{kind=link}

Next week’s GDP report will likely show output up a modest 1.5% (annualized) in the final quarter of 2022—just half the average pace of the first three quarters of last year. Some positive signs remained: higher retail and food services sales are pointing to an uptick in consumer spending following a 1% decline in the third quarter. But we expect another large drop in residential investment in the fourth quarter as housing markets continue to retrench. Meantime, a drop in equipment imports is pointing to another quarterly decline in business investment.

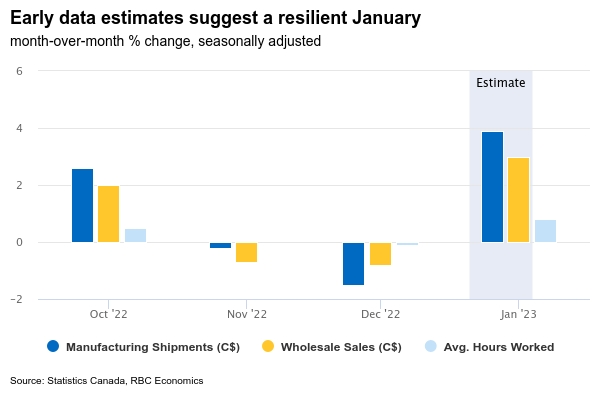

Growth likely slowed into the end of the fourth quarter. Our own RBC cardholder data shows spending plateauing in the back half of 2022, as consumers started to feel the pinch of high inflation and the Bank of Canada’s interest rate hikes dug in. Statistics Canada’s advance estimate of December output was “essentially unchanged.” Still, that is in part due to another pull-back in non-conventional oil production that is likely more due to temporary production disruptions at some of the larger oil production facilities in Alberta (these will reverse as production resumes.) And early data is pointing to a likely sizable bounce-back in January GDP. A surge in employment in January pushed hours worked up 0.8% from December and advance estimates for manufacturing and wholesale trade jumped by 3.9% and 3.0%, respectively.

Nevertheless, the lagged impact of record interest rate hikes (+425 basis points in less than a year) will continue to elevate household debt payments over the first half of 2023—cutting into consumer demand. As a result, though early economic data in 2023 has been better than feared, the most likely base-case remains at least a mild recession starting in the first half of the year.

Week ahead data watch

The annual Business CAPEX intentions survey is expected to show weaker investment plans in 2023. This was reflected in the Bank of Canada’s Business Outlook Survey (BOS) which showed 80% of firms had either lower or static investment intentions in 2023. Still structural labour shortages are expected to persist beyond the near-term. That could prompt businesses to cut investment less than typically might be the case in an economic downturn.