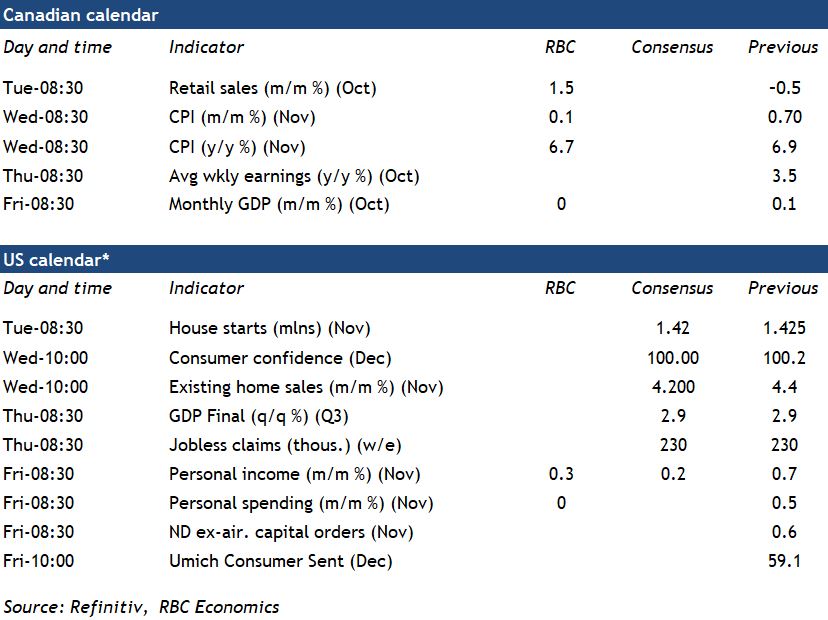

{kind=link}

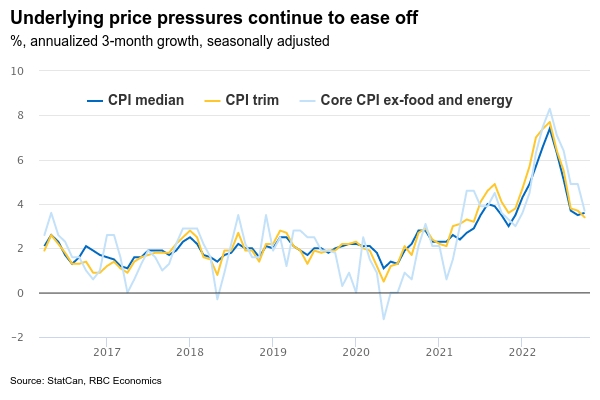

Canadian inflation is falling further from its summer peak. CPI growth likely edged down to 6.7% year-over-year. Though that’s still very high, it nevertheless marks another drop below the measure’s 8.1% peak in June. Easing global inflation pressures have been behind much of that deceleration. Gas prices declined again in November, dropping 4% from October. Food prices were likely still running 10% above year-ago levels. And ‘core’ measures of price growth, like the Bank of Canada’s preferred ‘median’ and ‘trim’ measures are still running 5% above year-ago levels. But recent month-over-month price increases have slowed significantly—an early sign that broader inflation pressures are also moderating.

The BoC has pointed to those early signs as a reason that interest rates may not need to rise further following a 50 basis point rate hike last week. The economy is also expected to soften in coming quarters as 400 basis points of interest rate hikes in 2022 cut into household purchasing power, further easing inflation pressures. The advance estimate of October GDP was “essentially unchanged” after a small 0.1% increase in September. We expect little change in the early estimate of November output. Hours worked rose just 0.1% in November. And consumer spending is holding up well for now. Statcan’s early estimate of retail sales was up 1.5% in November and our own tracking of card transactions suggests sales early in the holiday shopping season have been strong. But the outlook for the manufacturing sector is starting to look softer and housing markets continue to retrench.

Week ahead data watch

We expect U.S. personal income to edge up 0.3% in November. Hourly wages rose 0.6% in the month, but hours worked edged lower. U.S. personal spending was likely unchanged in November, given a softening in retail sales (-0.6%). We expect ‘real’ sales (excluding price impacts) to have declined by 0.2%.

Wage growth from the SEPH data will be closely watched given the three-month rolling average hourly earnings were more than a percentage point below LFS in September.

The advance estimate from StatCan showed October retail sales grew by 1.5%. Auto sales ticked higher, and gas station sales likely ticked down on lower gasoline prices. We expect the advance estimate of November sales to remain firm. Our own tracking of card transactions suggests strong November holiday spending and another increase in unit auto sales.