{kind=link}

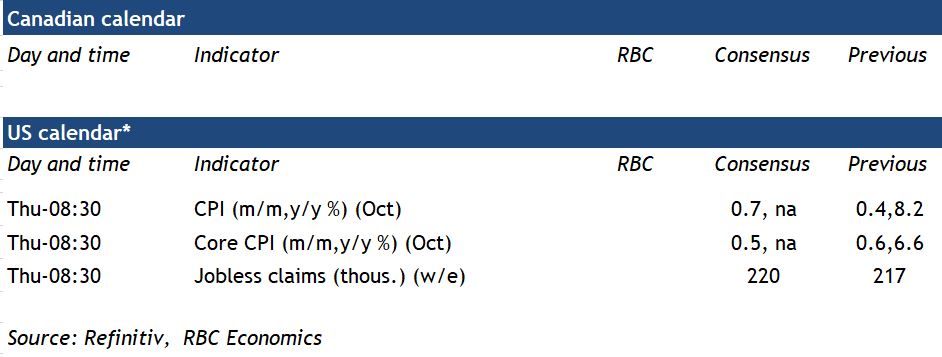

The next inflation reading from the U.S. will still be way too high to prevent another round of interest rate hikes. Year-over-year consumer price growth is expected to edge lower, to 8.0% in October from 8.2% in September. But that is despite an expected large 0.7% month-over-month increase. The price of gasoline rose 4% from October, reversing a 5% drop in September. And grocery prices likely continued to surge.

A 75 basis point interest rate hike from the Federal Reserve this past week took the fed funds target range to 3.75% to 4%. We expect at least another 50 basis point increase when the Fed meets again in December. But the inflation data will continue to be scrutinized for any signs of easing in broader price pressures that could allow the U.S. central bank to slow its pace of interest rate hikes going forward.

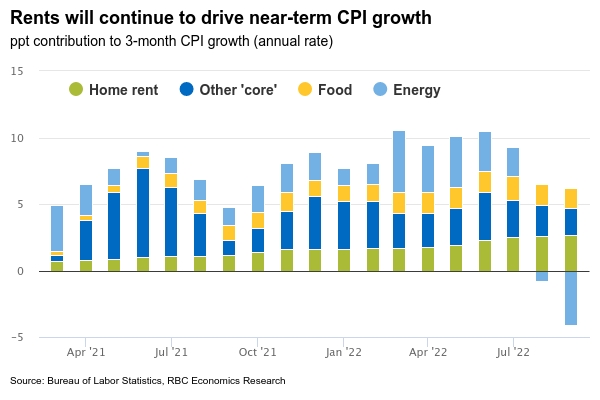

Core growth in the Consumer Price Index (a closely watched metric that excludes food & energy products) will continue to be fueled by surging home rents. Those gains are the result of earlier increases in market rental prices (there’s a lag as leases are renewed) that are still feeding through to higher household costs. But a pullback in more recent indicators of current rents mean those pressures will start to ease off in the year ahead.

There are early signs that higher interest rates are starting to cut into household demand, particularly for discretionary goods purchases. And wholesale used vehicle prices have been ticking lower after driving a disproportionate share of the initial surge in inflation. Still, by our count, almost 90% of goods and services in the CPI basket (excluding the shelter component) were still recording price growth above the Fed’s 2% inflation objective in September.

U.S. CPI growth probably peaked in June. But the Fed has further to go with risks increasingly tilted to the upside to our forecast that the Fed Funds rate will rise to 4.50-4.75%.