{kind=link}

Japan will update its CPI inflation data on Thursday at 23:30 GMT, with investors projecting a bold acceleration in the pace of price increases. Although the Bank of Japan (BoJ) keeps sticking stubbornly to its ultra-easy policy, recent comments disclosed willingness for a hawkish change. If the data intensifies the debate for an earlier exit, the rally in the yen could gain another leg.

Yen’s outlook is still fragile

It was a devastating year for the yen as the ultra-easy monetary policy in Japan forced investors to seek higher interest rates elsewhere to compensate for high inflation. The BoJ’s multi-billion-dollar FX intervention proved ineffective in stopping the yen from melting until a shift in Fed rate expectations came to the rescue – for free. Specifically, growing speculation that the Fed may use less aggressive rate increases to bring down inflation next year boosted the currency by more than 5% against the US dollar last week, making investors wonder whether the bad times for the yen have passed.

The problem now is that if the BoJ keeps defending its accommodative policy settings amid an uncertain global growth outlook, the yen could easily fall again on hard times. Speaking at a news conference last week, the BoJ chief Haruhiko Kuroda argued that there are signs of peaking inflation in the economy, telegraphing that a hawkish reversal is unnecessary.

A tweak in policy expected, but eyes on wage growth

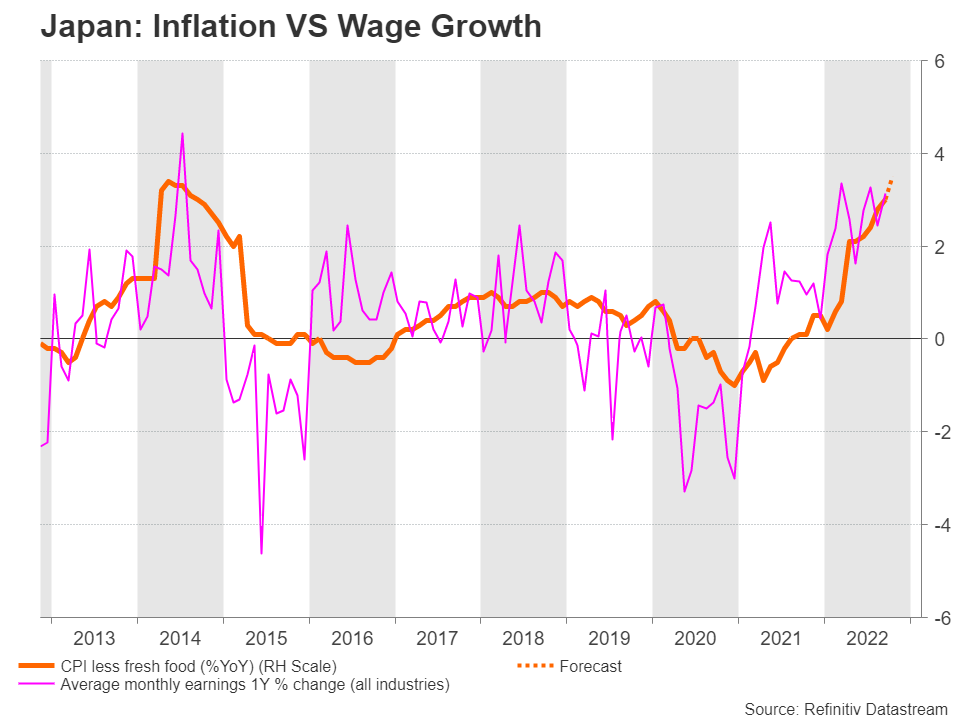

However, the latest summary of opinions showed that policymakers are now more open to the possibility of a policy normalization. Surprisingly, Kuroda himself backed the scenario of a flexible yield curve control in the future earlier this month, though only if inflation returns sustainably to the 2.0% target. However, unlike his counterparts in other advanced economies, he claimed solid wage increases might be a prerequisite for price stability.

Hence, wage negotiations in March, which involve talks between blue-chip firms and labor unions, could be vital before the central bank reviews any stimulus reduction plans. Note that Kuroda will not seek a reappointment when his term ends in April. Therefore, that could be a good timing for his predecessor to pilot monetary policy into the tightening era, especially if Rego, Japan’s largest labor organization, gets a green light for its 5% pay increase proposal.

CPI inflation

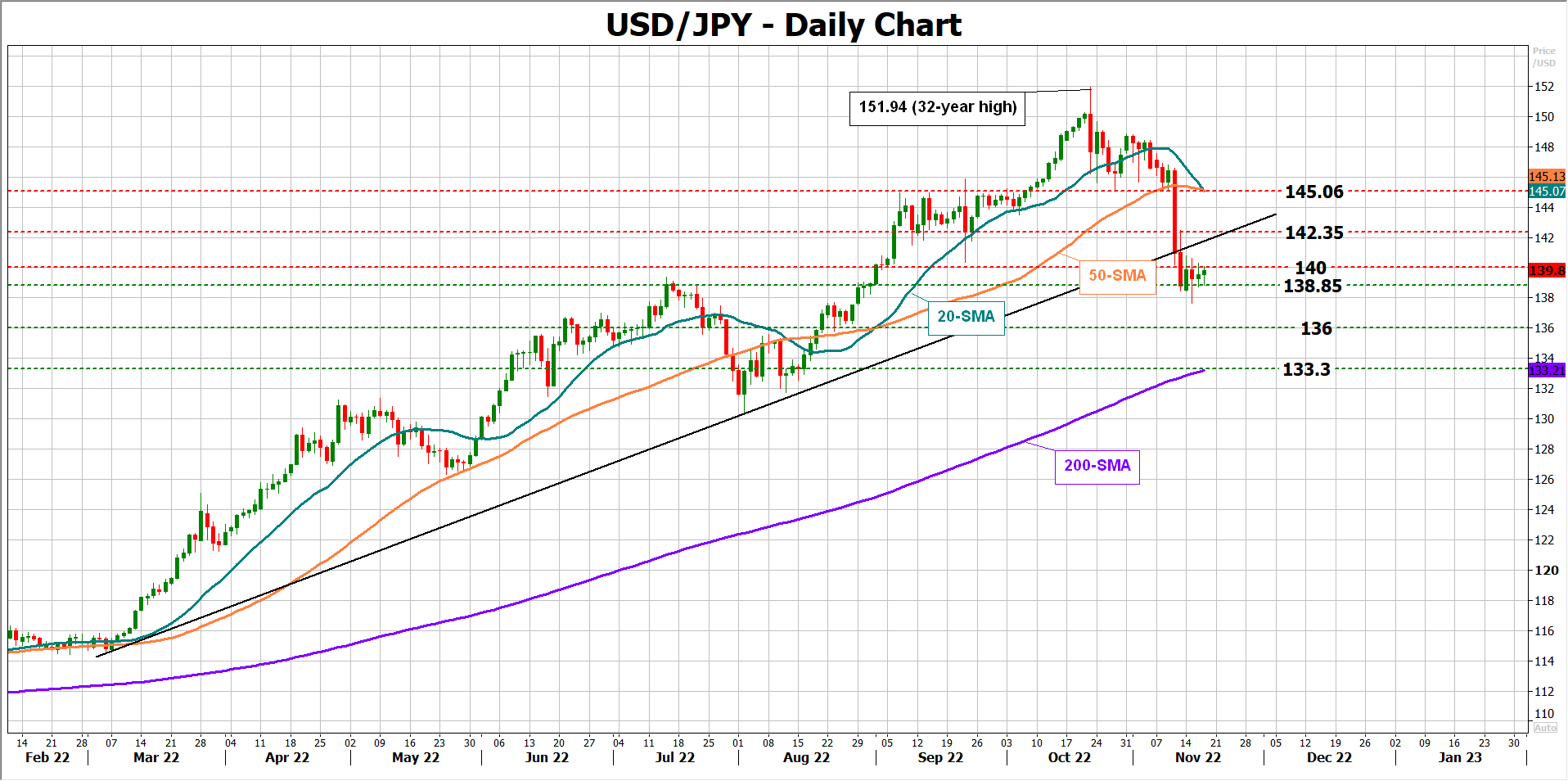

Still, some government officials have claimed that structural changes in wages can take a long time, and the central bank should not wait that long to exit stimulus. Another spike in the core CPI inflation, which is expected to have unlocked a new forty-year high at 3.5% y/y in October from 3.0% previously, may urge the need for an earlier policy shift. In this case, dollar/yen could breach the 138.85 base and slide towards 136.00. Even lower, the door will open for the 200-day simple moving average (SMA) and the 134.00 number. With the US dollar barely finding any fresh bullish catalysts these days, the yen could easily steal further ground.

Alternatively, a US-like downside surprise in the CPI would endorse Kuroda’s accommodative strategy as inflation is not that far above the BoJ’s 2.0% target. Consequently, dollar/yen could crawl back above the 140.00 level with scope to meet the 142.35 bar. A durable move above the latter may next pause near the 20- and 50-day SMAs at 145.00.