{kind=link}

Fed Review: Another Hawkish 75bp Hike – We Now Expect 50bp also in February

- Fed hiked rates by 75bp as broadly expected. Powell delivered a hawkish message, emphasizing the need to tighten financial conditions further. We have not seen Fed make significant progress towards its goals over the past month.

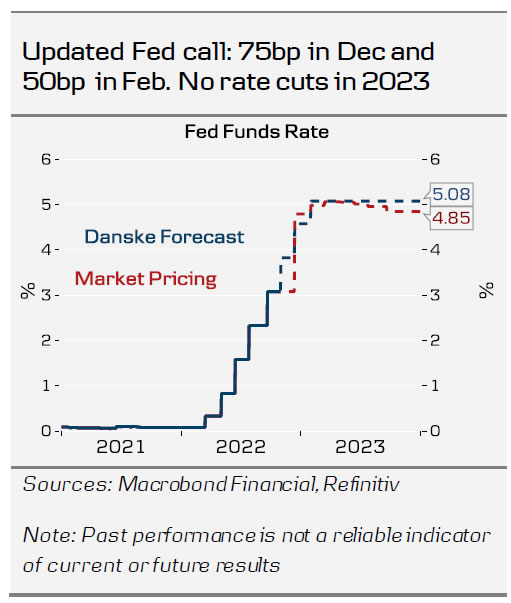

- Thus, we adjust our Fed call and expect a 50bp hike in February in addition to our earlier forecast for one more 75bp hike in December.

- Markets took the FOMC statement dovishly, but the move faded during the press conference and EUR/USD declined below pre-meeting levels while 2y UST yield rose around 6bp. We maintain our forecast for EUR/USD at 0.93 in 12M.

Fed hiked rates by 75bp in its October meeting as widely expected. There was no updated ‘dot plot’ or economic forecasts. While Powell did acknowledge the downside risks to the economy, he also emphasized that “is is very premature to be thinking about pausing”.

While there is uncertainty around the lag on how monetary policy tightening impacts the real economy, Powell emphasized that Fed is closely monitoring the development in overall financial conditions. As we highlighted in our Fed preview: Too early for a pivot, 28 October, we have not seen real financial conditions tightening over the past month, and instead inflation expectations have ticked slightly higher. Thus, Fed has not made any progress on its goals despite realized inflation continuing to surprise to the upside. We adjust our Fed call and now see the terminal rate at 5.00 – 5.25% after a 75bp hike in December and a 50bp hike in February.

Powell did not hint if there is a bias towards hiking either 50 or 75bp in December, but also noted that the terminal rate matters more than the exact pace of hikes. We agree, but also note that market is already pricing a decent (around 50%) probability for the 75bp hike, and from the perspective of maintaining financial conditions restrictive, Fed most likely does not want surprise markets dovishly in the current situation.

Powell was also clear on the asymmetric balance of risks in terms of policy tightening, which was already flagged in the September minutes. If Fed ends up tightening too much and causing a recession, it can very quickly also reverse its policy stance to more accommodative. But tightening too little risks inflation pressures becoming increasingly entrenched. Prolonged period of high inflation, tight monetary policy and constant need to push the terminal rate higher will eventually increase the risk of unnecessarily deep recession and a clear rise in unemployment. In other words, Fed prefers a short recession over years of stagflation.

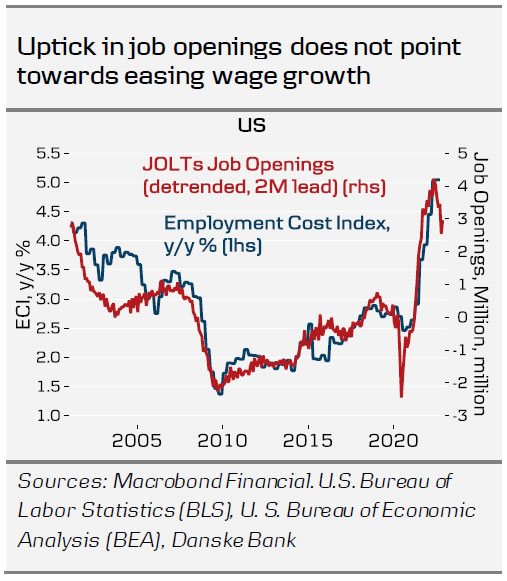

While Powell did not see a wage-price spiral right now, he also added that when it is evident, Fed has already failed. US wage inflation has remained above Fed’s target, and the JOLTs Job Openings (which is among the best leading indicators for wage growth) surprised once again to the upside in September. Fed is still faced with aggregate demand remaining too high especially in the labour markets, which leads to persistent and broad-based inflation. Fed needs to continue tightening financial conditions further, and it simply does not have the luxury of giving up on the hawkish stance to achieve this.