{kind=link}

Summary

- The Bank of England (BoE) raised its policy rate aggressively at today monetary policy announcement, raising its Bank rate by 75 basis points to 3.00%.

- However, there were also signals from the BoE that the pace of tightening will likely slow going forward. First, while all policymakers voted to raise interest rates, the size of the rate hike was not unanimous. The Bank of England also said policy interest rates could peak at a lower level than was priced into financial markets as of late October (albeit at the time that peak rate was expected to be around 5.25%).

- The central bank’s updated economic projections offer a clear indication as to why interest rates could rise at a less rapid pace than previously. The central scenario based off market interest rates sees a protracted recession and inflation undershooting its target over the medium term. Even in a scenario where interest rates hold steady at 3.00%, CPI inflation is forecasted to be only slightly above target in two years time.

- With the prospect of further fiscal consolidation also potentially weighing on the growth outlook, we now forecast slightly less tightening from the Bank of England than previously. We expect a 50 basis point rate increase in December and a final 25 basis point increase in February next year. That would see the policy rate peak at 3.75%.

- The combination of a protracted economic recession and a central bank that under delivers versus the market’s rate hike expectations are key factors behind our view of renewed sterling weakness into early 2023, with a targeted GBP/USD exchange rate of $1.0600 by the end of the first quarter next year.

Bank of England Delivers Jumbo Hike, Hints at Smaller Moves Ahead

The Bank of England (BoE) raised its policy rate aggressively at today’s monetary policy announcement, raising its Bank Rate by 75 basis points to 3.00%. The increase matched the consensus forecast. However, there were also signals from the BoE that the pace of tightening will likely slow going forward. First, while all policymakers voted to raise interest rates, the size of the rate hike was not unanimous. Seven policymakers voted for the 75 basis point increase, while one voted for 50 basis points and one voted for 25 basis points. Second, the BoE offered updated economic projections conditioned on the market’s interest rate expectations as of late October, which at the time saw a peak policy rate of around 5.25% by Q3-2023. In addition to raising interest rates and specifically referring to that 5.25% peak rate, the BoE said:

“Should the economy evolve broadly in line with the latest Monetary Policy Report projections, further increases in Bank Rate may be required for a sustainable return of inflation to target, albeit to a peak lower than priced into financial markets.”

The central bank’s updated economic projections do not make pleasant reading, and offer a clear indication as to why the BoE believes interest rates could rise at a less rapid pace than previously. Higher mortgage rates and tighter financial conditions are expected to weigh on economic activity. And even though the energy price cap means inflation should peak at a lower rate than previously, elevated inflation is still expected to weigh on incomes and growth for an extended period. Against this backdrop, the BoE’s central projections anticipate U.K. GDP declining for eight consecutive quarters, with a peak-to-trough decline of almost 3%. The BoE forecasts full-year 2023 GDP growth at -1.6%, and full year 2024 GDP growth at -0.9%. With respect to inflation, the BoE sees CPI inflation peaking at 10.9% year-over-year in Q4-2022, before slowing to 5.2% by Q4-2023 and 1.4% by Q4-2024.

The BoE’s alternative economic projections, based on a constant policy rate of 3.00%, are also quite illuminating. Under that scenario, U.K. GDP is forecast to fall by a smaller 0.9% in 2023 and 0.2% in 2024. Meanwhile, CPI inflation is forecast to slow to 5.6% in Q4-2023 and 2.2% in Q4-2024. With inflation only slightly above target in 2024, even under an assumption of constant interest rates, it’s possible interest rates may not need to rise too much further from current levels.

Softening Household Finances and Tightening Fiscal Policy to Weigh on the Economy

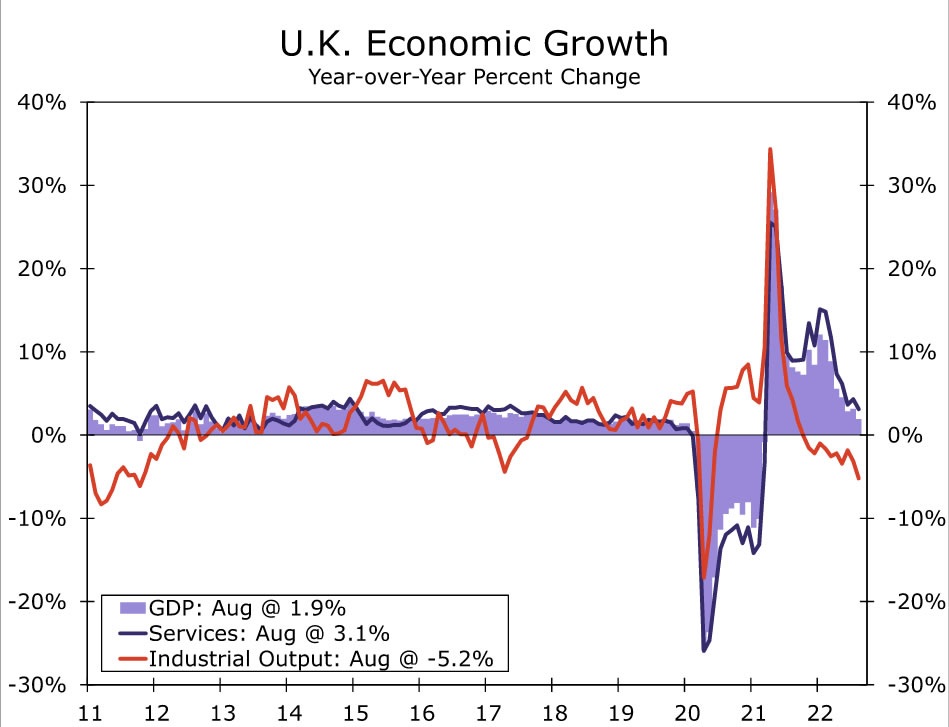

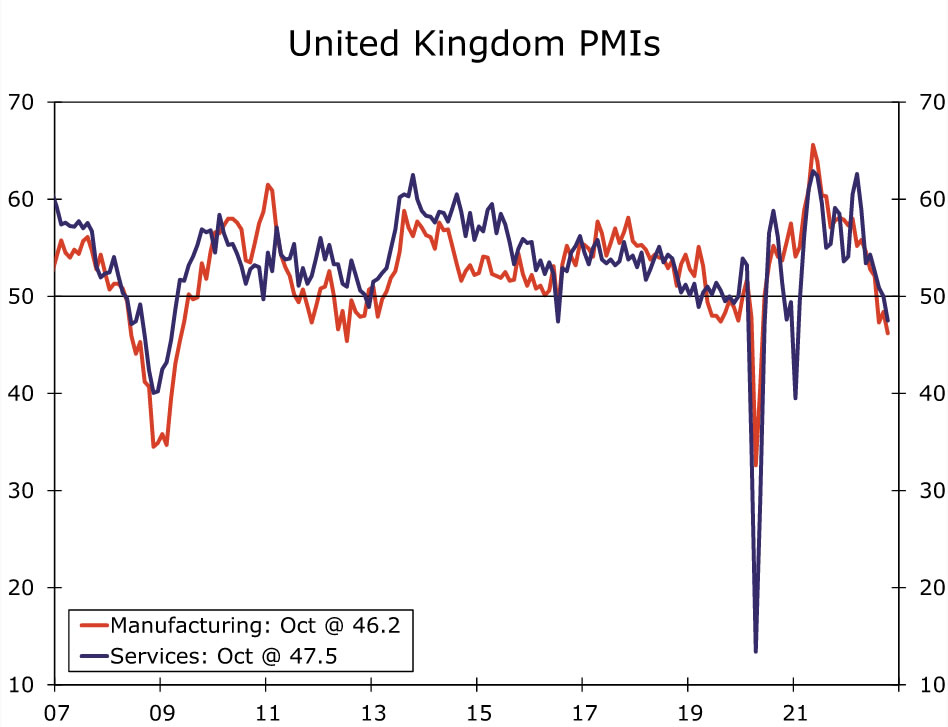

Recent indicators are consistent with the central bank’s underwhelming growth outlook. The economy has already shown a clear loss of momentum during the third quarter, as a small 0.1% month-over-month increase in July GDP was more than offset by a 0.3% decline in August GDP. While the August weakness was concentrated in manufacturing, with industrial output down 1.8%, services activity also dipped by 0.1%. In addition, the economy appears to have continued softening into the fourth quarter. The October services PMI fell sharply to 47.5, the first sub-50 reading since February 2021, while the manufacturing PMI also declined to 46.2.

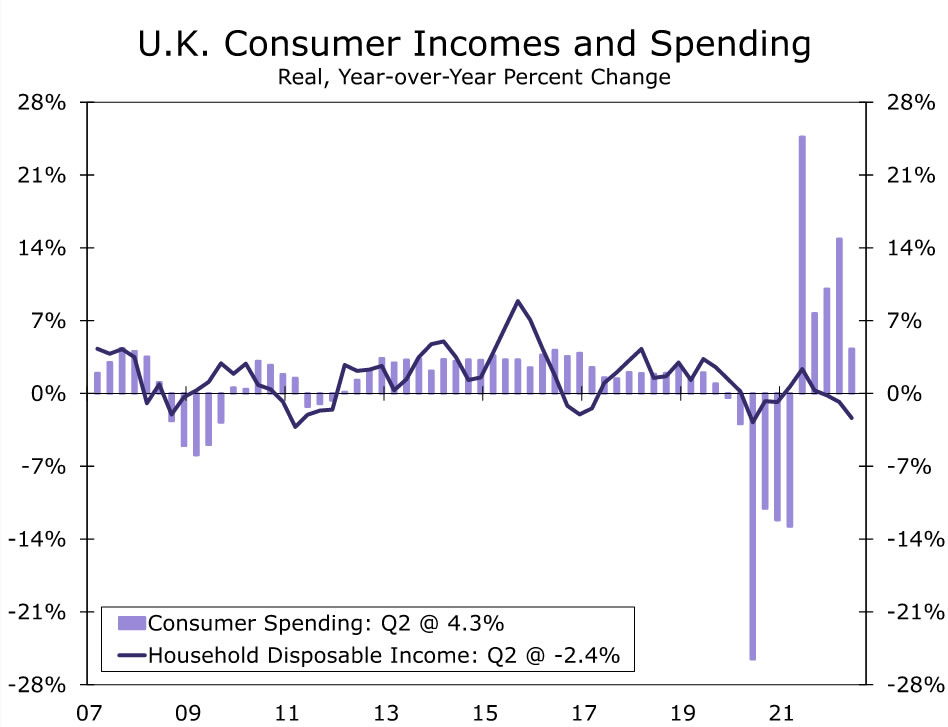

More generally, and as the Bank of England itself highlighted, softening household finances are likely to weigh on the consumer for an extended period. With price increases now outstripping income gains, growth in real household disposable incomes has turned negative for the past several quarters. Indeed, real household incomes fell 1.2% quarter-over-quarter in Q2, the fourth decline in a row, and are down 2.4% year-over-year. With CPI inflation having quickened further since, and given signs of slowing job growth (employment fell by 109,000 in the three months through August), further declines in real household incomes appear more likely than not.

Finally, the potential for fiscal consolidation could add to downside pressures on the economy and reinforce the downturn. The BoE’s forecast incorporate the government’s publicly announced fiscal initiatives as of October 17. These include a reversal of most of the proposals that were outlined in the Growth Plan in late September, as well as scaling back plans to cap energy prices for households. Previously the government said that energy prices would be capped for households for up to two years beginning from October 2022. However, new Chancellor Hunt subsequently said those plans would now only apply for six months through April 2023, with the intention to transition to a more targeted energy support package after that. However, media reports suggest the government will likely announce further fiscal consolidation measures at the Autumn Statement scheduled for November 17. Indeed, Prime Minister Sunak and Chancellor Hunt said it’s inevitable all Britons will pay more in tax. Analysts have suggested the government will announce a further £40B-£50B (1.75%-2.00% of GDP) of annual savings in the Autumn Statement, initiatives that would pose downside risks to growth.

Thus, while the BoE remains concerned about inflation, we ultimately believe a sharp economic downturn will be the key factor that brings the central bank’s policy rate increases to an early end, likely during the initial months of 2023. That would particularly be the case if CPI inflation shows signs of having peaked, or if there is a significant and sustained decline in wholesale energy prices. And with the prospect of further fiscal consolidation to be announced shortly, that could also rein in the extent of Bank of England tightening. In fact, following today’s announcement we now forecast slightly less tightening from the Bank of England than previously. We expect a 50 basis point rate increase in December, and a final 25 basis point increase in February next year. That would see the policy rate peak at 3.75%, which is still well below the peak of around 4.65% forecast by market participants. The combination of a protracted economic recession and a central bank that under delivers versus the market’s rate hike expectations are key factors behind our view of renewed sterling weakness into early 2023, with a targeted GBP/USD exchange rate of $1.0600 by the end of the first quarter next year.