{kind=link}

Following a relatively busy week, the calendar becomes lighter next week. However, that doesn’t mean there are no important economic releases on the agenda. On the contrary, with market participants trying to figure out how many more rate hikes the US economy can withstand, they may pay extra attention to the ISM PMIs for February. Also, with most ECB policymakers arguing that more 50bps worth of rate hikes are needed to tame inflation, the Eurozone’s preliminary CPI numbers for February will likely take center stage as well.

ISM PMIs the dollar’s next test

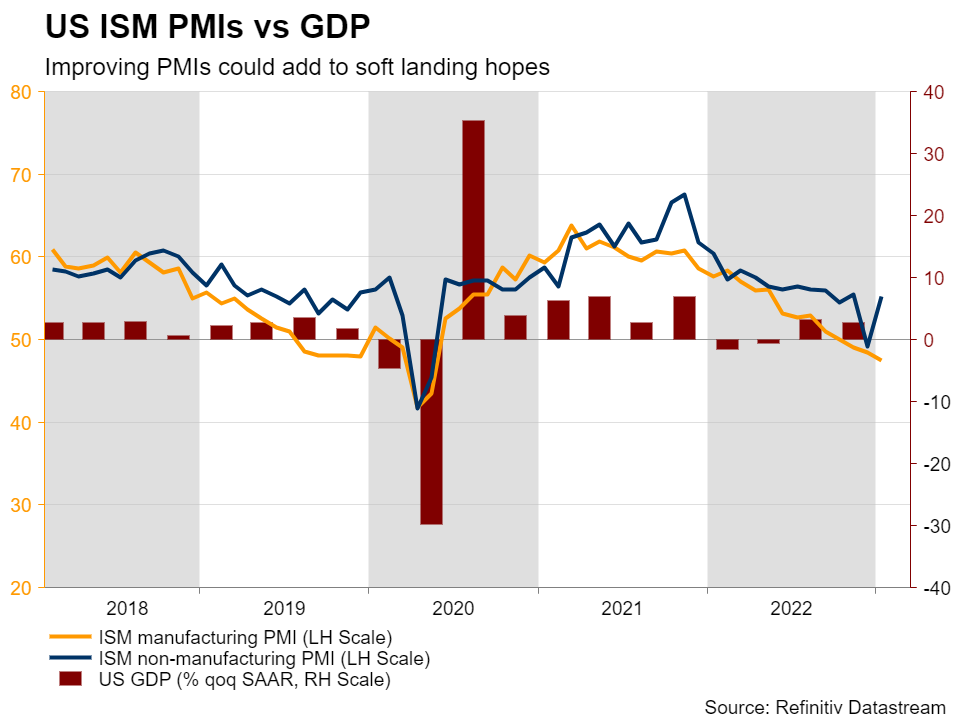

Getting the ball rolling with the US, last week, the preliminary S&P Global PMIs surprised to the upside, with the composite index returning from contractionary to expansionary territory. This was the latest piece of data confirming investors’ decision to drastically revise up their implied rate path projections. With January CPI data also suggesting that inflation is stickier than previously expected, they are now expecting interest rates to peak at around 5.35% in July, while they see them ending the year at 5.15%.

In that respect, the ISM PMIs on Wednesday and Friday are likely to attract special attention. Will they confirm or contradict the S&P Global indices? The forecasts point to a mixed picture, with the manufacturing PMI expected to have risen to 47.9 from 47.4, and the non-manufacturing PMI expected to have declined to 54.2 from 55.2. Nonetheless, given that the services index accounts for nearly 80% of US GDP, another print decently above 50 is unlikely to alter much expectations about the Fed’s future course of action.

The durable goods orders for January and the Conference Board consumer confidence index for February are also coming out on Monday and Tuesday respectively.

Anything adding to hopes that the US is likely to dodge a severe recession could support the US dollar on speculation that the Fed will continue raising interest rates at levels higher than it projected in December. That said, arguing about a full-scale bullish reversal in the US dollar remains premature as ahead of the March meeting, the market will have to digest the employment and CPI reports for February. On top of that, the Fed is not the only central bank for which investors have upended their rate hike bets.

Will Eurozone inflation numbers shake ECB bets?

One of them is the ECB. Most ECB officials have been adamant that more double hikes are needed, with President Lagarde confirming at the last meeting that another 50bps hike will be the case in March and several others hinting at a similar move in May. The only policymaker sounding a bit cautious was Chief Economist Philip Lane, who noted last week that the Governing Council may not need to proceed as forcefully as before.

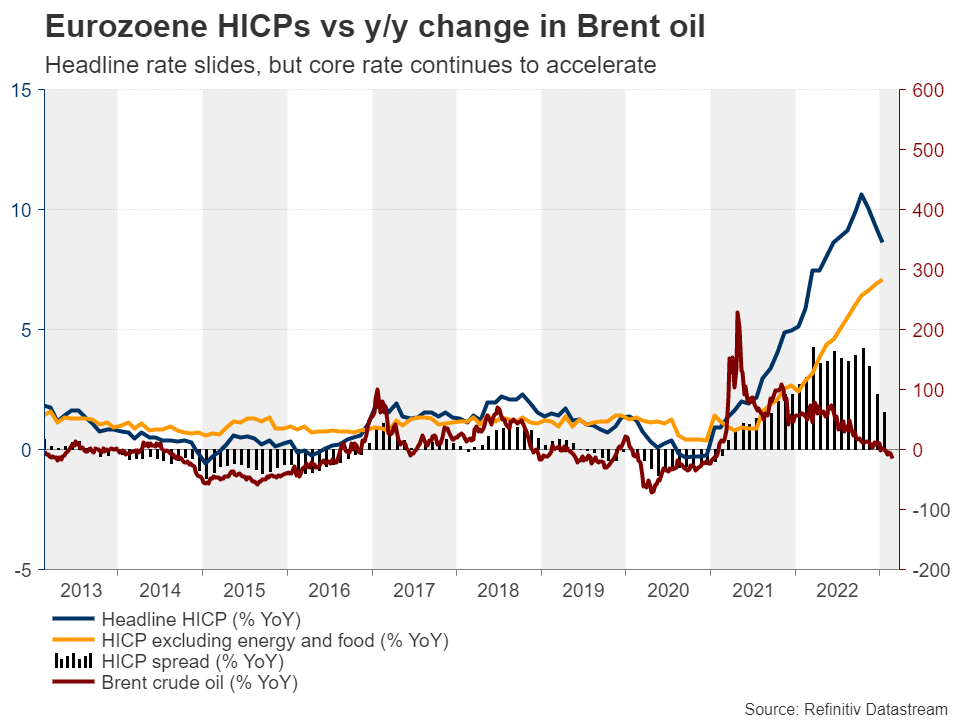

Yes, headline inflation has slowed notably after peaking at 10.6% in October and could slow even further in the months to come as the year-on-year change in oil prices continues to slide. Nonetheless, core inflation is proving tenacious, and Thursday’s data is expected to reveal a modest slowdown for the month of February to 6.9% y/y from 7.1%. The minutes of the latest ECB meeting are also on Thursday’s schedule.

Combined with improving PMIs in the Euro area, stubbornly high underlying inflation and more hawkish rhetoric by ECB officials could allow investors to maintain bets about a triple hike at the upcoming meeting. Currently, they are assigning a 30% probability for a 75bps increment, with the remaining 70% pointing to 50bps. They also see a total of 130bps worth of additional rate hikes before the Bank takes the sidelines, while just a week ago, they were seeing 100bps.

Increasing ECB hike bets are complicating things for euro/dollar sellers, but they also increase the downside risk in the case of an upcoming economic release disappointing. The same goes for the dollar. Therefore, the outlook for euro/dollar seems somewhat blurry for now. Maybe both currencies will perform better against the risk-linked ones as increasing hike expectations have been weighing on risk sentiment lately. With the slowdown in Canada’s inflation for January congealing expectations that the BoC may refrain from hiking rates further, the loonie may be the best choice.

Canadian and Australian GDP, as well as Chinese PMIs on tap

Loonie traders could place some hopes on Canada’s GDP figures, but with the m/m rate for December expected to have held steady at a modest 0.1% and the annualized q/q rate estimated to have declined to 1.5% from 2.9%, the picture for the loonie looks anything but bright.

Australia also releases GDP data for Q4, as well as its CPIs for January. In contrast to the BoC, the RBA raised interest rates by 25bps and dropped from its statement a part that put the option of a pause on the table, arguing that more hikes are necessary in the coming months. So, improving GDP and further acceleration in inflation would add credence to that view and perhaps allow the aussie to gain.

That said, with investors raising their bets with regards to more aggressive action by other major central banks as well, risk appetite has been very subdued lately, which is negative for risk-linked currencies like the aussie and the loonie. Thus, with the risk trade becoming a more or less zero-sum game in aussie/loonie, the Australian currency has more potential to gain against its Canadian counterpart rather than any other risk-linked currency, as the main driving force for this pair may be the divergence in monetary policy between the RBA and the BoC.

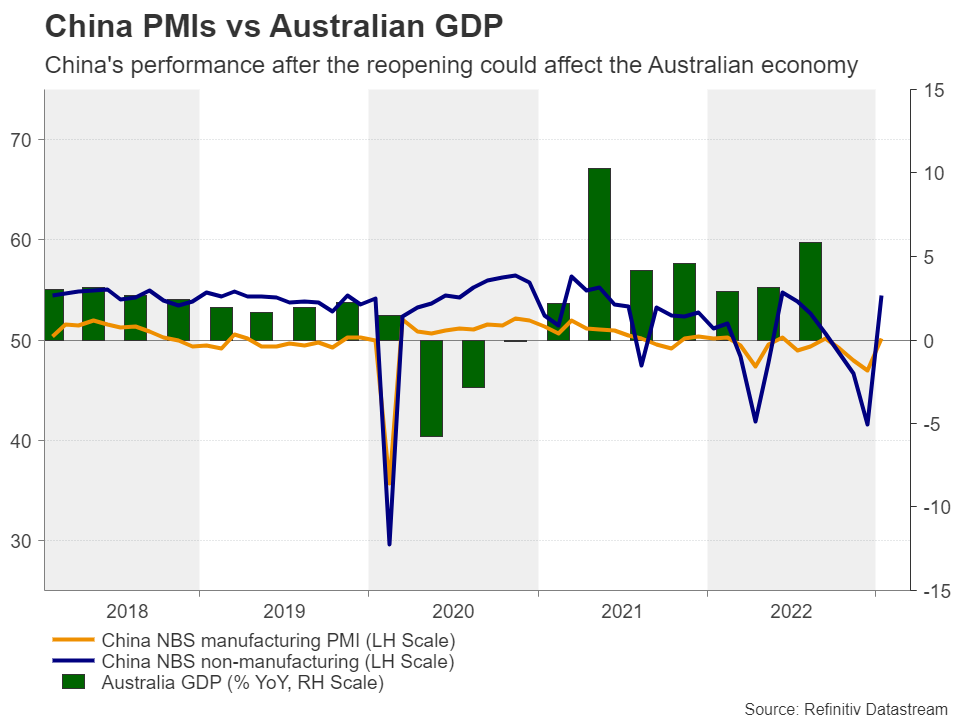

Aussie traders may also pay attention to the Chinese PMIs for February which come out just an hour after the Australian data. Given that China is Australia’s main trading partner, they may be eager to find out how the world’s second largest economy has been performing after the reopening.

After Ueda’s testimony, yen traders turn to the data

Flying from China to Japan, the world’s third biggest economy, next week’s agenda includes the industrial production and retail sales numbers for January on Tuesday and the Tokyo CPIs for February on Friday.

At his testimony before the lower house of the Japanese parliament, BoJ Governor nominee Kazuo Ueda said that the central bank must maintain ultra-low interest rates to support the economy, and while it signaled the chance of tweaking the yield curve control policy in the future, he seemed in no rush to overhaul the controversial policy.

So, as investors try to estimate when this could happen, they could pay close attention to the aforementioned data, especially the Tokyo CPI numbers, as they are a very good gauge of National inflation. Although they are not a major market moving data set, investors will have a first glimpse as to where inflation is headed and if it is set to continue to accelerate, they may start speculating a move towards normalization sooner rather than later.