{kind=link}

The US dollar has been firing on all cylinders lately, capitalizing on bets that the Fed will raise rates one final time this summer. Yet, Fed officials seem split on whether more tightening is needed. This puts more emphasis on the upcoming nonfarm payrolls on Friday. Most signs point to another solid employment report, which could cement expectations of higher-for-longer rates and thereby, add fuel to the dollar’s recovery.

One final hike

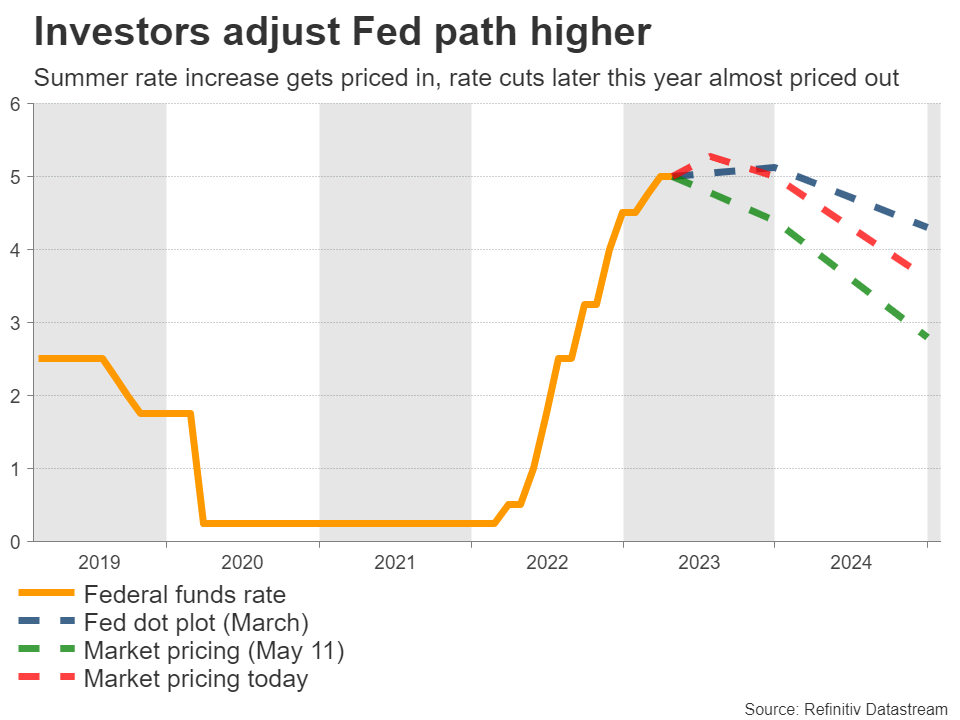

Following a streak of encouraging data releases that highlighted the resilience of the US economy and the persistence of inflationary pressures, there has been a dramatic repricing of the Fed’s interest rate trajectory in recent weeks.

Market participants now assign a 60% probability for the Fed to raise rates again in June, which jumps to 95% for the July meeting. Similarly, the rate cuts that were priced in for the second half of this year have been mostly unwound, as fears of an imminent recession faded.

This repricing has helped to resurrect the dollar. With investors suddenly betting on a higher-for-longer Fed scenario, rate differentials have widened back into the dollar’s benefit. Signs that the European economy is losing steam also played a role, by diminishing the euro’s appeal.

Now the question is whether Fed officials share the view of investors. That’s not clear yet, as some FOMC members have voiced support for ‘pausing’ their tightening cycle. Hence, incoming data will be vital in settling this debate.

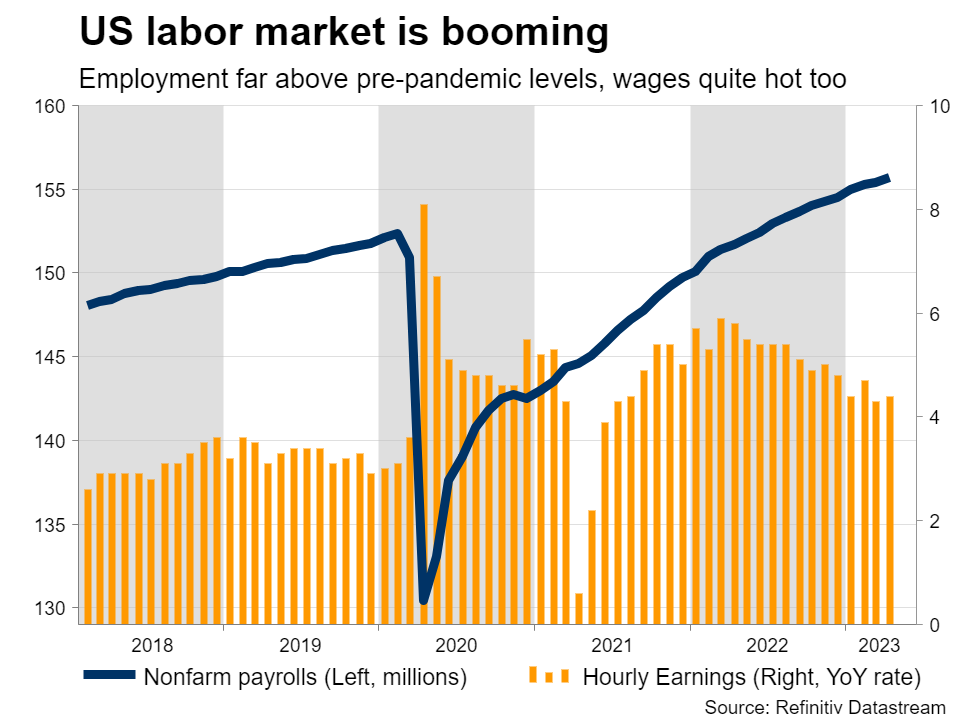

Another solid NFP report?This week, the show will get started on Wednesday with the JOLTS survey, ahead of the ADP jobs report and the ISM manufacturing index on Thursday. But the main event will be on Friday, when the latest employment data hits the markets.

Nonfarm payrolls are expected to have risen by 195k in May, which is a healthy number. The unemployment rate is anticipated to tick up to 3.5%, although that would still leave it very close to five-decade lows. Meanwhile, wage growth is projected unchanged at 4.4% in yearly terms.

It’s crucial to note that nonfarm payrolls have exceeded consensus forecasts 12 times in the last 13 months, as economists seem to consistently underestimate the strength of the US labor market.

Some early signs suggest this pattern could be repeated this time. Business surveys from S&P Global revealed the strongest increase in employment growth for ten months in May, and also highlighted growing salary pressures as workers demanded higher compensation.

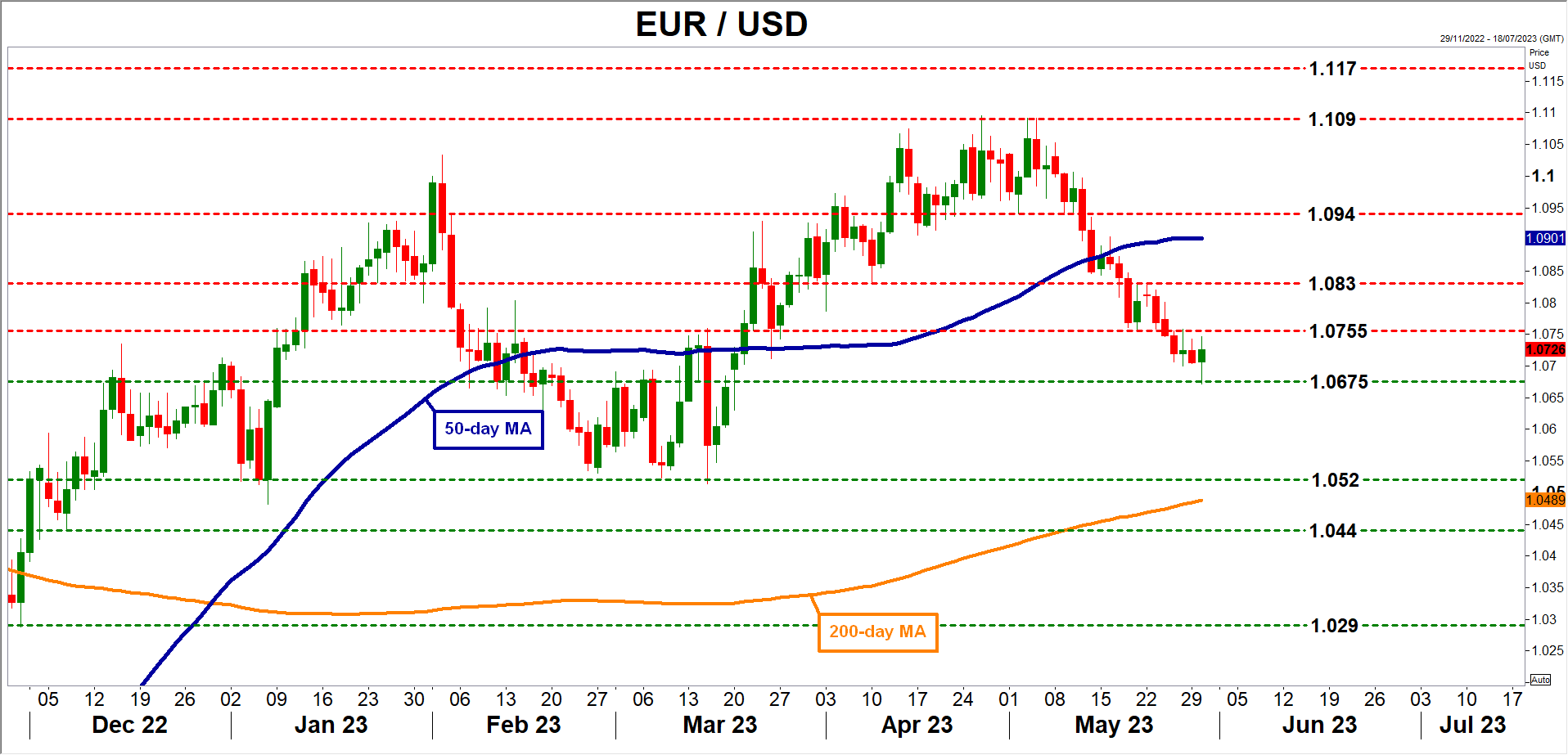

A surprisingly strong report could cement hawkish Fed bets and boost demand for the dollar. Taking a technical look at euro/dollar, the first downside barrier might be the 1.0675 area.

On the flipside, a disappointing report has the capacity to spark a wave of profit-taking in the dollar, propelling euro/dollar higher to challenge the 1.0755 zone again.

More euro/dollar losses?

Looking ahead, in the scenario where US data remains resilient, there is scope for euro/dollar to decline further as traders unwind the surviving rate-cut bets for later this year. In addition, the summer months could be marked by tighter liquidity conditions as the Treasury replenishes its cash buffer, which is another positive force for the greenback.

On the euro side of the equation, with the Eurozone economy slowing down and inflationary pressures finally cooling, market pricing for another 60bps worth of ECB rate increases seems a little unrealistic. If those rate-hike bets are dialed back, the euro could remain under pressure.

From a chart perspective, the ‘line in the sand’ for euro/dollar is the 1.0530 region. A downside violation would mark a lower low on the daily chart, signaling that the longer-term uptrend is no longer in play.