{kind=link}

On Friday, Haruhiko Kuroda will sit at the helm of the Bank of Japan for the last time and investors may be eager to find out whether his exit will be accompanied by fireworks, or whether he will prefer to pass the torch to the incoming Governor untouched. With several officials arguing that there is no immediate need to take additional steps, will this decision prove just a stepping stone for the meetings led by the new Governor Kazuo Ueda?

No rush to take more tightening steps

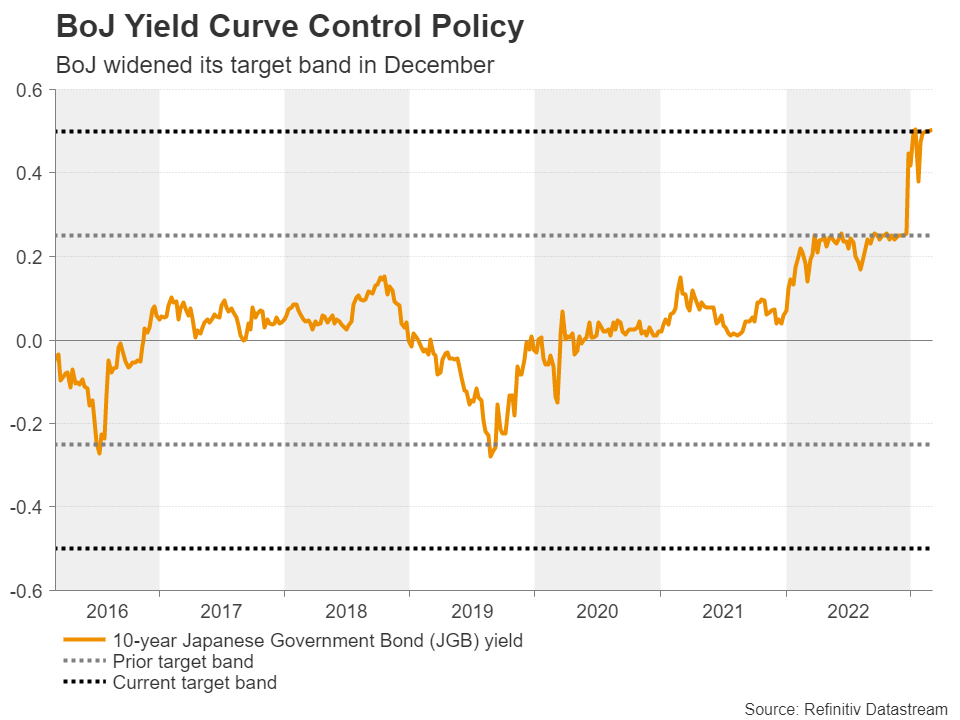

When they last met, BoJ policymakers decided not to further tweak their yield curve control policy, after stunning the financial world in December by widening the target band around the 10-year yield target from ±25 to ±50 basis points around 0%.

Since then, investors have been trying to figure out whether and when the Bank will decide to further remove accommodation, with the nomination of Kazuo Ueda and subsequent comments of his making the picture blurrier instead of clearing it. While he highlighted last year the difficulty of maintaining yield curve control as inflation bites harder, just after his nomination he seemed in no rush to make another step towards ending years of ultra-loose monetary policy, adding that inflation seems mostly fueled by surging import costs of raw materials rather than strong domestic demand. Apart from Ueda, several other, active policymakers also said they see no immediate need to take additional steps.

Inflation and wages slow

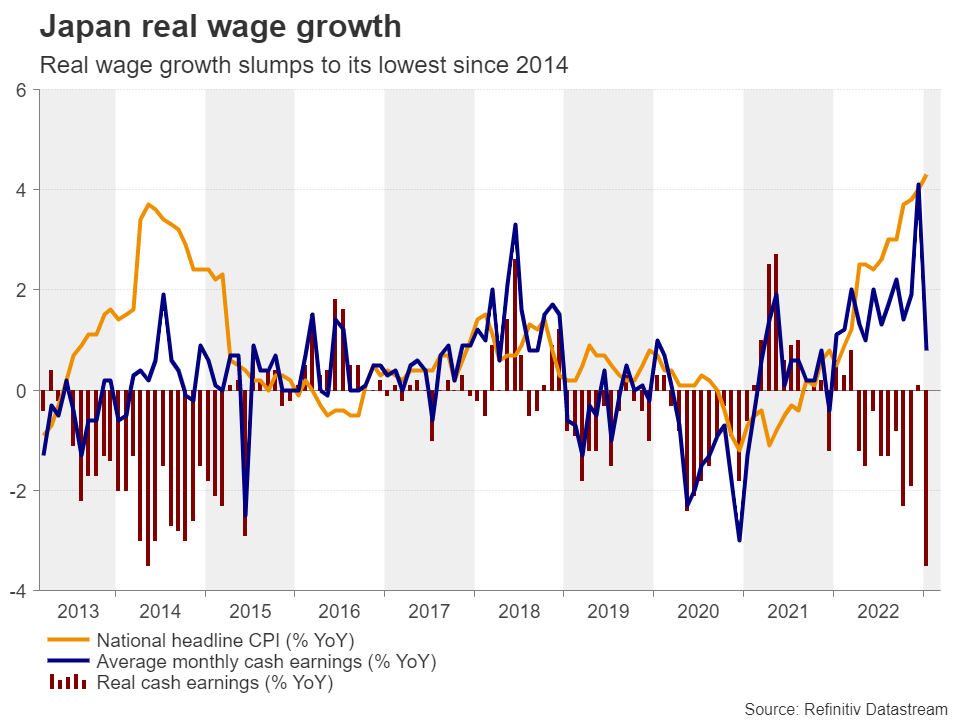

Economic data also support the notion for not taking any action at this week’s gathering. Yes, wage growth surged to above 4% in December, exceeding inflation and thereby resulting in positive real wage growth for the first time since March 2022, but just on Tuesday, data showed that Japan’s cash earnings for January slumped to 0.8% y/y from 4.1%, taking the real growth rate to the lowest since May 2014. What’s more, last week, the more forward-looking Tokyo headline CPI for February slowed by a whole percentage point, while the excluding food and energy rate just ticked up 1.8% y/y from 1.7%, which is still below the BoJ’s 2% objective. What also adds credence to choosing patience for now is the fact that the “shunto” wage negotiations have yet to conclude.

Having said all that though, even if there is ample reason for Kuroda to step down silently, the BoJ’s quarterly survey for the bond market showed that that an index measuring the degree of the market’s functioning slipped to a new record low in February, which means that the widening of the yield band by 0.25bps in December has failed to reduce market distortions. This may have allowed some participants to increase their bets that officials could eventually decide to raise the yield cap at this meeting.

How can the yen react?

Therefore, if the Bank decides to wait for a while longer before taking further steps towards normalization, those expecting action at this gathering will become disappointed and the yen could slip. However, it may be too early to chuck up the sponge on the yen. Despite not being in a rush, officials have repeatedly signaled that they stand ready to adjust policy when deemed necessary, with Ueda saying that he already has ideas on how the central bank could exit its massively stimulative policy. Therefore, it may be a matter of time before policymakers decide to further remove accommodation. For the yen to stay pressured for long, the BoJ may need to maintain a dovish stance beyond April, when other major central banks like the Fed and the ECB continue to raise interest rates to higher-than-previously-estimated levels.

Dollar/yen seems poised to climb higher

From a technical standpoint, dollar/yen has been trading in a consolidative manner since February 27, staying slightly above both the 50- and 200-day exponential moving averages and the key support zone of 134.50. In the bigger picture, the pair is trading well above the prior downtrend line drawn from the high of October 21, as well as above a newly born uptrend line taken from the low of January 16. This keeps the short-term bias positive for now.

If indeed the BoJ refrains from acting on Friday, dollar/yen could emerge above the 138.15 barrier, marked by the high of December 15, and perhaps travel towards the 142.25 zone, defined as resistance by the highs of November 21 and 22. If the bulls don’t stop there either, they may then climb to the 146.65 territory, which provided support between October 24 and November 8.

On the downside, the move signaling that the bears are staging a comeback may be a dip below the round number of 130.00. Such a move may also confirm the break below the short-term uptrend line and may initially pave the way towards the 127.20 barrier, marked by the low of January 16. Should that territory fail to hold, its break would confirm a lower low on bigger timeframes and perhaps pave the way towards the 121.25 zone, marked by the lows of March 30 and 31, 2022.