{kind=link}

Summary

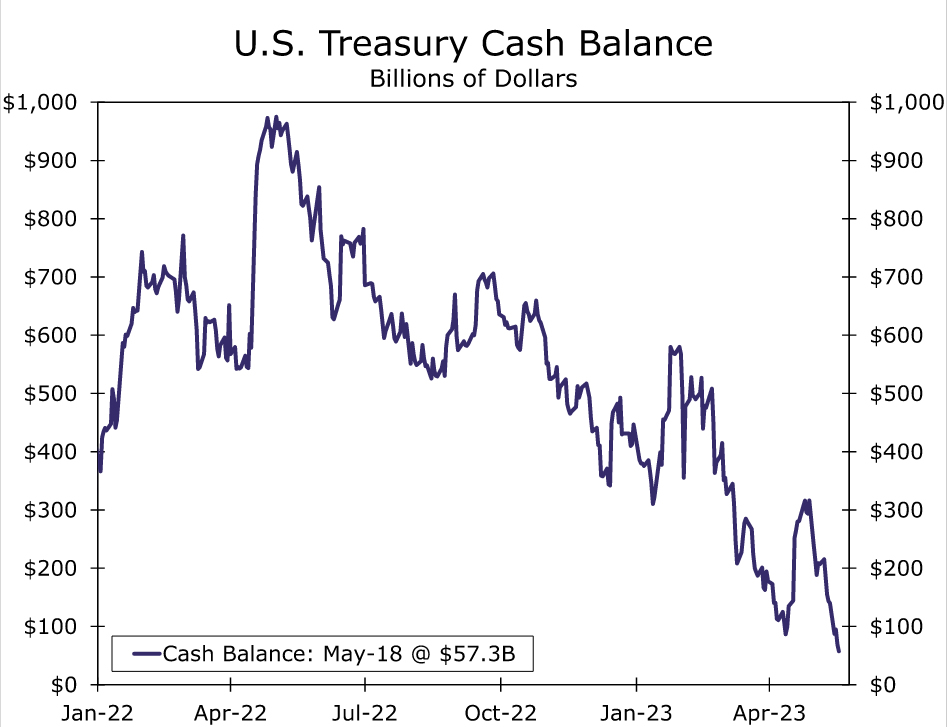

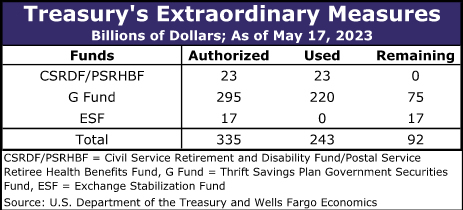

- The debt ceiling drama has reached a fever pitch in recent weeks. As of May 17, the U.S. Treasury had roughly $68 billion of cash on hand and another $92 billion of untapped extraordinary measures. Taken together, Treasury had just $160 billion of additional borrowing capacity remaining under the debt ceiling.

- How long will that borrowing capacity keep the U.S. government afloat? During a May 21 appearance on NBC’s “Meet the Press”, Treasury Secretary Janet Yellen said the odds of reaching June 15 and being able to pay all the government’s bills are “quite low”, while noting there is always uncertainty about future tax receipts and spending.

- Our own internal tracking is a bit more optimistic, but the forecasting misses in recent weeks and months have been towards a greater financing need/bigger budget deficits, which does not inspire much confidence. It has become increasingly clear that, even in the best case scenario, the Treasury’s General Account will be extremely low (<$50 billion) in the first half of June if the debt ceiling is not raised. Put another way, a fifty-fifty chance of an early June default in the absence of a debt ceiling increase is still very concerning and highlights the clear risk of hitting the X date in early June.

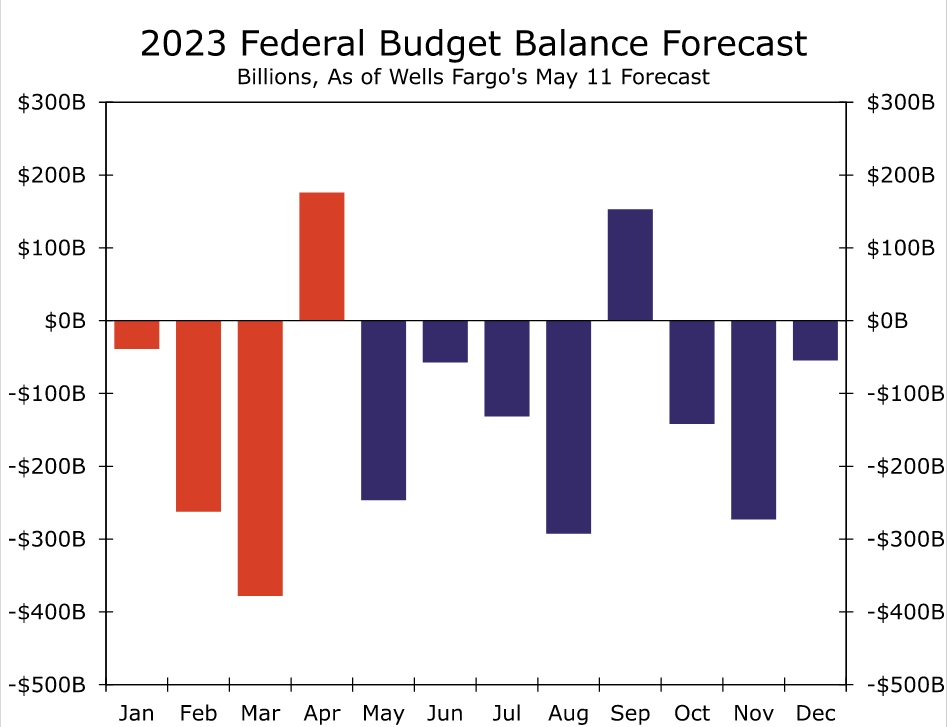

- As we have written previously, if Treasury can manage to stretch its funds to June 15, an infusion of corporate tax revenue and the unlocking of a new extraordinary measure on June 30 would likely keep the U.S. government afloat until the beginning of August.

- While the Treasury’s cash balance and extraordinary measure balances continue to dwindle, lawmakers are attempting to negotiate a deal that would increase or suspend the debt ceiling. So far, negotiations between the two sides have not yielded a deal. This is not to say no progress has been made. But there remain major outstanding questions that still need answers to close a deal.

- So what happens next? In our view, there are three possibilities. First, Republicans in Congress could strike a sweeping deal with President Biden and Democrats in Congress to increase or suspend the debt ceiling for 1-2 years. For a deal to be reached and turned into law before early June, a breakthrough in the negotiations will need to occur this week.

- Another possibility is policymakers agree to a short-term debt ceiling increase that buys more time for negotiations. In this scenario, we envision a debt ceiling suspension for a very short period of time, perhaps one or two months.

- The third possibility is that the standoff continues, and we venture into the early June danger zone with Treasury perilously close to exhausting its borrowing capacity.

- We believe a short-term debt ceiling increase that gives negotiators a bit more time to reach a broader agreement is the most likely outcome, but the situation remains very uncertain and precarious, and we would not be shocked if any of these three possibilities are realized.

- We have continued to field numerous questions about the various contingency plans available to policymakers in the event the debt ceiling X date is breached. Although we are not entirely dismissive of such “break the glass” options, we do not view any of them as painless silver bullets. Ultimately, if any of these numerous plans are adopted, they would be entirely experimental and would come with a litany of legal, technical, economic and political challenges.

Debt Ceiling Crunch Time Draws Near

The debt ceiling drama has reached a fever pitch in recent weeks. The escalating showdown has occurred even though the issue has been coming to a slow boil for months. On January 19, the outstanding debt of the United States government hit its limit of $31.38 trillion. Since then, the U.S. Treasury has been relying on its cash balance and “extraordinary measures” to make up the difference between tax revenues and outlays. However, these two sources of wiggle room have begun to run dry. The Treasury’s General Account (TGA) at the Federal Reserve was down to just $57.3 billion on May 18 (Figure 1). Absent debt ceiling constraints, the TGA would probably be around $600 billion, so a balance of just $57 billion is unusually low. Treasury’s available extraordinary measures amounted to $92 billion as of May 17, the latest data available (Figure 2). When these extraordinary measures are added to the TGA balance on that day, Treasury had just $160 billion of additional borrowing capacity remaining as of May 17.

How long will that remaining borrowing capacity keep the U.S. government afloat? As we have written previously, June 15 is an important date in the timeline. If Treasury can stretch its funds through to June 15, a quarterly deadline for corporate tax payments should bring another revenue infusion of $75 billion or so. That should be enough money to remain solvent for at least another couple of weeks, at which point a new $133 billion one-time extraordinary measure will become available on June 30.1 Our federal budget deficit forecast for July is in the ballpark of $130 billion, and from there it becomes more clear how the X date, or the date on which the Treasury would be unable to meet all of its obligations on time due to the debt limit, could be as far away as the beginning of August (Figure 3).

But getting to June 15 is far from a guarantee. It has become increasingly clear that, even in the best case scenario, the TGA will be extremely low (<$50 billion) in the first half of June if the debt ceiling is not raised. For context, the average daily non-debt cash outflow from the TGA this year has been about $30 billion, and daily withdrawals of more than $50 billion are not uncommon. On May 15, Treasury Secretary Janet Yellen sent another letter to Congressional leaders reiterating that Treasury will likely no longer be able to satisfy all of the government’s obligations if Congress has not acted to raise or suspend the debt limit by early June.2 During a May 21 appearance on NBC’s “Meet the Press”, Yellen said the odds of reaching June 15 and being able to pay all the government’s bills are “quite low”, while noting there’s always uncertainty about future tax receipts and spending. Our own internal tracking is a bit more optimistic, but the forecasting misses in recent weeks and months have been towards a greater financing need/bigger budget deficits, which does not inspire much confidence. Put another way, a fifty-fifty chance of an early June default in the absence of a debt ceiling increase is still very concerning and highlights the clear risk of hitting the X date in early June.

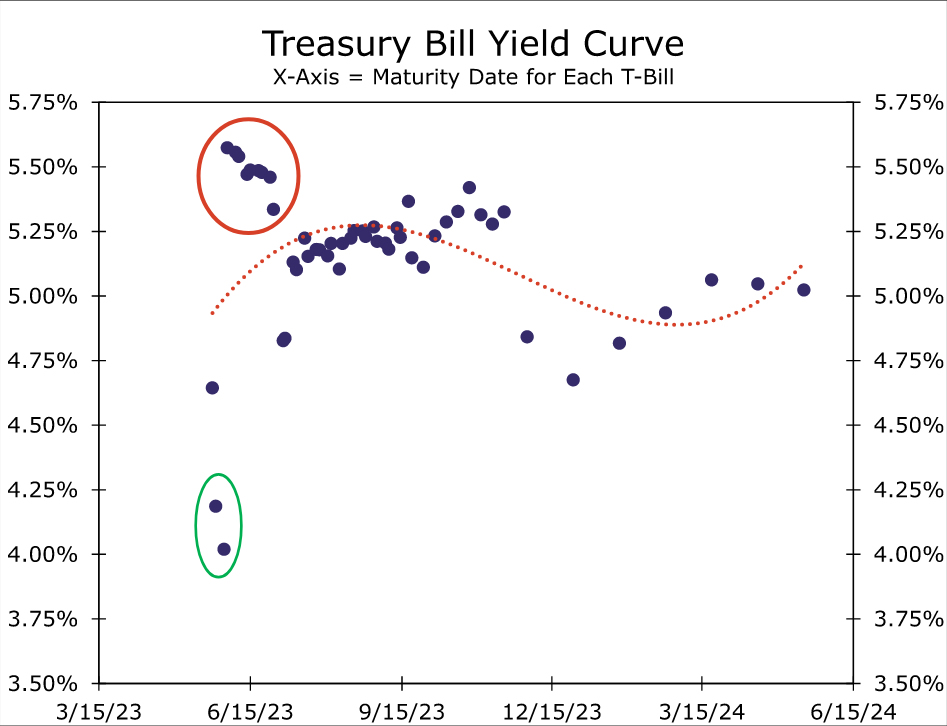

Yields on Treasury bills signal that investors are taking Treasury’s guidance seriously. As we go to print, the yield on the T-bill maturing on May 30 is 4.02%. The yield on the T-bill maturing just two days later on June 1 is a whopping 5.57%, 155 bps higher for two very similar securities with one important difference. Figure 4 illustrates that investors are paying a healthy premium to own bills that mature in May while demanding hefty compensation to hold T-bills that are maturing in the first half of June.

Deal or No Deal?

While the TGA and extraordinary measure balances continue to dwindle, lawmakers are attempting to negotiate a deal that would increase or suspend the debt ceiling. So far, negotiations between the two sides have not yielded a deal. This is not to say no progress has been made. Active negotiations are forward progress relative to the standstill that prevailed for much of the year, and some areas of compromise might be within reach. For example, the two sides appear to be moving closer to rescinding about $50 billion of COVID relief funds that have gone unspent. But there remain major outstanding questions that still need answers to close a deal. Will budget caps on discretionary spending be put in place for just the next one or two years, or will they be implemented for a much longer period of time, such as the next decade? Will the budget caps lead to outright discretionary spending cuts as House Republicans have proposed, a spending freeze, or just slower growth in future outlays? Will lawmakers enact tougher work requirements for some social assistance programs such as Temporary Assistance for Needy Families (TANF) and the Supplement Nutritional Assistance Program (SNAP)? Will energy production permitting reform find its way into the final bill?

The policy disagreements among lawmakers appear wide as we enter crunch time. So what happens next? In our view, there are three possibilities. First, Republicans in Congress could strike a sweeping deal with President Biden and Democrats in Congress to increase or suspend the debt ceiling for 1-2 years. For a deal to be reached and turned into law before early June, a breakthrough in the negotiations will need to occur this week. Another possibility is policymakers agree to a short-term debt ceiling increase that buys more time for negotiations. In this scenario, we envision a debt ceiling suspension for a very short period of time, perhaps one or two months. The third possibility is that the political standoff continues, and we venture into the early June danger zone with Treasury perilously close to exhausting its remaining borrowing capacity. We believe a short-term debt ceiling increase that gives negotiators a bit more time to reach a broader agreement is the most likely outcome, but the situation remains very uncertain and precarious, and we would not be shocked if any of these three possibilities are realized.

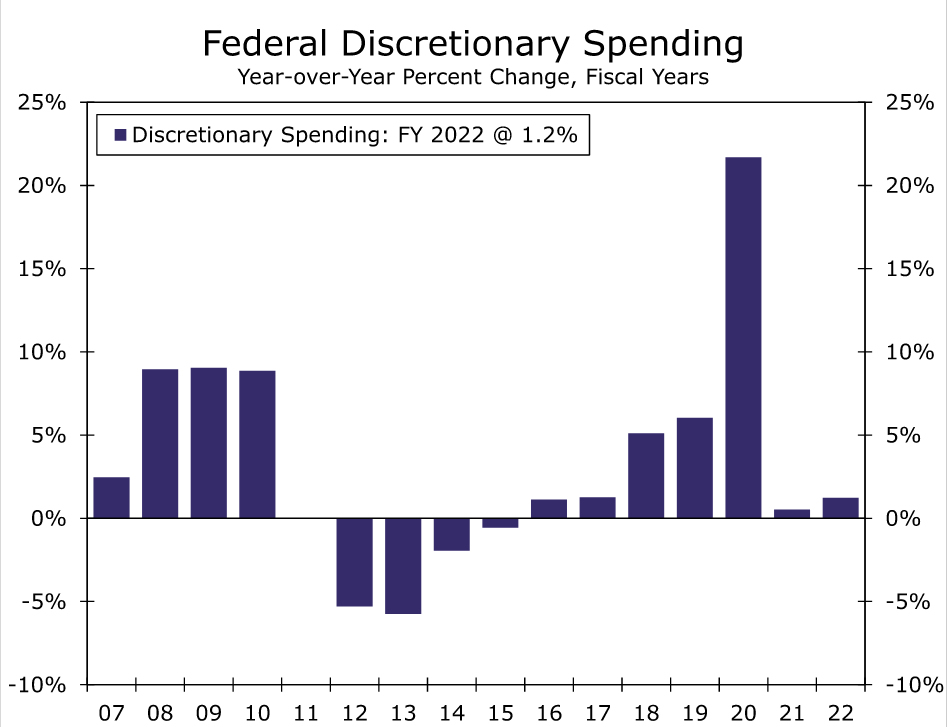

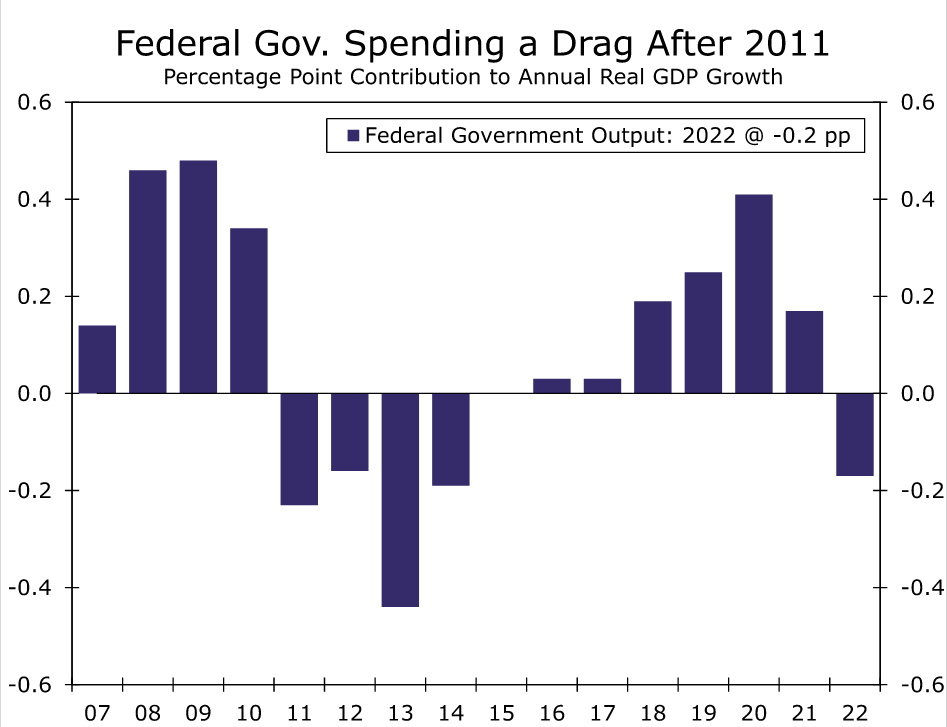

The substance of a debt ceiling deal remains just as fluid as its prospects. We think it is important to keep in mind that any major changes in the fiscal policy outlook could have a material impact on the broader economic outlook. The fiscal austerity that flowed from the 2011 debt ceiling showdown imparted a significant drag on economic growth in the years that followed (Figures 5 and 6). Our baseline economic forecast assumes federal discretionary spending is modestly additive to economic growth in 2024 as most annual appropriations grow roughly with inflation and the 2021 infrastructure bill and other previously-enacted spending boosts continue to flow. However, spending cuts much closer to what was in the House Republican debt limit bill would create downside risk to this forecast. For example, returning total discretionary spending in FY 2024 to FY 2022 levels would amount to roughly a $130 billion spending cut (~0.5% of GDP) relative to the Congressional Budget Office’s baseline. If realized, federal fiscal policy could shift from neutral or somewhat accommodative to restrictive. A pending Supreme Court ruling on President Biden’s student loan forgiveness program also looms in the near future as an important swing factor in the outlook for the federal fiscal policy growth impulse.

Fallback Options, but No Silver Bullet

We have continued to field numerous questions about the various contingency plans available to policymakers in the event the debt ceiling X date is breached. We would encourage our readers to review the debt ceiling guide we published in January, which can be found here, for further reading on Treasury prioritization plans and Federal Reserve options. The Congressional Research Service also has written extensively on various hypothetical escape hatches, such as minting a high denomination platinum coin or invoking the 14th amendment.3

Although we are not entirely dismissive of such “break the glass” options, we do not view any of them as painless silver bullets. Treasury may be able to prioritize principal and interest payments on the national debt, but choosing to pay bondholders would still delay payments due to other recipients of federal spending, such as military salaries, health care providers or Social Security beneficiaries. Furthermore, financial markets may still face serious stress in such a scenario, not caring to differentiate between a de jure or de facto default. The Federal Reserve could attempt to soothe financial markets with repurchase agreements or bond purchases for defaulted securities, but this would still not fix the fundamental problem of not enough tax revenue to cover existing obligations, and transcripts from past debt ceiling showdowns suggest the bar for such FOMC actions would be extremely high.4 Financial system stress could also emerge if markets are forced to await a Supreme Court ruling on unilateral executive action to bypass the debt limit. Ultimately, if any of these numerous plans are adopted, they would be entirely experimental and would come with a litany of legal, technical, economic and political challenges.

Our economic forecast is predicated on the assumption that the debt ceiling is eventually increased or suspended with minimal collateral damage on the real economy. However, past brushes with default have tightened financial conditions, occasionally in a significant way, such as the summer of 2011. The economic impact of a default is highly uncertain since that has never happened previously, but economic modeling suggests the fallout could be quite severe.5 For now, we will continue to monitor developments closely, and we will keep our readers updated on our latest thinking. Stay tuned.

Endnotes

1 U.S. Department of the Treasury. “Description of the Extraordinary Measures” January 19, 2023. (Return)

2 Yellen, Janet. “Debt Limit Letter to Congress Members” U.S. Department of the Treasury. May 15, 2023. (Return)

3 Austin, D. Andrew; Stiff, Sean. “Clearing the Air on the Debt Limit” Congressional Research Service, CRS Report 45011. November 10, 2021. (Return)

4 “Conference Call of the Federal Open Market Committee on August 1, 2011” Federal Reserve. August 8, 2011. (Return)

5 Engen, Eric; Follette, Glenn; Laforte, Jean-Philippe. “Possible Macroeconomic Effects of a Temporary Federal Debt Default” Federal Reserve. October 4, 2013. (Return)