{kind=link}

With the UK banking sector surviving the March developments – a sign of good banking regulations or clever hedging from UK banks – the focus remains squarely on economic developments. Inflation remains a proper thorn in BoE’s side that will become even bigger if this week’s data send the wrong message. Could the pound continue to outperform the euro and other major currencies despite the dovish stance by the BoE?

BoE’s inflation problem

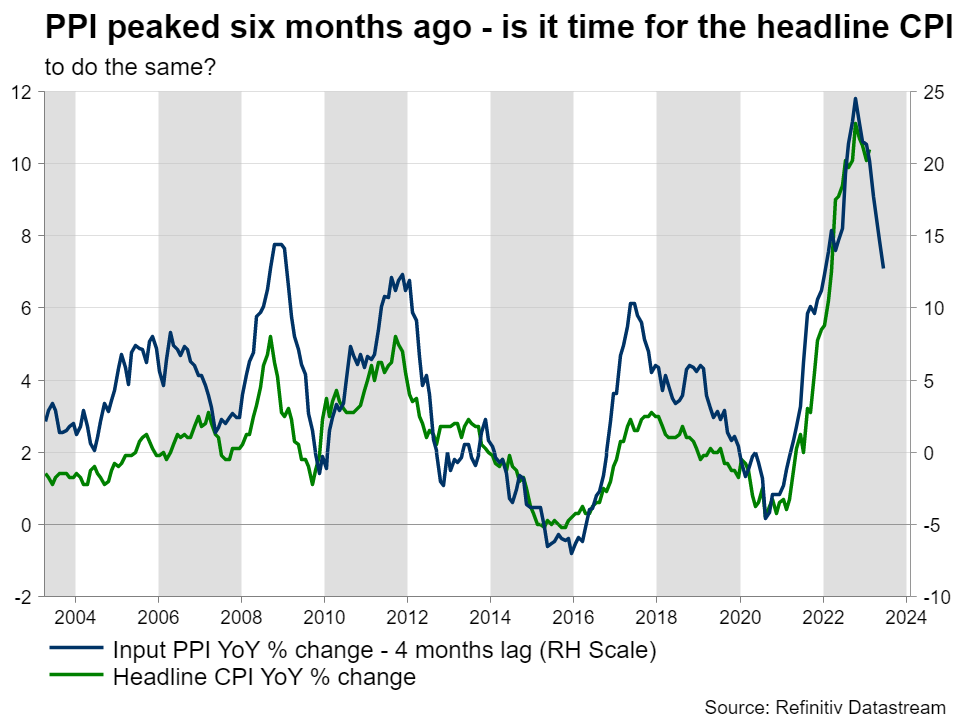

The BoE remains the most intriguing case among the key central banks globally. Despite having the worst inflation rates in the developed world, the BoE maintains its mostly dovish stance. One could argue that the Bank has raised rates by a total of 400 bps in the past 1.5 years, but the data readings are undeniable. February inflation produced an upside surprise and printed again above 10%, even though the rest of the world continues to see a drop in headline inflation rates. We would have expected a plethora of hawkish comments to follow, but the BoE members did not meet our expectations. We understand the reasons behind their reluctance to push rates even higher and instead opting to wait for the already announced monetary policy decisions to impact the real economy. However, here lies a big risk for the BoE. As inflation remains high, it becomes entrenched in wage agreements and the public’s mindset. This creates a vicious cycle that could potentially require further effort and higher rates by the BoE to be untangled.

Production data to give clearer picture about growth in the first quarter of 2023

At the recent testimony by Fed chairman Powell, there was a barrage of questions, mostly from Republican politicians, that the Fed is engineering a slowdown to get inflation in check. While this remains to be seen for the Fed, we have the feeling that this is exactly what the BoE is hoping for. Their wish appears to have come true as the fourth quarter GDP figures showed a barely expanding economy and initial evidence points to an equally weak first quarter of 2023. On Thursday, we will get the February industrial and manufacturing production details. These year-on-year figures have been plateauing at a deeply negative territory, increasing concerns that the targeted slowdown might prove deeper than initially envisaged.

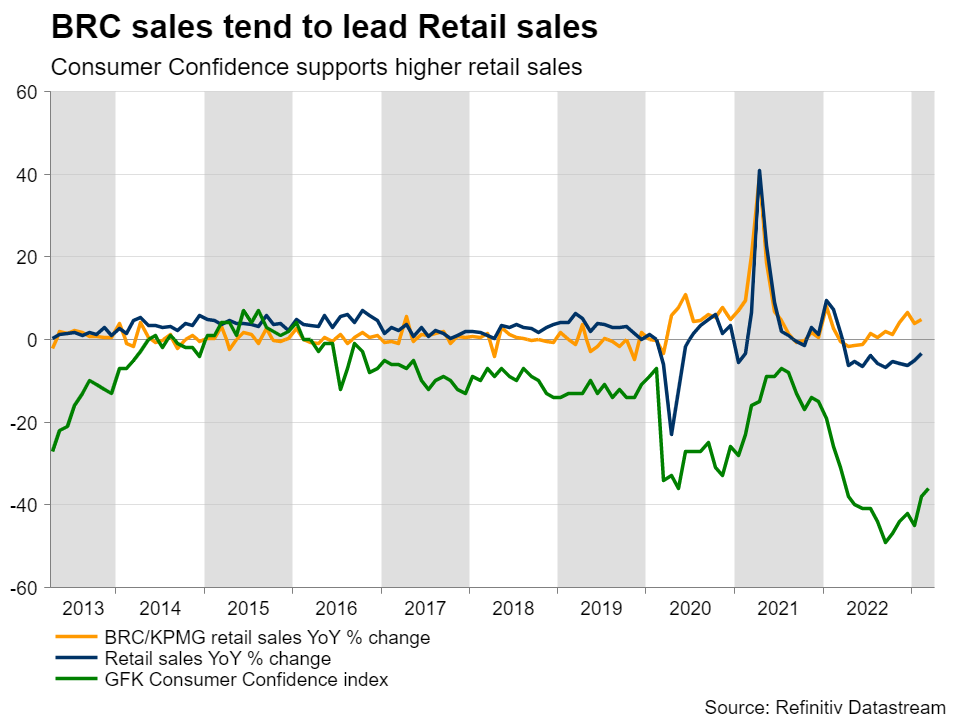

Retail sales keep the BoE on its toes

Retail sales could potentially create another upset for the BoE. The BRC retail sales indicator is released on Tuesday morning and barring a major disappointment, it is expected to confirm that the retail sales figures are on an upwards path. If we add to the mix the decent pace of increase in average earnings, then the BoE is expected to have a hard time affecting consumer appetite or limiting the pricing power by the main retailers, unless it increases interest rates significantly or the economy enters a recession.

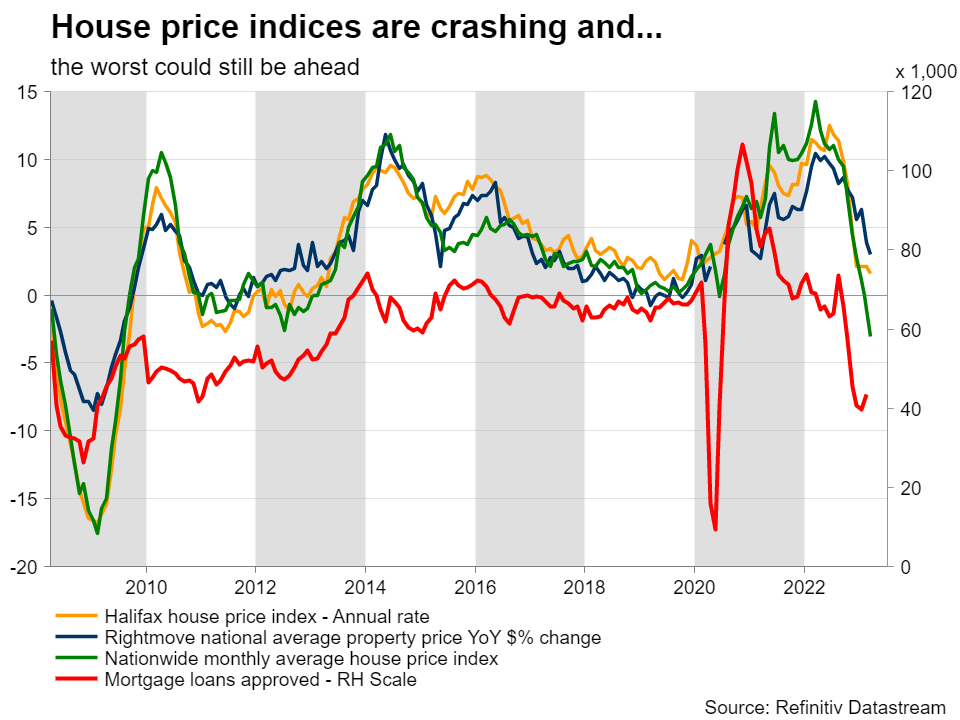

The housing sector matters for the BoE

Central banks have to make decisions for the entire economy, but sometimes certain sectors carry more weight in the decision-making process. For example, the housing sector in the UK is a significant economic factor and a sizeable source of private wealth. As seen in the US, this sector tends to get disproportionately affected by higher interest rates as mortgage lending in the UK has crashed. The RICS house price balance print for March will be published on Thursday and an improvement is forecast. While such an outcome will not necessarily mean that house prices will start to recover, it could be an initial sign that prices are potentially close to the bottom of the current downward move.

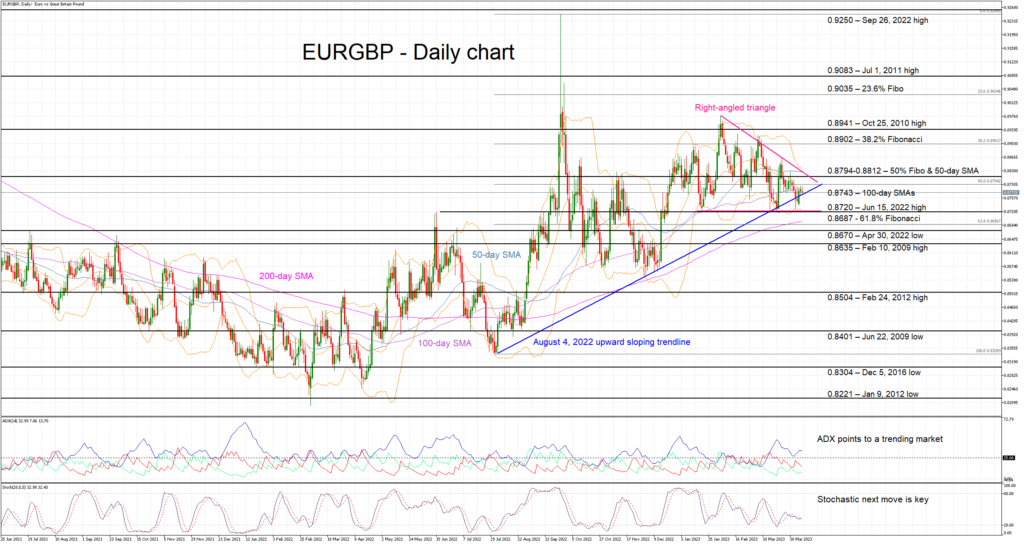

Pound needs a boost

The pound has been the star of the show since the start of the year. It has managed to outperform most major currencies despite the hesitant BoE stance. This outperformance is also significant from an economic standpoint as it reduces imported inflation, but makes UK products and services more expensive internationally, denting even further the weak growth outlook.

The euro/pound pair has been on an upward path since the March 2022 lows, but pound bulls have lately found the courage to stage a small comeback. It has not been a straightforward path as they had to clear some key levels on the way down. The pair is currently fighting with the August 4, 2022 upward sloping trendline and a potential break of this support line could open the door for a move towards the 0.8635 area. Pound bulls could also potentially count on the developing right-angled triangle for further bearish pressure. On the other hand, euro bulls would love a retest of the 0.8900 area provided that they break the 0.8800 midpoint of the recent range.