{kind=link}

Summary

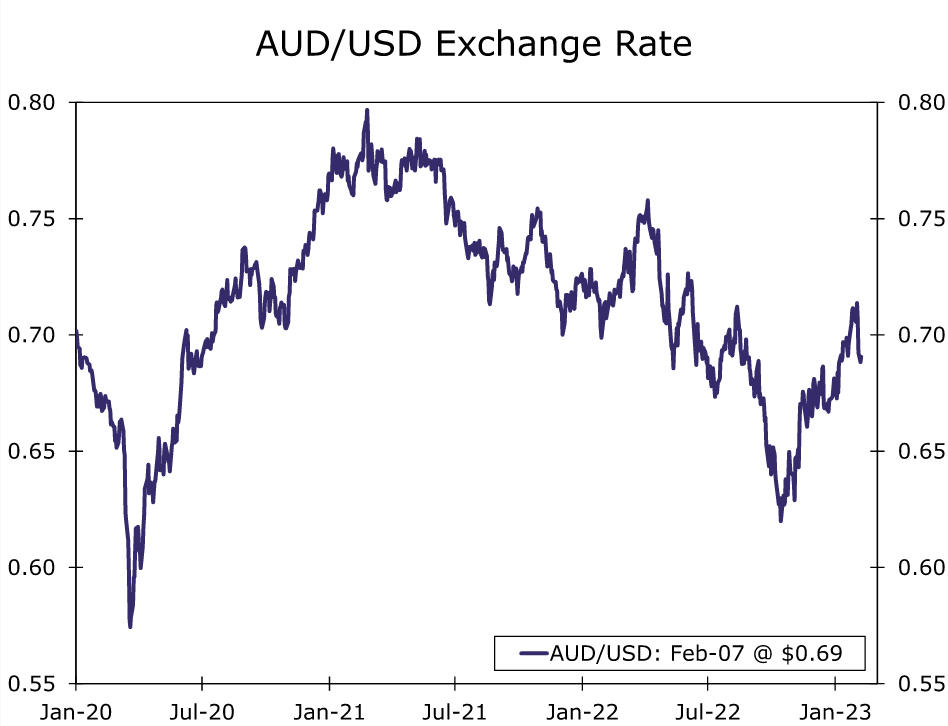

- The Australian dollar has been a solid performer in recent months and is up 11% from its October 2022 low. Given recent developments, we believe this positive trend can continue and have adopted a more constructive medium-term outlook for AUD/USD, targeting an exchange rate of $0.7800 by mid-2024.

- In our view, growth in Australia should be sturdy enough to avoid recession, and with inflation still elevated at the highest rate in over 30 years, we do not expect the Reserve Bank of Australia (RBA) to cut rates from now through mid-2024. This is in contrast to our expectation for a U.S. recession in H2-2023 and eventual Federal Reserve easing at the beginning of 2024. Resilient Australian growth and favorable RBA monetary policy dynamics versus the Fed are the main factors that should be supportive of the Australian dollar over time.

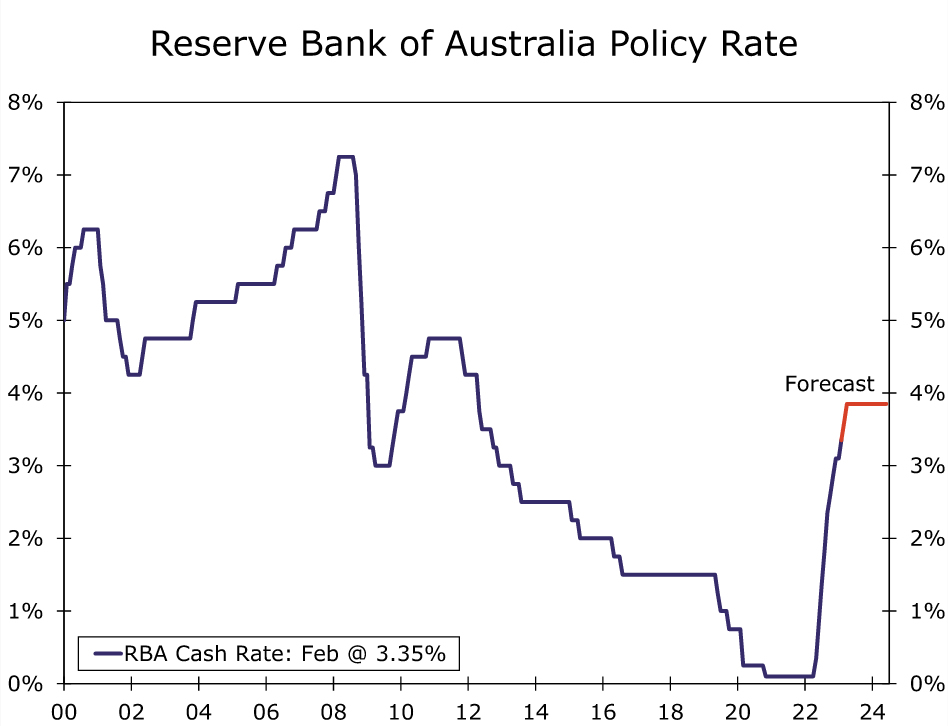

- Notably, the RBA raised its Cash Rate by 25 bps to 3.35% at its February monetary policy meeting and signaled additional rate hikes to come. Given some hawkish comments and guidance, we now expect the RBA to deliver two more 25 bps rate hikes in March and April to a terminal rate of 3.85%.

Emerging Divergence Between U.S. and Australia

The Australian dollar has been a solid performer in recent months, and is up 11% from its October 2022 low (Figure 1). Given recent developments, we believe this positive trend can continue and have adopted a more constructive outlook for AUD/USD, targeting an exchange rate of $0.7800 by mid-2024. A key driver of this improving outlook has been some important swings in growth and monetary policy trends. More specifically, our outlook for continued expansion in Australia’s economy is in contrast to our expectation for a U.S. recession in H2-2023. In addition, we expect eventual Federal Reserve easing in early 2024, whereas we do not forecast Reserve Bank of Australia rate cuts at this time.

In terms of U.S. monetary policy, the Fed is becoming less hawkish, having shifted from 50 and 75 bps rate hikes during much of 2022 to just 25 bps in February. In addition, price pressures in the U.S. have subsided somewhat—inflation receded to 6.5% year-over-year in December, down from a peak of 9.1% in June last year. For now, U.S. activity indicators are mixed, though they are perhaps consistent with some overall slowing. Nonfarm payrolls jumped in January and the ISM services index rebounded to growth territory. However, the January ISM manufacturing index fell for a fifth straight month, while real consumer spending and consumer confidence fell late last year. Overall, we forecast a U.S. recession in the second half of 2023, which should place broad depreciation pressure on the dollar.

Inflation Still Elevated in Australia

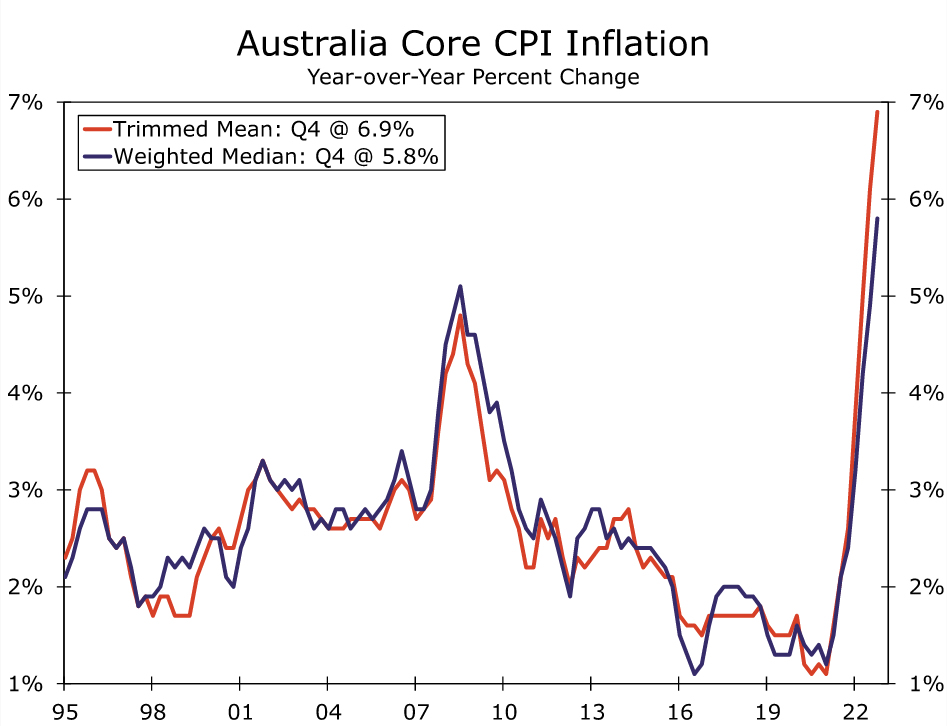

In contrast to the downshift from the Federal Reserve, the Reserve Bank of Australia has been hiking rates at a steady 25 bps pace and does not appear to have a dovish pivot on the immediate horizon. Australian inflation has remained elevated, demonstrating no clear signs of slowing yet from the highest rate in over 30 years. While prices within many peer developed economies have already begun to recede from their respective peaks, inflation in Australia appears to have remained persistently high to end 2022. Indeed, the headline CPI quickened to an above-consensus 7.8% year-over-year in Q4. Perhaps even more importantly, underlying measures of inflation accelerated more than expected in the fourth quarter. Trimmed mean and weighted median inflation rose to 6.9% and 5.8%, respectively (Figure 2). These two measures of core inflation remaining significantly above the RBA’s medium-term 2-3% inflation target band and lead us to believe more rate hikes are on the way. Additionally, while both measures quickened in Q4, tradables inflation, which is influenced by currency movements (stronger AUD) and international conditions (softer commodity prices), was higher at 8.7%, compared to domestically-oriented non-tradables inflation, up 7.4% over the year.

RBA Monetary Tightening Not Done Yet

With inflation still elevated, the RBA raised its Cash Rate by 25 bps to 3.35% at its February meeting and signaled additional rate hikes to come. The announcement contained some hawkish-leaning commentary and conveyed a sense of steadfastness in bringing inflation back to target.

The announcement reiterated that inflation is too high, but is expected to recede this year due to both global factors and slower domestic demand. The RBA’s central forecast is for CPI inflation to decline to 4.75% this year and reach around 3% by mid-2025. It acknowledged that monetary policy operates with a lag and the cumulative effect of rate hikes is yet to be fully felt by households, but it also recognized that if high inflation were to become entrenched in expectations, it would be very costly to reduce later on. Thus, lower inflation remains the main priority for the central bank. With respect to economic growth, the RBA expects GDP growth to slow to around 1.5% over both 2023 and 2024.

Lastly, the Board explicitly signaled “further increases in interest rates will be needed over the months ahead.” Given the hawkish comments and guidance, we now expect the RBA to deliver two more 25 bps rate hikes in March and April to a terminal rate of 3.85% (Figure 3). Just as importantly, with inflation elevated, we do not expect the RBA to ease monetary policy from now through mid-2024.

Slower Australian Growth Prospects, But Recession Unlikely

While Australia’s recent sentiment, PMI, and employment data showed some softness to end 2022 and suggest some areas of the economy have begun to slow, we believe growth will be sturdy enough to avoid recession.

With respect to activity data, labor market trends turned less positive in December, as the employment report showed an unexpected 14,600-job decline following four months of solid gains. That said, the decline was entirely due to a drop in part-time employment, while full-time employment increased. In our view, the miss in the December jobs report shouldn’t be enough to prevent further tightening, as the RBA still views the labor market as being very tight. In addition to the unexpected jobs decline, consumers and households have started to feel the sting from elevated inflation and higher interest rates. After eleven consecutive months of gains, December retail sales dropped more than expected by 3.9% month-over-month. Meanwhile, after adjusting for inflation, Q4 real retail sales fell by 0.2% quarter-over-quarter, pointing to higher prices weighing on the retail sector.

China’s Reopening Provides a Tailwind

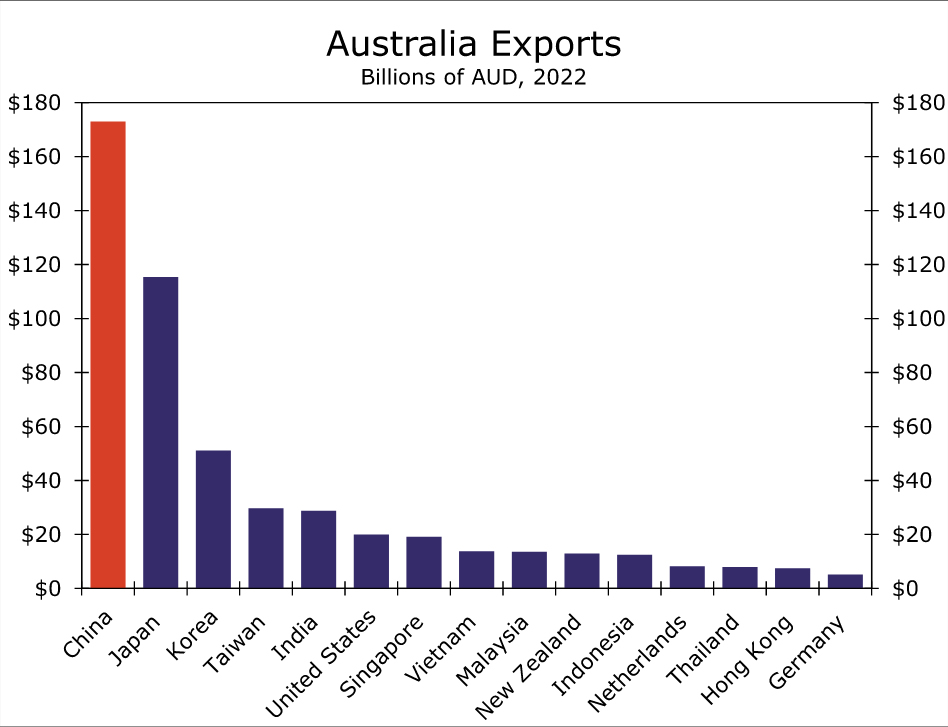

Importantly, we believe this soft patch for Australian economic growth will be temporary. After two years of Zero-COVID, China’s reopening led us to upgrade our Chinese GDP growth outlook for 2023 to 5.2%. The improved outlook for China should also improve Australia’s growth prospects and sentiment towards the Australian dollar, given strong trade linkages between the two countries (Figure 4). Given that 28% of Australia’s GDP consists of exports and around 45% of those exports go to China, we believe positive growth trends in China will provide a boost Australia’s economy.

In another encouraging development, government officials from China and Australia met this week to discuss trade relations after the Chinese government placed restrictions on a variety of exports from Australia in 2020. According to a statement from the Chinese Commerce Ministry, both parties agreed to “enhance dialogue”, with a goal of “timely and full resumption of trade.” In addition, trade officials from both countries agreed to further future discussions in Beijing, as the meeting “represents another important step in the stabilization of Australia’s relations with China.”

This in combination with recent announcements that China would resume purchases of Australian coal after a two-year pause should be a boost for AUD, and could open the door for further easing of trade restrictions. In any case, considering the resilient medium-term outlook for economic growth, we do not believe the recent soft patch will prevent additional RBA rate hikes or currency gains.

Australian Dollar’s Path Looks Brighter Ahead

To sum up, given our outlook for Australia to enjoy a reasonably steady expansion over time and avoid recession, our base case remains for some further monetary policy tightening before a pause in rate hikes. Even if the RBA were to eventually cut rates (which is not our base case though mid-2024), we anticipate that any RBA easing would be noticeably later than the Federal Reserve’s and smaller in magnitude. And as we highlighted above, continued Australian growth also contrasts with an expected recession in the United States. Against this backdrop, we believe resilient Australian growth and favorable RBA monetary policy dynamics versus the Fed are the main factors that should be supportive of the Australian dollar over the medium term. Those factors underpin our forecast for the AUD/USD exchange rate to appreciate to $0.7800 by mid-2024. We expect the Australian dollar to be an outperformer among G10 currencies during this period.