{kind=link}

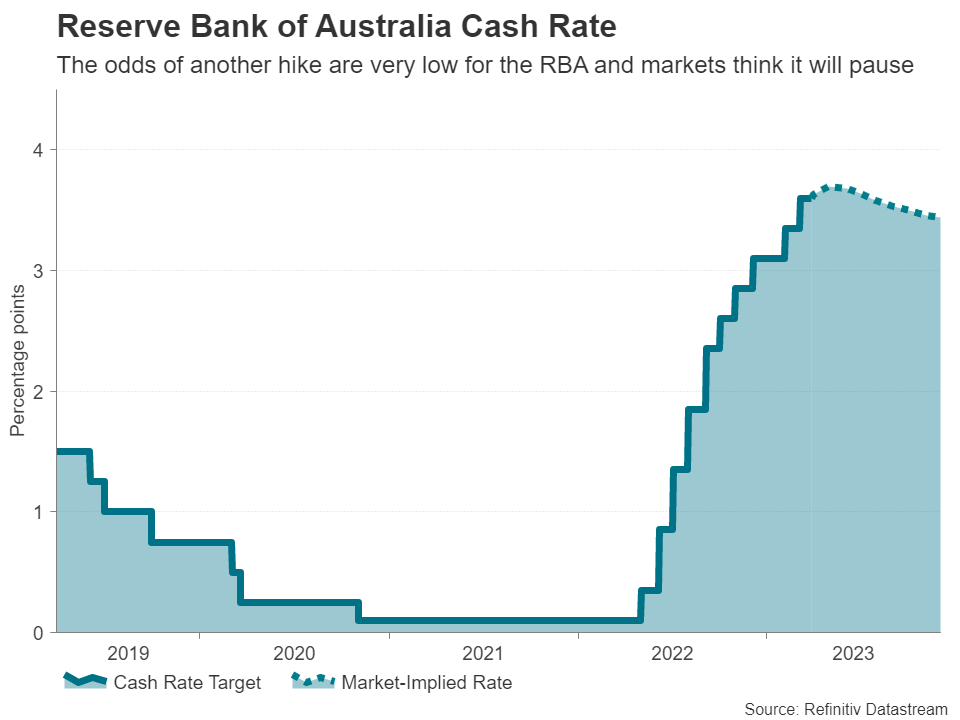

The Reserve Bank of Australia meets on Tuesday to set interest rates and is expected to announce its decision at 4:30 GMT. Investors are anticipating that the central bank will bring to a halt its run of 10 straight meetings of rate increases as inflation finally appears to have peaked and economic growth has lost some momentum lately. A pause would be negative for the Australian dollar, but much will depend on whether the RBA maintains a tightening bias.

No spillover from banking crisis

There’s been little if any direct impact from the banking crisis on Australia’s financial system, and the fallout is not anticipated to be a major headwind for the economy either. Yet, the aussie has suffered some collateral damage as it’s failed to capitalize much on the US dollar’s weakness. The ensuing risk-off sentiment has been one factor that’s been a major drag on the risk-sensitive aussie, but a more significant change since the crisis is that rate hike expectations for central banks globally, not just the Fed, have been sharply scaled back.

For the Australian currency, this is likely having an outsized effect in spite of the economy not being very vulnerable to the turmoil, primarily because the RBA was already on the verge of pausing its tightening cycle. After quite a bit of flip-flopping in recent months, the RBA put a pause back on the table at the March meeting, even before the banking panic began.

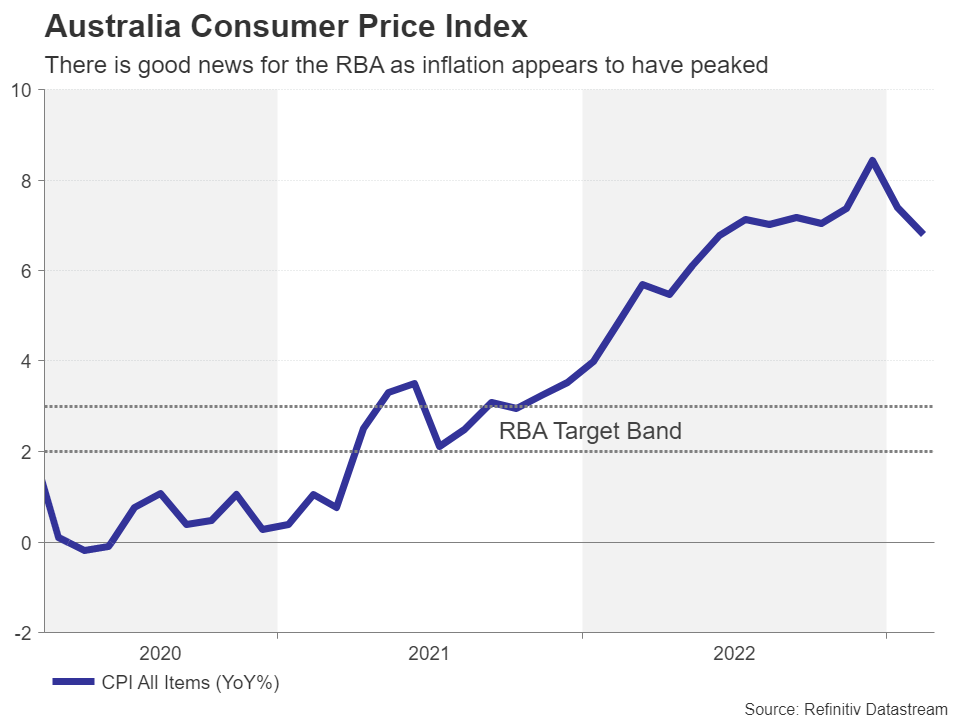

Inflation has probably peaked

Hot inflation data scuppered the RBA’s plans to press the pause button earlier this year. The consumer price index surged by 8.4% year-on-year in December, but price pressures appear to be easing now. The annual CPI rate moderated for the second straight month in February to 6.8%, giving the green light to policymakers to call time on rate hikes.

When adding the uncertainty sparked by the banking crisis into the mix, as well as the RBA being mindful about increasing the burden on households any more than it already has amid cracks in the housing sector, a pause seems almost like a done deal on Tuesday. Moreover, both the manufacturing and services PMIs fell back into contractionary territory in March, raising doubts about the rebound seen at the beginning of the year.

There’s still some juice in the economy

However, the economic picture isn’t quite so simple. The labour market bounced back strongly in February, with the jobless rate edging back down to 3.5%. The outlook for the country’s exports has also brightened following China’s reopening. Most surprisingly of all, some housing indicators point to a modest recovery in house prices being underway.

This then raises the question of what kind of forward guidance will the RBA provide to accompany a potential pause. At the last meeting, the Bank kept its language that “further tightening of monetary policy will be needed” and only hinted that the next hike might not necessarily come in April. However, there was a more explicit signal of a pause a day later in a speech by Governor Philip Lowe.

Will the RBA keep rate hike door open?

It’s very unlikely that the RBA will completely rule out further rate increases in April given that the Australian economy is not quite flirting with recession and the jobs market remains tight. However, how policymakers phrase the language around the likelihood for future tightening is what will matter most for shaping rate hike expectations post the meeting.

Should the Bank keep its guidance about the need for further rate increases over the coming months even if it decides to hold policy unchanged in April, this would be the most hawkish outcome for the aussie. A somewhat less hawkish scenario is if the statement says that some modest tightening “may” be required. However, if the RBA makes a complete dovish pivot and flags that it is likely done raising rates, this could deal a major blow to the aussie.

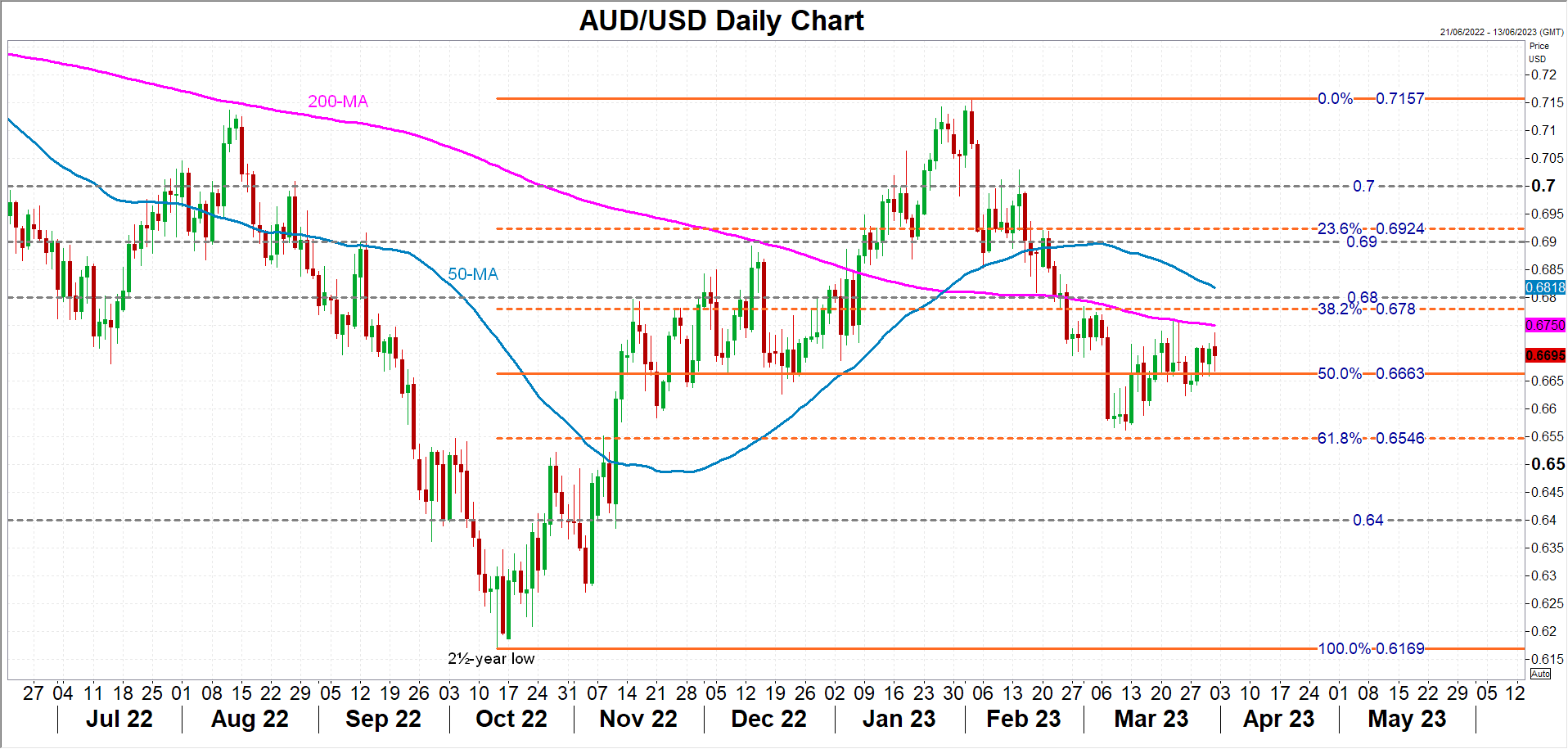

Aussie bulls face a tough battle

The local dollar has already retraced half its gains since February from the October 2022 low versus its US counterpart and faces several major hurdles on the upside. The 200-day moving average, the 38.2% Fibonacci, the $0.68 handle and the 50-day moving average all lie between $0.6750 and $0.6823.

Without a strong enough tightening bias from the RBA, it will be difficult for the aussie to climb back above its moving averages and the February peak of $0.7157 seems increasingly out of reach.

To the downside, a test of the 61.8% Fibonacci of $0.6546 would become almost certain in the event of a clear pause and aussie/dollar could soon be headed for the $0.64 level.

It’s worth bearing in mind, however, that any weakness in the pair could be short-lived if the Fed also decides to go on pause when it meets in May.