{kind=link}

EUR/USD: Ahead of the Fed and ECB Meetings

Two key events await us next week. The first is the FOMC (Federal Open Market Committee) meeting of the US Federal Reserve, which will be held on Wednesday, December 14. Recall that the key interest rate on the dollar is 4.00% at the moment, and that Fed Chairman Jerome Powell confirmed on November 30 that the pace of rate growth may slow down in December. These words of his convinced market participants that the rate would be increased in December not by 75 basis points (bp), but by only 50 bp. The actual developments on December 14 will set the mood of the regulator for 2023. Naturally, an important role here will be played not only by the decision on the interest rate itself, but also by the economic forecasts of the FOMC and the press conference of the management of this organization following the meeting.

It is highly likely that the decision of the Committee members will be influenced by data on inflation in the US: the November values of the Consumer Price Index (CPI) will be announced on the eve of the meeting, on Tuesday, December 13.

The second event is the ECB meeting on Thursday, December 15. The interest rate on the euro is 2.00% at the moment, and according to forecasts, the European regulator will also raise it by 50 bp, which will keep the advantage in favor of the US currency: 4.50% against 2.50%. As in the case of the Fed, the comments and forecasts of the ECB leaders, which will be made after this meeting, will also be important for market participants.

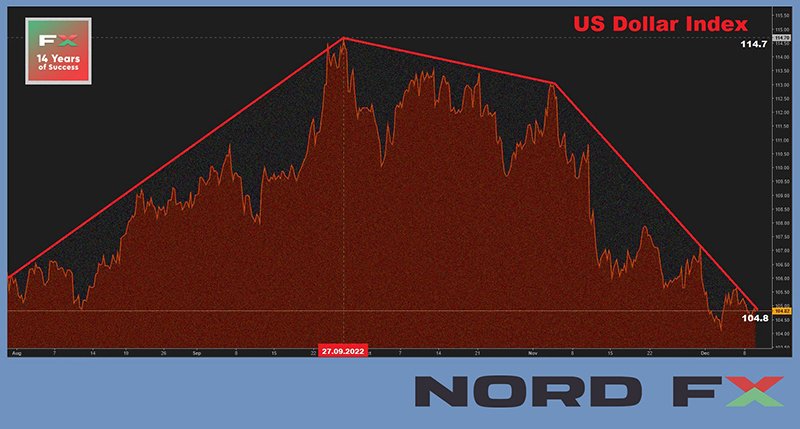

As for the past week, the DXY Dollar Index did not manage to win back at least some of the losses it has suffered since the end of September. This time it was hampered by statistics from China. On the one hand, China’s manufacturing sector continues to deflate: the Producer Price Index (PPI) has been falling by 1.3% for the second month in a row. On the other hand, inflation is slowing down: the Consumer Price Index (CPI) in November was 1.6% against 2.1% a month ago. In this situation, the Chinese government has taken a course of easing monetary policy (QE) to support the country’s economy. A survey conducted by Bloomberg showed that the market expects the People’s Bank of China to cut interest rates on the yuan as early as Q1 2023. Against this background, stock indices, primarily Asian ones, went up, and the dollar went down. Optimism over the easing of strict COVID-19 restrictions in China also supported the positive tone in equity markets.

Additional pressure on the US currency was exerted by statistics on the US labor market. The number of initial applications for unemployment benefits became known on Thursday, December 08. This figure showed a slight increase from 226K to 230K, which was fully in line with the forecast. But repeated applications have reached a maximum over the past ten months: 1671K, which is also a signal for the Fed, pointing to problems in the economy.

On the contrary, European macro statistics looked good. Thus, the GDP of the Eurozone in Q3 turned out to be higher than the forecast, 0.3% vs. 0.2% (q/q) and 2.3% vs. 2.1% (y/y).

As a result, EUR/USD abandoned a deep correction and, having reached a local low of 1.0442 on December 07, reversed and rose to the level of 1.0587 on December 09. The Producer Price Index (PPI) and the Consumer Confidence Index from the University of Michigan made modest adjustments to the prices at the very end of the working week, after which the pair finished at 1.0531.

50% of analysts count on its further growth, 25% expect the pair to turn south. The remaining 25% of experts point to the east. It should be noted here that when moving to a medium-term forecast, the number of bearish supporters who expect the pair to drop below the parity level of 1.0000 increases sharply, up to 75%.

The picture is different from the oscillators on D1. All 100% of the oscillators are colored green, while 10% is in the overbought zone. Among the trend indicators, the 100% advantage is on the green side.

The nearest support for EUR/USD is located at the 1.0500 horizon, then there are levels and zones 1.0440, 1.0375-1.0400, 1.0280-1.0315, 1.0220-1.0255, 1.0130, 1.0070, followed by the parity zone 0.9950-1.0010. Bulls will meet resistance at levels 1.0545-1.0560, 1.0595-1.0620, 1.0745-1.0775, 1.0865, 1.0935.

We will see other important macro statistics next week in addition to the above. Thus, data on consumer inflation (CPI) and economic sentiment (ZEW) in Germany will be released on Tuesday, December 13. And business activity indicators in the manufacturing sectors of Germany and the Eurozone (PMI), as well as the November value of the European Consumer Price Index (CPI) will become known on Friday, December 16.

GBP/USD: Ahead of the Bank of England Meeting

Not only the ECB, but also the Bank of England (BoE) will decide on the interest rate on Thursday, December 15. It should be noted that the regulator of the United Kingdom was one of the first among the G10 Central Banks, following the Fed, to curtail the policy of quantitative easing (QE). It raised the pound interest rate by 75 bps in November. However, it is expected that like the ECB and the Fed, it will raise it by only 50 bp in December, after which it will reach 3.50%. According to a survey conducted by Reuters, 96% of economists have voted for this step. And only 4% of them insist on 75 bp.

Most respondents believe that the recession will be long and shallow. According to forecasts, the economy contracted by 0.2% in Q3 2022 (exact data will be known on December 12) and will decrease by another 0.4% in Q4. The fall in the first three quarters of 2023 may be 0.4%, 0.4% and 0.2%, respectively.

As for inflation, the survey conducted by the BoE showed that the fears of the UK population about it have slightly decreased. If we talk about economists’ forecasts, it is expected that in it will reach a peak of 10.9% in Q4, and then it will decline. The current value is more than five times higher than the target level of 2.0%. And the Bank of England will be forced to continue to raise the rate to fight inflation, despite the threat of a deepening recession. It is predicted that BoE will raise it in Q1 and Q2 2023, another 50 bp and 25 bp, respectively, to 4.25%.

GBP/USD, as well as EUR/USD, has been developing an upward trend since the end of September taking advantage of the weakness of the dollar. In addition, it is being pushed up by the end of the fiscal micro-crisis and the Bank of England’s actions to tighten monetary policy and support the British government bond market. GBP/USD reached its maximum value on December 05 at the height of 1.2344, however, it did not go further north and completed the five-day period at the level of 1.2260 in anticipation of the decisions of the coming week.

Strategists at the German Commerzbank consider the current situation only a temporary respite and expect increased pressure on the British currency. “At present,” they write, “the relief that the fiscal crisis has been brought under control prevails, and there are no signs of a further worsening of the energy crisis. In our opinion, this is only a temporary respite for the pound. The deteriorating economic outlook, relatively prudent monetary policy […] and continued high inflation continue to put major pressure on the pound.”

The median forecast for the near term copies the forecast for EUR/USD in full: 50% of experts side with the bulls, 25% side with the bears, and the remaining 25% prefer to remain neutral. At the same time, there is a slight difference when moving to the medium-term forecast: the number of bear supporters here is 10% higher, 85%.

The readings of trend indicators and oscillators on D1 also copy the readings of their counterparts for EUR/USD: all 100% are on the green side, and 10% of the oscillators give signals that the pair is overbought.

Levels and support zones for the pair are 1.2210-1.2235, 1.2150, 1.2085-1.2105, 1.2030, 1.1960, 1.1900, 1.1800-1.1840, 1.1700-1.1720, 1.1475-1.1500, 1.1350, 1.1230, 1.1150, 1.1100. When the pair moves north, it will meet resistance at the levels of 1.2290-1.2310, 1.2345, 1.2425-1.2450 and 1.2575-1.2610, 1.2750.

As already mentioned, Monday, December 12, when the country’s GDP data will be published, attracts attention this week, as for the events concerning the economy of the United Kingdom. Data on unemployment and wages will arrive the following day, that on consumer prices (CPI) will become known on Wednesday, December 14, and on retail sales and business activity in the UK – on Friday, December 16. And of course, a special emphasis is on December 15, when the Bank of England will issue its verdict on the interest rate.

USD/JPY: What Can Help the Yen

USD/JPY rose from the Dec 02 low of 133.61 to 137.85 last week, slightly above the strong 137.50 support/resistance zone. The last chord of the week sounded at 136.60.

The future of the pair will continue to depend on the difference in interest rates between the US and Japan. If the Fed remains at least moderately hawkish and the BoJ remains ultra-dovey, the dollar will continue to dominate the yen. The threat of new foreign exchange intervention by the Ministry of Finance of Japan, the same as it was on November 10, seems unlikely at current levels. Raising the key rate could help, but it is very likely that the Bank of Japan (BoJ) will leave it unchanged at its meeting on December 20: at the negative level of -0.1%. A radical change in monetary policy can be expected only after April 8 next year. It is on this day that Haruhiko Kuroda, the head of the Bank of Japan, will end hs term, and he may be replaced by a new candidate with a tougher position. Although this is not a fact.

Another hope is for renewed concerns about China’s economic prospects. “Weak growth rates and a clear decline in bond yields,” economists from the ING banking group believe, “should lead to the fact that safe currencies, such as the yen, will begin to show superiority,” and this will support the Japanese currency.

Analysts’ forecast for the near future is bearish: 50% of them vote for the pair to fall, the remaining 50% have taken a neutral position. However, in the medium term, most experts (60%) are shifting their gaze from south to north, expecting a serious strengthening of the dollar and the return of the pair to the 145.00-150.00 zone. For oscillators on D1, the picture looks like this: 90% look south, 10% look north. Among the trend indicators, the ratio is 85% versus 15% in favor of the red ones.

The nearest support level is located at 136.00 zone, followed by levels and zones 134.10-134.35, 133.60, 131.25-131.70, 129.60-130.00, 128.10-128.25, 126.35 and 125.00. Levels and resistance zones are 137.50-137.70, 138.00-138.30, 139.00, 139.50-139.75, 140.60, 142.25, 143.75, 145.30, 146.85-147.00, 148.45, 149.45, 150.00 and 151.55. The purpose of the bulls is to rise and gain a foothold above the height of 152.00.

The calendar could mark Wednesday December 14, when the values of the Sentiment Indices of Large Manufacturers and Non-Manufacturing Tankan Companies for Q4 2022 will be announced. The publication of other macro indicators of the Japanese economy is not expected next week.

CRYPTOCURRENCIES: Christmas Rally After Crypto Massacre

We titled the last review “Cryptogeddon Instead of Crypto Winter” (by analogy with Armageddon, the place of the last and decisive battle between the forces of good and the forces of evil). There is another “bloody” term now: “crypto massacre”, which characterizes what happened as a result of the collapse of the second most capitalized crypto exchange, FTX. Investors lost $10.16 billion in just one week in November. This crisis was like a domino, which led to the collapse of many other companies. About 94% of respondents believe the FTX bankruptcy will be followed by further turmoil as years of easy lending give way to a tougher business and market environment, according to a Bloomberg survey. To complicate matters , between 73% and 81% of investors lost money due to investing in cryptocurrencies between 2015 and 2022. This is evidenced by data from a study conducted by the Bank for International Settlements (BIS).

The price of bitcoin is consolidating around $17,000 at the moment, and the readings of the SMA100 and SMA200 indicators on the four-hour chart have converged almost at one point. BTC/USD is kept from falling by the dollar that has sagged in recent weeks. Markets froze in anticipation of December 14, when the Fed will make a decision on the interest rate. And it, in turn, depends on the data on inflation in the US, which will arrive the day before. The FOMC (Federal Open Market Committee) Economic Forecasts will also play a significant role in the dollar dynamics.

Optimists, including crypto communities such as Credible Crypto, Moustache and Dave the Wave, expect this data to positively influence the market’s risk appetite, and the Christmas rally will push bitcoin to $20,000. According to the expectations of members of the crypto community CoinMarketCap, BTC will trade at an average price of $19,788 by the end of the year.

PricePredictions’ machine learning algorithms, which include a number of technical indicators (MA, RSI, MACD, BB, etc.), indicate a price of $1,000 lower. According to their metrics, the main cryptocurrency will reach $18,797 on December 31, 2022.

However, not everything is so rosy and unambiguous. For example, Bloomberg Intelligence senior strategist Mike McGlone believes that cryptocurrencies are now going through the last stage before reaching the bottom. However, he warns that it will be very difficult to survive this phase: “Normally, markets do not just form a V-bottom. They make it as hard as possible with a lot of volatility, taking money from all investors.”

According to Michael Van De Poppe, a well-known trader and analyst, the pair will face many difficulties on the way to $19,000. The bulls will need to break through the important resistance level in the $17,400-17,600 range and then try to reach the $18,285 horizon.

As for the price of ethereum, Van de Poppe believes that the key support level for this cryptocurrency is the price of $1,200. Mike McGlone is of the same opinion. According to his calculations, ETH has strong support close to the current price level.

There is very little time left until the end of the year, and then we will find out who was more accurate in their forecasts. In the meantime, at the time of writing the review (Friday evening, December 09), ETH/USDis trading around $1,260, and BTC/USD – $17,100. The total capitalization of the crypto market has not changed much over the week and is $0.852 trillion ($0.859 trillion a week ago). The Crypto Fear & Greed Index has fallen only 1 point in seven days, from 27 to 26 and still remains in the Fear zone.

And to conclude the review, a few words about longer-term forecasts. Such popular Twitter analysts as Bluntz and Korinek_Trades do not rule out BTC/USD falling to $15,000 or even $12,000 in Q1 2023.

The picture drawn by Standard Chartered economists is even bleaker. They expect that the collapse of FTX will continue to affect the mood of the crypto market, the series of bankruptcies of large industry participants will continue, which will lead to a further loss of confidence in digital assets. As a result, bitcoin’s price could fall to $5,000 during 2023. Standard Chartered Chief Strategist Eric Robertsen allowed investor interest to switch from the digital version of gold to its physical counterpart and the price of the precious metal to rise to $2,250 per troy ounce. At the same time, Robertsen emphasized that the proposed scenario is not a forecast, but only suggests a possible deviation from the current market consensus.

Galaxy Digital founder Mike Novogratz looked farthest into the future and saw a light at the end of the tunnel. In a comment to Bloomberg Television, he maintained his forecast that the price of the first cryptocurrency will rise to $500,000. However, it will now take more than five years for bitcoin, in his opinion, to achieve this goal due to significant changes in the macroeconomic situation and the aggressive actions of the Fed.