal about this possibility at its most recent Financial Stability review. It was also highlighted that a wave of yen repatriation could create an investment gap in the European and US bond markets.

Plethora of data but two releases stand out next week

Understandably, next week’s focus will be on Tuesday’s figures and, to a lesser extent, on Thursday’s releases. The final GDP print for the first quarter of 2023 and the current account figures for April, both released on Thursday, are critical pieces of the economic puzzle, but as described above the focus is squarely on domestic earnings and spending.

The year-on-year change in the labour cash earnings is forecast to moderate even further to 0.5%. If confirmed, this would be the lowest print since February 2022, and a potential signal that the optimism after the recent wage agreements might have been premature. Similarly, the overall household spending data for April is expected to show some improvement but remain in negative territory. A positive set of data figures on Tuesday would be greatly welcomed at the BoJ halls, but probably not by the bond markets.

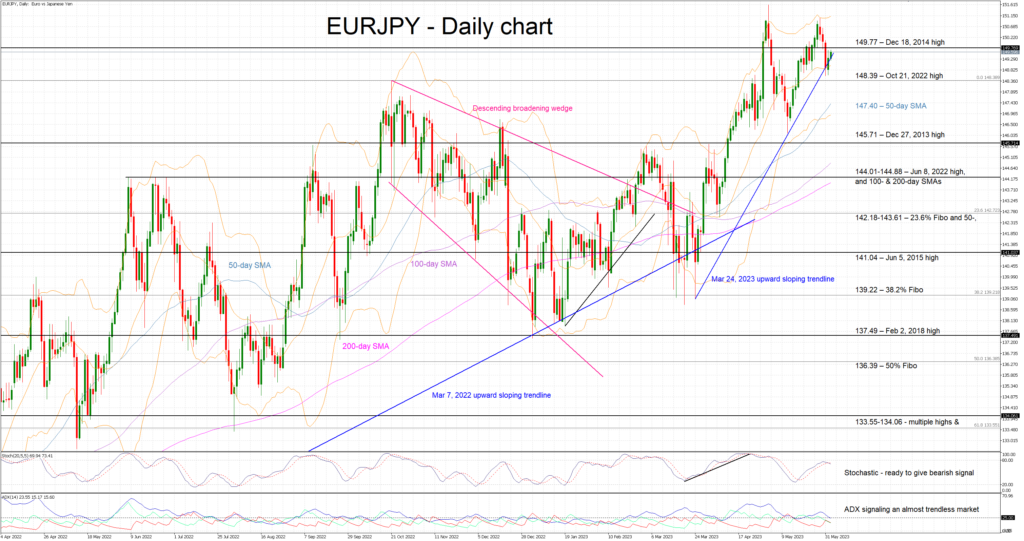

Can the yen finally recover some of its 2023 losses?

The 15-year high at 151.61 in euro/yen appears to have somewhat energized the yen bulls as they have been trying to stop this pair’s advance. Their effort has been fruitless up to now, but the formation of a double top pattern could be the answer to their prayers.

Should the data releases surprise to the upside and sentiment turn in favour of the yen, we would see a retreat towards the 148.39 level and a retest of the 147.22 level. A break of the neckline of the formed pattern at 146.13 could result in an even stronger correction. On the other hand, an upwards break of the 149.77 level could open the door for a higher high, above the recent 151.61.