{kind=link}

After trading in a rollercoaster manner in 2022, oil seems to be starting the new year between a rock and a hard place as the outcomes of ongoing market-related themes could end up working in favor of it or against it. In other words, the risks surrounding the black liquid are two-sided, and it remains to be seen which will prevail in the weeks and months to come.

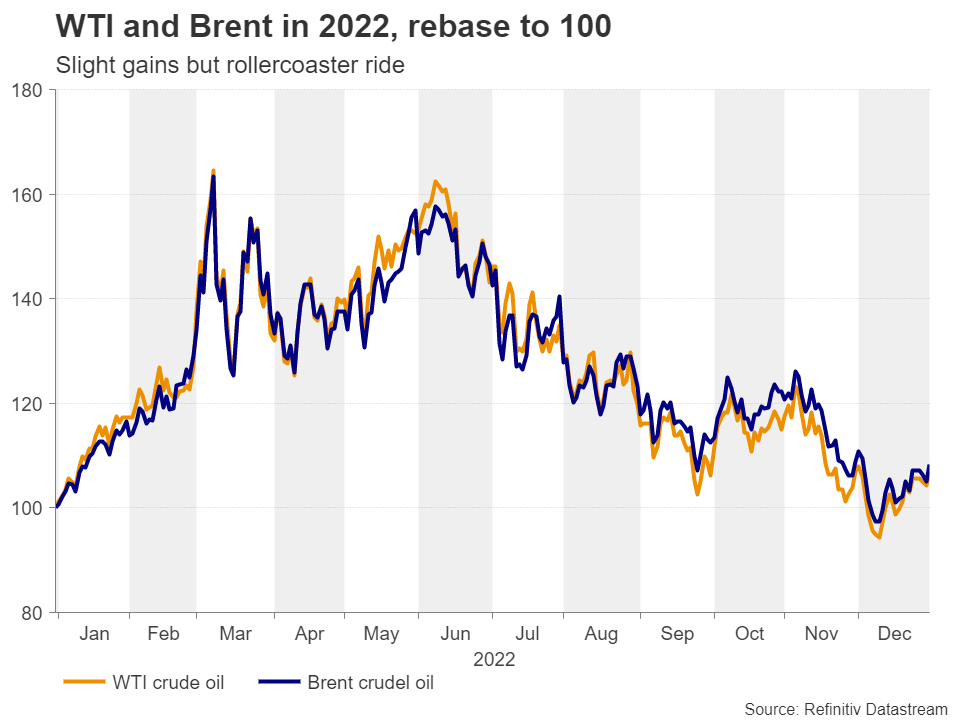

Oil trades in rollercoaster fashion in 2022

Oil prices finished 2022 slightly in the green, with WTI and Brent crude oil futures adding yearly gains of around 7% and 9% respectively. However, these numbers are not telling the whole story. From around $75 per barrel, WTI shot up to around $130 in the aftermath of Russia’s invasion of Ukraine, reversing south soon thereafter as sky-high inflation and aggressive tightening by major central banks sparked fears about a global recession and thereby concerns about weaker demand for the black liquid.

Entering 2023, oil seems to be trading between a rock and a hard place, as the current landscape and potential responses to expected developments could drive prices either way.

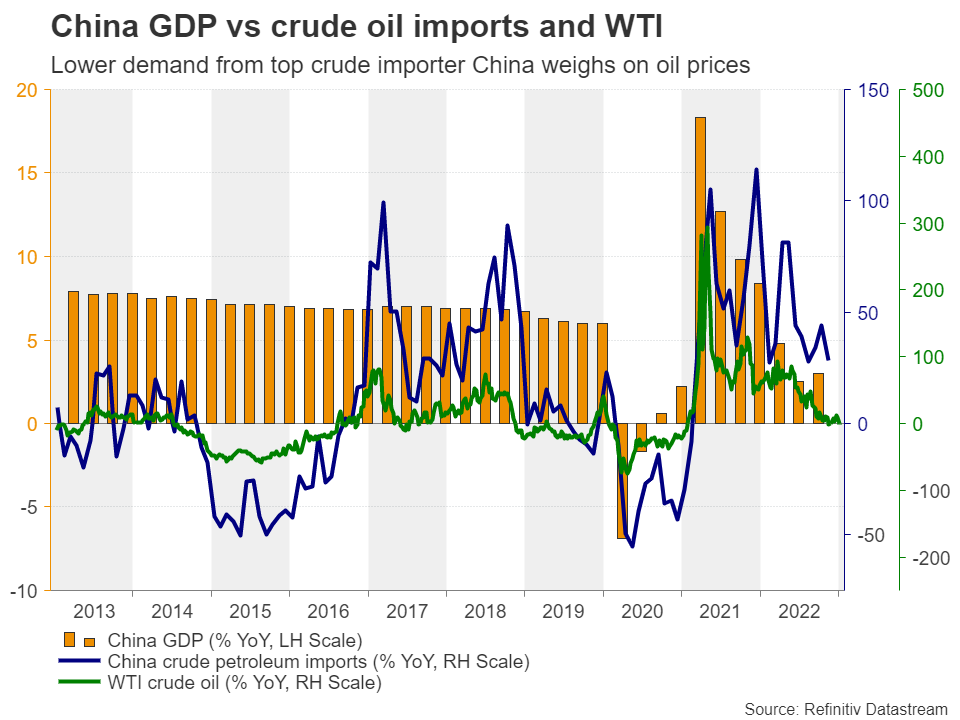

Is the reopening of China a positive development?

Getting the ball rolling with China, in early December, investors cheered headlines of a gradual easing of COVID restrictions and a reopening of the world’s second largest economy. Oil prices joined the party and rebounded from a nearly one year low on hopes that demand from the world’s top crude importer could be restored.

That said, with COVID infections soaring in many districts, the optimism faded fast. Investors became worried that, let alone the risk of reversing relaxations, the Chinese economy may take much longer to recover. There are also increasing concerns about the risk of new variants spreading to the rest of the world, resulting in economic complications elsewhere as well and thereby more reduction in fuel consumption. And all this as major economies, like the EU, the US, and the UK, are already considerably wounded.

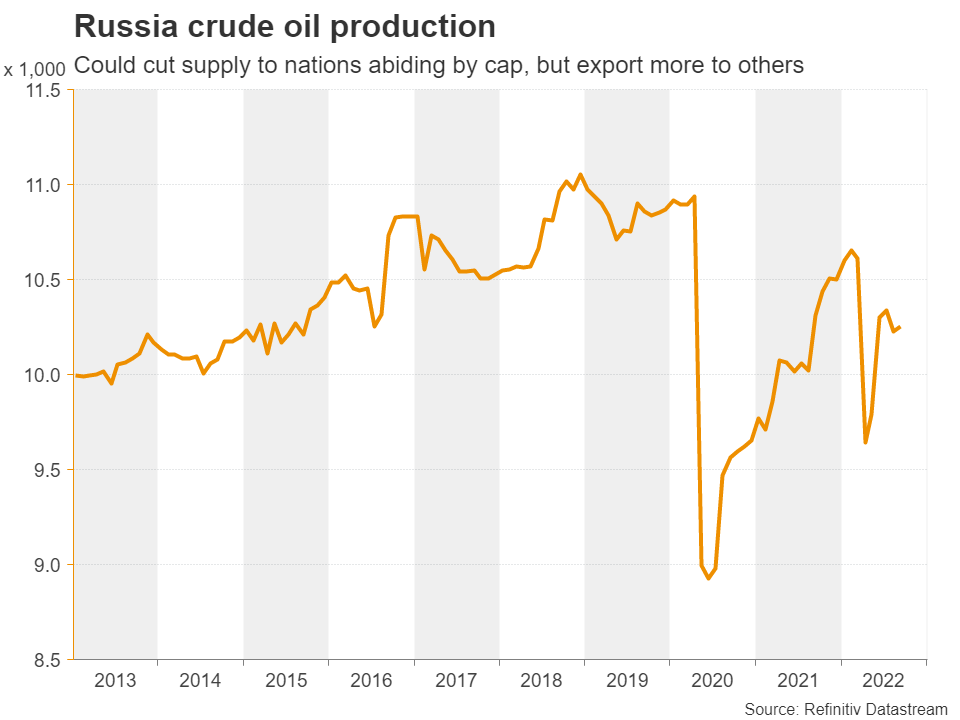

What about the cap on Russian oil?

Apart from China’s reopening, the cap imposed by the G7 nations on Russian oil is another double-edged sword. Following the verdict, Russia decided to ban the supply of oil to nations that will abide by the cap for five months starting in February, which is supportive for prices.

Nonetheless, given that more Russian oil is now shipped to China, Turkey, and Indonesia for refining and that there are no restrictions for the US and Europe on importing petroleum products made with Russian oil outside Russia, any gains in oil prices from Russia’s banning may be limited and short lived.

US reserves, OPEC, and winter also variables in the oil equation

Another source of demand may be the US’s decision to replenish its strategic petroleum reserve after selling record amounts, while the list of arguments pointing to a limited recovery includes the possibility of OPEC reversing some of its production cuts announced in November, as the cartel’s own projections point to increasing demand in 2023.

Winter is also a variable in the oil equation. EU nations’ ability to pile up oil before Russia’s retaliating measures take full effect and a mild winter so far have allowed oil prices to stay in downtrend mode. However, should winter get colder in the coming months, demand for heating oil could increase and thereby lift prices.

Outlook seems blurry for now

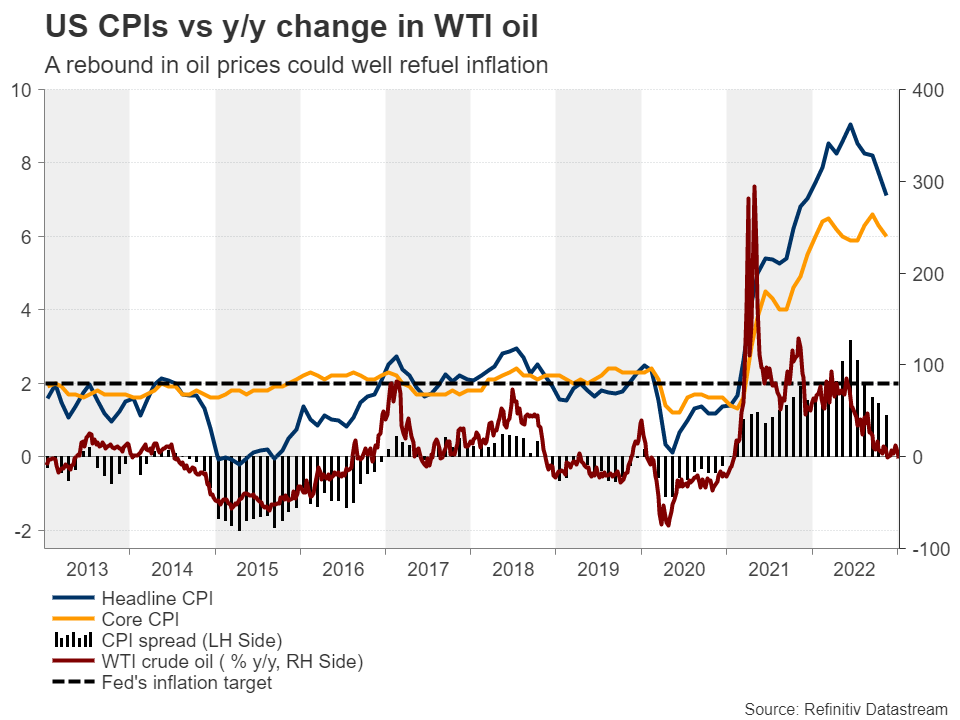

Blending everything together, the short-term outlook of oil looks blurry for now. Having said that though, what appears to be a clearer case for the next months is that a sustained uptrend may be off the books. Even if the Chinese economy recovers faster and oil demand is restored, and even if supply tightens more due to Russia’s decisions, a strong recovery in oil prices could well refuel inflation.

Should the central banks respond by re-accelerating and extending their tightening crusades, the global economy is very likely to fall into a deeper recession than currently estimated, which would eventually weigh on oil prices due to speculation that demand for energy could be dented again. A rebound in the US dollar as it reclaims the throne of the ultimate safe haven may also weigh on oil.

Now, if the surging infections in China result in more economic complications and the reopening of its borders more spreading of the virus to the rest of the world rather than spurring an economic recovery, oil prices may come instantly under pressure, with WTI perhaps falling below $70 per barrel.

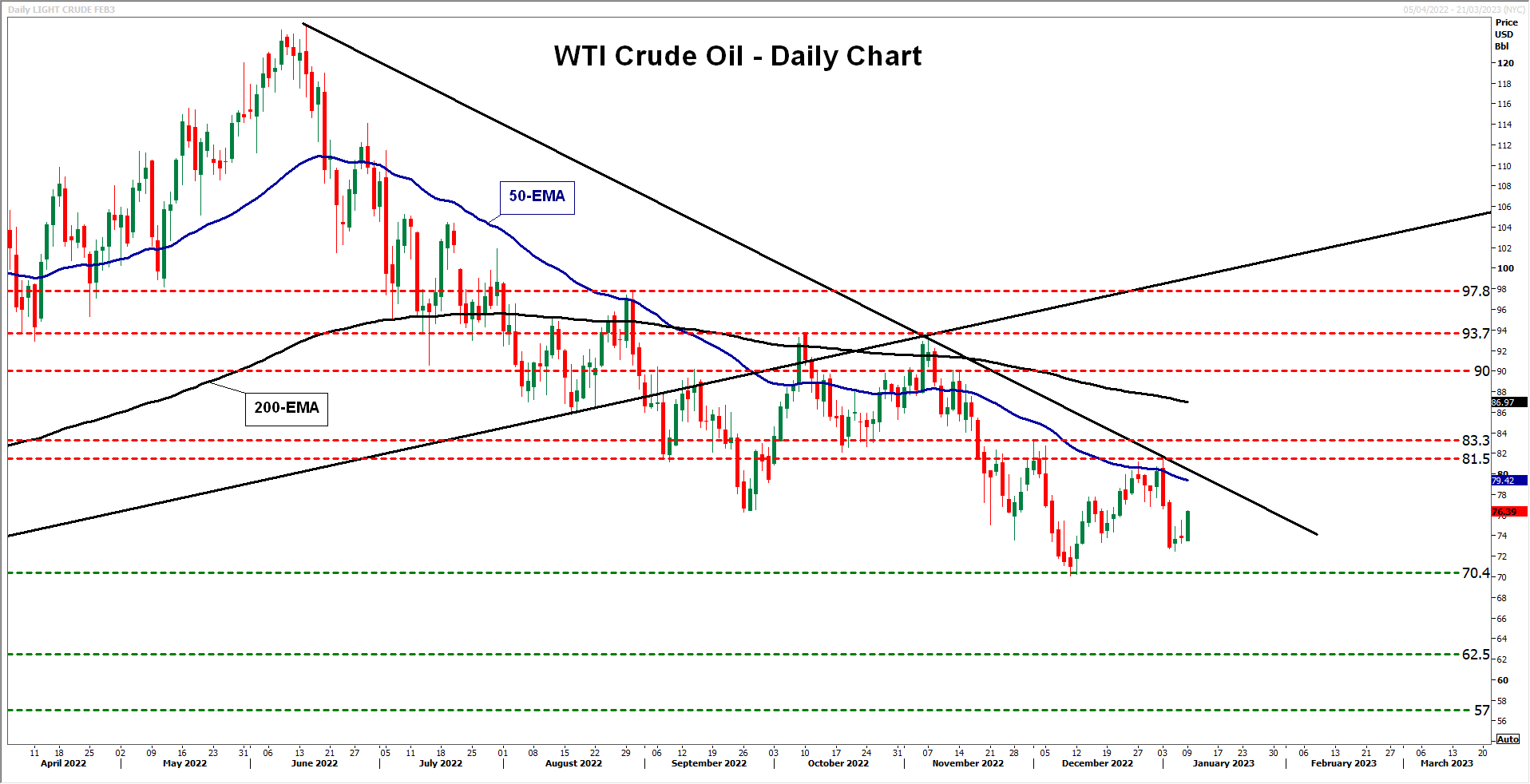

Technical analysis still points to a downtrend

From a technical standpoint, WTI crude oil remains below the long-term uptrend line taken from the low of April 28, 2020, below the downtrend line drawn from the high of June 14, and below both the 50- and 200-day exponential moving averages. On top of that, last week, the black liquid came under selling pressure after hitting the short-term downtrend line, which implies that the bears may not have said their last word, despite allowing a rebound at the start of this week.

Should they overcome the low of December 9 at 70.40, a lower low would be confirmed and the trend may extend towards the low of December 2, 2021, at around 62.50. If that zone does not hold either, additional declines may result in the test of the 57.00 barrier, marked by the low of March 23, 2021, or even challenging the 51.50 zone, which provided support during January that year.

A decent recovery may be triggered upon a break above the 83.30 hurdle, which provided resistance on December 1 and support in October. Such a break could also take the price above the downtrend line and may allow advances towards the round number of 90.00 or the key resistance zone of 93.70, marked by the highs of October 7 and November 7 respectively. Slightly higher lies the peak of August 30 at 97.80 and the prior longer-term uptrend line, which may act as a strong resistance and confirm the hypothesis that any near-term recovery in oil prices is unlikely to lead to a sustained uptrend.

A meaningful uptrend may be a theme for the second half of 2023, conditional upon further cooling in inflation (especially underlying metrics), the end of the latest tightening crusade by major central banks, and signs of economic recovery worldwide.