{kind=link}

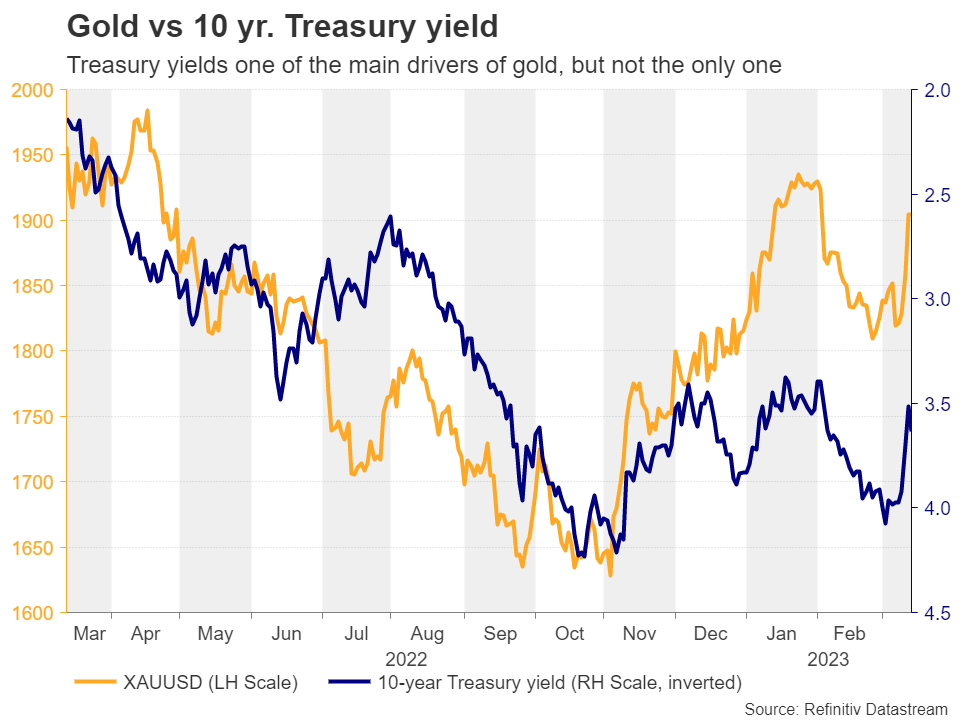

The collapse of the Silicon Valley Bank (SVB) on Friday brought chaos in the markets, with equity indices and government bond yields around the globe coming under strong pressure. This appeared to be the recipe of an elixir potion for gold, which rebounded strongly from near the $1,810 zone and skyrocketed. Is the metal poised to continue flying and what should its traders watch out for?

SVB collapse spreads panic

Markets were thrown into tailspin last Friday and on Monday this week, after a US lender, the Silicon Valley Bank (SVB), collapsed and spread panic among investors. Even after the prompt response of the Fed and the US Treasury to announce contingency plans, investors continued seeking shelter to safe-haven assets, something that allowed gold to shine again.

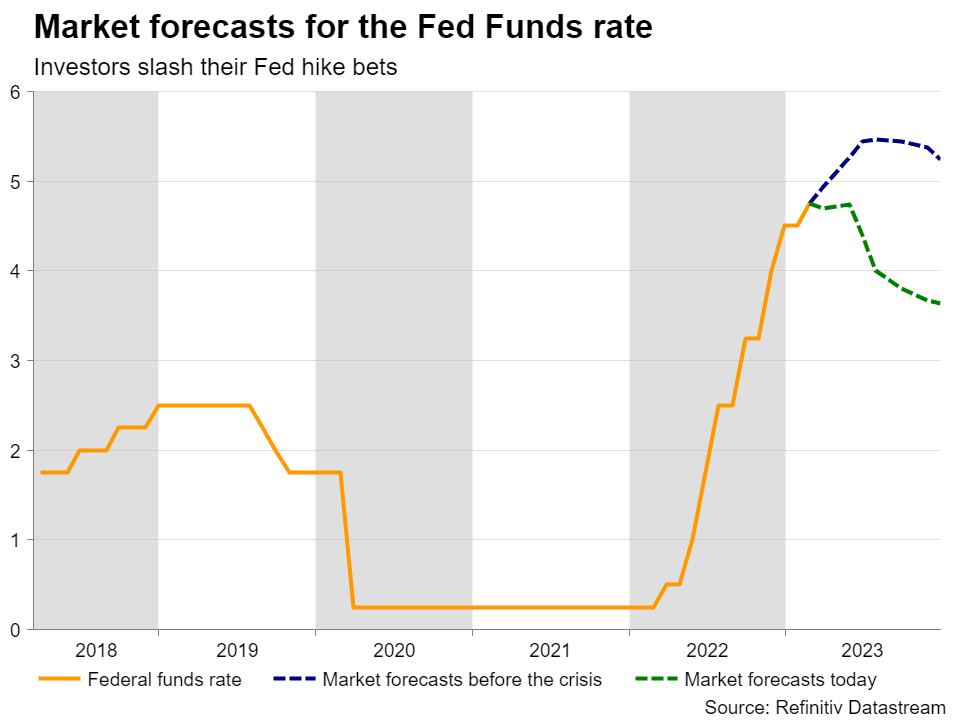

Another beneficiary this flight to safety was the US bond market, something that pushed Treasury yields off the cliff as market participants began scaling back their Fed hike bets in a panicked manner. Jitters eased somehow on Tuesday, but that appeared to be just a calm before another storm, which broke today on headlines that Credit’s Suisse’s largest investors, Saudi National Bank, will stop providing the bank with funds for capital. From expecting a terminal rate of around 5.65% after Fed Chair Powell’s remarks before Congress, investors are now split on whether the Fed will proceed with pressing the hike button next week, and more shockingly, they are seeing interest rates ending 2023 below 4% from their current 4.50-4.75% target range.

All eyes on the Fed

Ergo, at next week’s FOMC gathering, investors will be eager to find out, not only whether policymakers will deliver another quarter-point hike or not, but also how officials’ view and forecasts have been affected by the new crisis. That said, with Powell appearing in a hawkish suit just last week, and data just yesterday showing that underlying inflation accelerated in monthly terms during the month of February, it is very hard to envision that the new dot plot will match the market’s implied rate path and signal so many basis points worth of rate cuts. Therefore, the risks surrounding next week’s meeting may be tilted to the upside.

An outcome less dovish than expected could allow Treasury yields to rise, which may result in a retreat in gold, but one that may not be enough to erase all the SVB related gains, especially if the Fed’s projections are not as high as were expected before the turbulence. On top of that, there are more factors that could keep gold bulls in the game.

Chinese and Indian demand also important

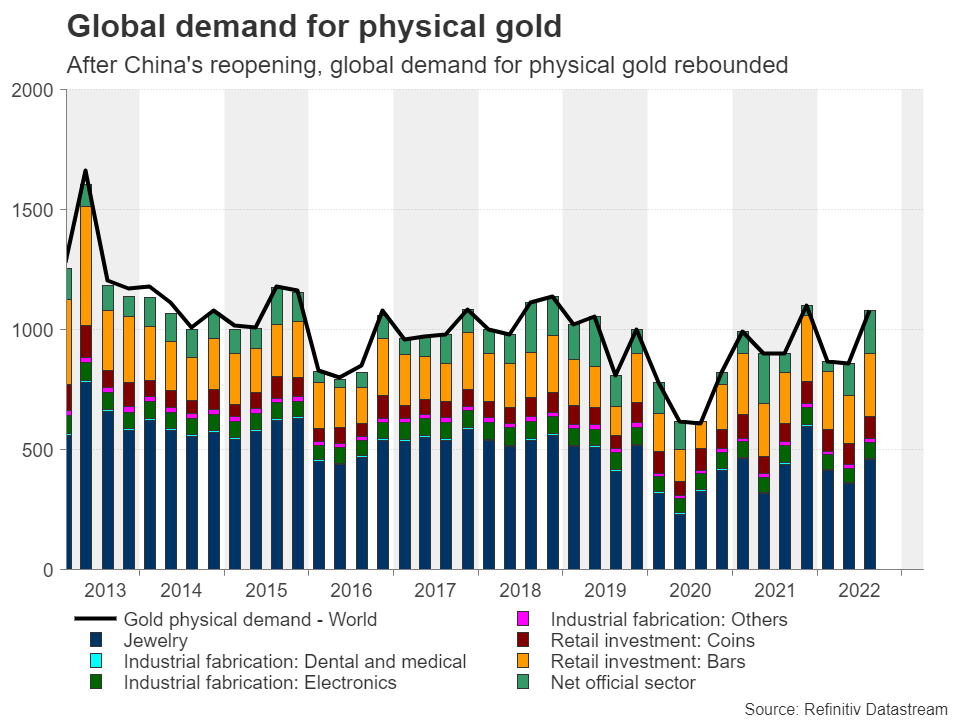

One very important factor may be China’s reopening. Traditionally, China has been the world’s largest consumer of gold, with its jewelry demand falling below that of India during 2022 for the first time since 2011. This suggests that there may be ample room for recovery should the engines of the Chinese economy continue to speed up. Jewelry is the largest component of physical demand for the yellow metal, and thus, a strong boost by Chinese consumers could be of major importance. India is the world’s second largest nation in terms of consumption, seeing economic growth of almost 7% in 2022 and nearly 9% the year before. Thus, if economic activity continues to flourish there as well, demand for gold could substantially increase.

Risks seem tilted to the upside

Putting everything together, it may be very difficult to form a convincing long-term view on gold in such a dynamic environment where sentiment is switching from one extreme to the other within a few hours, but it seems that the risks may be skewed to the upside.

From a technical standpoint, gold emerged above Monday’s peak of $1,915 today, a move that may allow the bulls to put the high of February 2 at $1,960 zone on their radar. If they are strong enough to overcome that zone, they may extend their rally towards the psychological round figure of $2,000, also marked by the peak of March 8, 2022.

On the downside, the move signaling that the bears have stolen all the bulls’ swords may be a clear dip below $1,805, which is currently coinciding with the 200-day EMA. Such a move would confirm a lower low on the bigger timeframes and may see scope for declines all the way down to the low of November 23 at $1,725.

That said, for the bigger picture to turn back bearish, the Fed may need to appear nearly as hawkish as the market was expecting it last week, a scenario that may not be that likely considering that the Fed has pledged to assist in stabilizing the banking sector.