{kind=link}

With the rest of the world almost reliving the 2007-08 events, the Japanese developments were mostly under the market radar. This is not atypical, but as we get closer to the Bank of Japan governorship handout the market will start to pay attention to Japanese news. Yen bulls have been enjoying the recent moves, but for the next leg they need concrete economic evidence. Hence, all eyes may be on Friday’s busy calendar with the Tokyo inflation figures being the highlight release.

What has been happening in Japan lately?

As the market got fixated on the banking sector shenanigans that eventually led to the demise of the once-too-big-to-fail Credit Suisse, the Japanese news were treated as non-events. To be fair, the data releases have been on the mixed side and the last BoJ meeting on March 10 proved to be dull. Outgoing governor Kuroda decided to pass the baton to the incoming BoJ chief Ueda without any amendments to the current monetary policy framework or the forward guidance. However, there was very positive news from the Shunto wage negotiations. A number of key firms including Mitsubishi Heavy Industries and Toyota not only fully agreed with the demands of their respective labour unions, but also did so in record time. Honda, for example, completed the negotiations at the fastest time since the 1990s. The end-product up to now has been significant, above inflation, increases in workers’ pay that should be music to the ears of the BoJ members.

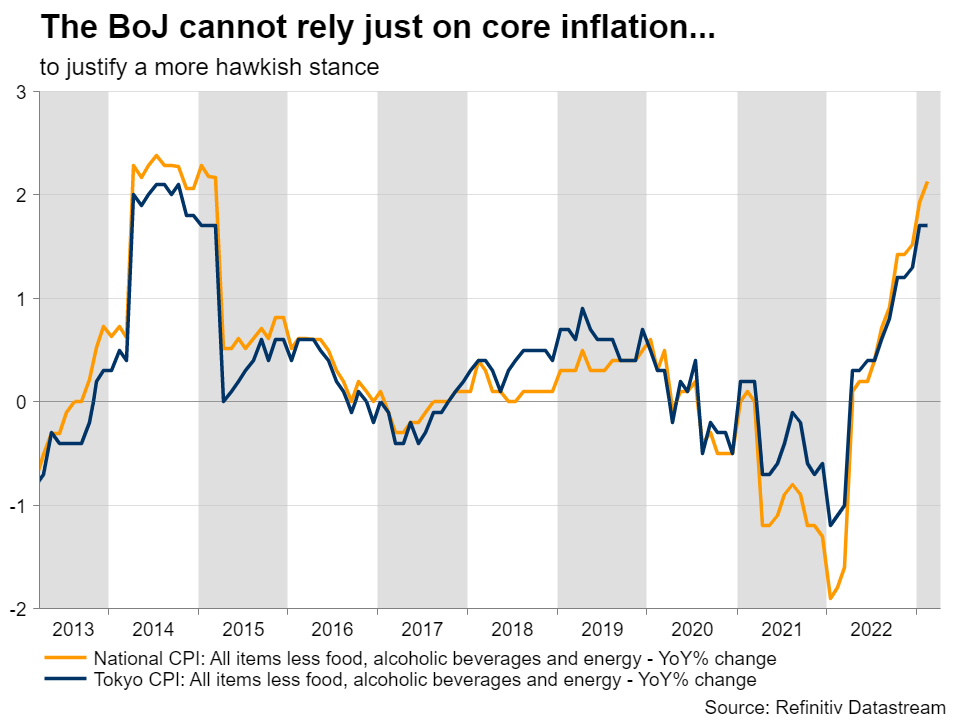

The key point going forward is whether this higher-wages momentum will translate into stronger consumer sentiment. As repeatedly highlighted, Japan has not been plagued by double digit inflation rates seen in other developed countries. However, the headline CPI moved to the highest year-on-year rate since the early 1990s and the core component recorded its strongest yearly increase since early 1980. But apart from the January adjustment at the yield curve control (YCC), the BoJ has not really amended its monetary policy stance, essentially abandoning the yen to foreign market forces.

Tokyo CPI frontrunning the nationwide print

The national CPI print for February showed a full percentage drop in the yearly rate of increase, from 4.3% to 3.3%. While globally we have seen some signs of inflation cooling off, particularly in the US and the euro area, the magnitude of the drop in Japan was clearly not anticipated. Similarly, the core component dropped to a yearly level not seen since September 2022, even though the rest of the world is facing stickier-than-expected-core inflation, and hence complicating the reaction function of the key central banks. On Friday, we get the March Tokyo headline and core CPI figures, an early preview of the current national inflation pressures. The market is looking for further easing in both indicators, which means that inflation is abating. If these forecasts are indeed confirmed, then it would be difficult for the new BoJ leadership to change dramatically the current mixture on monetary policy. The national aggregate inflation print is scheduled for release on April 20, a week before the first BoJ meeting under Ueda.

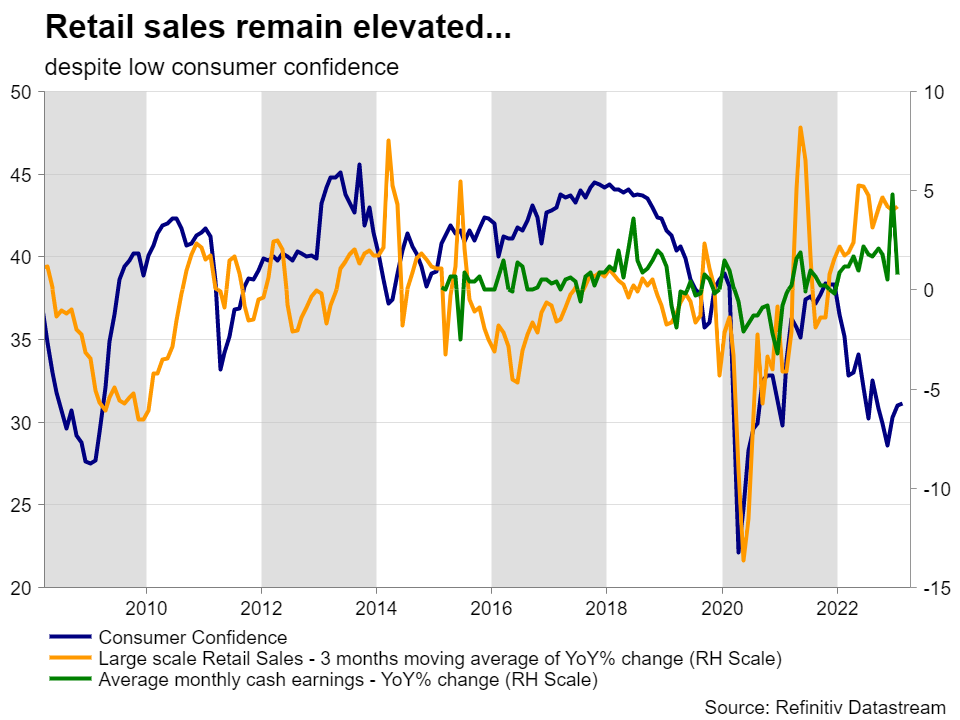

Decent retail sales growth despite low consumer confidence

While the rest of the central banks have been almost exclusively focusing on CPI, the BoJ has been all over the consumer spending data. The ongoing disparity between the retail sales figures and consumer confidence remains significant. While the latter has dropped aggressively and hovers around low levels, retail sales growth remains elevated. This gap is even more evident when analyzing the large-scale retail shops data. Putting aside the volatile nature of the sales dataset, history points to a possible correction in retail sales ahead. However, the recent wage increases agreed should support retail sales going forward, and lead to some degree of correction in the consumer appetite. But this tendency is expected to be seen in next month’s figures, thus raising the possibility for a downside surprise on Friday.

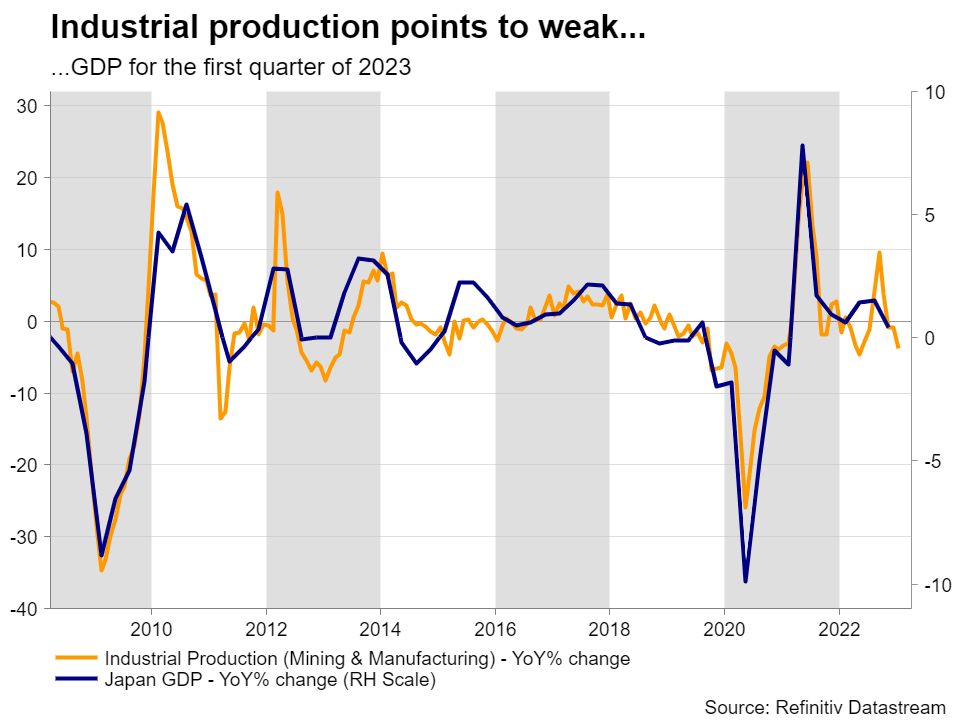

Industrial production raises question about GDP growth

With the final fourth-quarter GDP report disappointing on March 9 and revealing an almost stagnant economy, the market would be looking closely at the preliminary March industrial production data on Friday morning. Up to now, the Q1 figures have been quite disheartening and another negative print means that the market could almost completely write off any hawkish expectations for the next BoJ meetings. In addition, questions will multiply regarding the true extent of the Chinese reopening, and its much-anticipated impact on goods demand and supply lines globally.

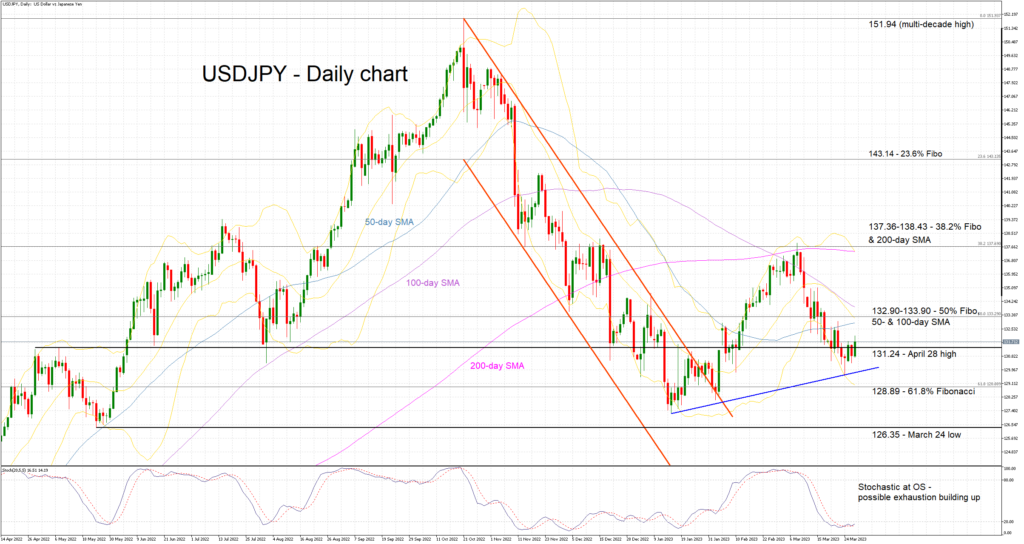

Yen’s fate determined by foreign forces

Yen has been one of the beneficiaries of the banking sector woes. Following a negative 3-month spell, the yen managed to record gains against both the euro and US dollar, a typical reaction in the risk-off sentiment seen earlier in March. As we return to more normal conditions and the market refocuses on the economic outlook, the yen underperformance is likely to resume. However, we are currently in a much different world to the early March situation, and hence yen bears should be satisfied with moderate gains in the dollar/yen pair. The overall technical set-up looks favourable for them as the stochastic is preparing for an upward move, signaling the possible start of another rally. The 132.90-133.90 range is a key area for momentum, and if successfully tackled by the yen bears, an aggressive push towards the early March highs could be possible.