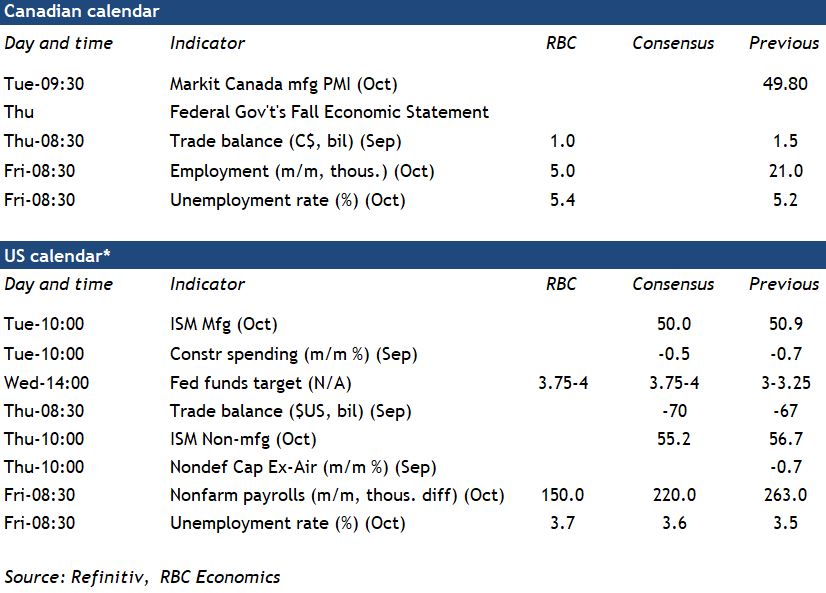

{kind=link}

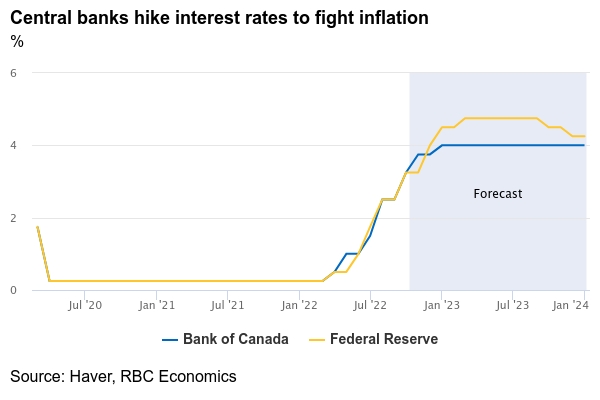

The U.S. Federal Reserve is likely to deliver another 75 basis point hike when it meets next week. The move will come on the heels of the Bank of Canada’s smaller-than-expected 50 basis point rate hike, which surprised markets this past week. And it will push the main U.S. policy rate slightly above the 3.75% overnight rate in Canada. Though comments from BoC Governor Macklem suggest Canada may be approaching the end of its current hiking cycle, the Fed isn’t likely to match that ‘dovish pivot’—at least not yet. Though we’ve seen some (very early) signs of inflation pressures easing in Canada, the same can’t be said of U.S. Indeed, core price inflation (which excludes food and energy), has been higher south of the border and more sticky.

Tamping down inflation will likely require more rate hikes in the U.S. than in Canada. Nevertheless, most Fed officials also expect the pace of those U.S. hikes to slow down after next week’s meeting. Our own forecast anticipates the Fed Funds rate entering the 4.5% – 4.75% range by early 2023. In Canada, we expect the overnight rate to reach 4% by year’s end. U.S. economic growth looks to be slowing—and that will eventually cut into inflation tailwinds. And though labour markets have remained exceptionally tight, there has been slight moderation in the number of job openings over the past few months. We expect employment growth will likely lose more momentum October. We expect a 150,000 increase in jobs alongside a tick higher in the unemployment rate, but to a still low 3.7%.

Labour markets aren’t exactly balanced in Canada either. But there are more signs of cracks forming, starting with 92,000 jobs lost over the last 4 months. We expect a 5,000 increase to Canadian employment in October, as hiring momentum (especially on the goods-producing side of the economy) continues to soften amid a cooling housing market and weakening demand for consumer products. That, together with a small rebound in the labour force participation rate, should drive the jobless rate back to August levels of 5.4%.

Week ahead data watch:

Next week’s Fall Economic Statement will be more fiscal update than mini budget as Ottawa forms its response to the U.S. Inflation Reduction Act. With a better-than-expected starting point for federal finances set against a deteriorating outlook, expect a follow-up on some of Budget 2022’s clean growth announcements—including the Canada Growth Fund and cleantech investment tax credit, as well as a plan to address carbon price uncertainty.

The Canadian trade surplus is expected to shrink again in September on lower oil prices.