{kind=link}

U.S. Highlights

- UK policymakers abruptly U-turned on its recently proposed “mini” budget, forcing Prime Minister Liz Truss to resign.

- Existing home sales fell 1.5% m/m in September to 4.7 million units. Sales have now fallen for eight consecutive months and are down 23% year-to-date.

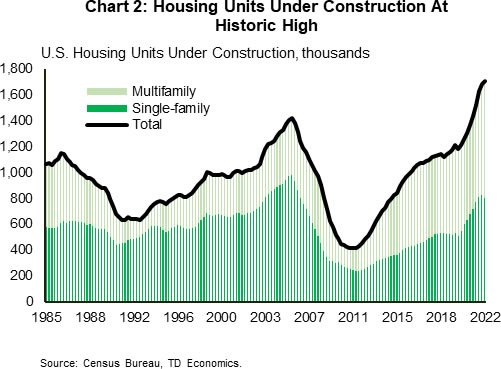

- Housing starts fell 8.1% m/m to 1.4 million units, with declines felt across both the single-family (-4.7% m/m) and multi¬family (-13.2% m/m) segments. The number of units currently under construction continued to edge higher, rising to a historic high of 1.7 million units.

Canadian Highlights

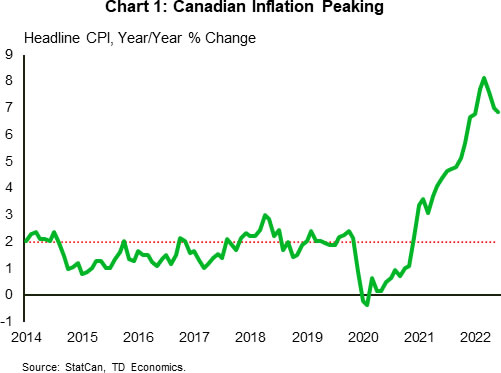

- Canadian consumer price inflation took a small step in the right direction in September, easing to 6.9% year-on-year, down from 7.0% in August.

- Worrisomely, the monthly inflation numbers showed a re-acceleration, with food and shelter costs proving more enduring.

- The Bank of Canada’s business and consumer surveys were also released, showing heightened fears that a recession will hit Canada in the next year.

U.S. – Hey Housing, How Low Can You Go?

This week brought some calming to global financial markets, helped along by UK policymakers abrupt U-turn on its proposed “mini” budget which had included £45 billion of unfunded tax cuts. UK Prime Minister Liz Truss resigned on Thursday, leaving the Conservative Party to elect a new leader sometime later next week. Yields on longer duration Gilts were down 50 basis points (bps) on the week, while the Sterling lost a modest 0.5% vis’-a-vis the dollar.

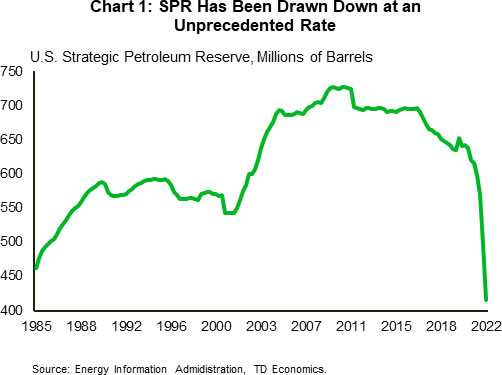

Investors also continued to digest last week’s CPI report, which led to further pressure on U.S. yields. At the time of writing, the 10-year has moved up an additional 30-bps this week to 4.3%, reaching both a new cyclical high and also the highest level since mid-2007. Top of mind on the inflation front, has been the recent turn higher in energy prices. Indeed, since peaking in July, gasoline prices had fallen by nearly 30% through mid-September. However, the recent announcement by OPEC+ members to pare back production quotas has led to renewed pressure on oil prices, which has also pulled gasoline prices higher. In an effort to provide some relief to consumers, the Biden Administration announced this week that they will be digging further into its Special Petroleum Reserve (SPR) and releasing an additional 15 million barrels in December. After including this week’s announcement, the cumulative release through December will total nearly 180 million barrels over the six-month preceding period. And its impact on gas prices cannot be understated. The U.S. Treasury estimated that the release of reserves to date has lowered retail fuel prices by as much as 42 cents per-gallon. That has come at the expense of an unprecedented drawdown in the SPR, which will eventually need to be topped up (Chart 1). According to the Biden Administration, this will happen once oil prices fall below $70 per-barrel.

The renewed pressure on interest rates has brought the housing market squarely back into focus. With the 30-year fixed mortgage rate now at 7.25%, buyer affordability has eroded to levels beyond the lows pre-dating the mid-2000 housing crisis. Demand continues to soften, with existing home sales falling 1.5% m/m to 4.7 million units in September and are now down 23% year-to-date. No reprieve appears to in sight, as leading indicators such as pending home sales and mortgage applications both point to further weakness in the months ahead.

The renewed pressure on interest rates has brought the housing market squarely back into focus. With the 30-year fixed mortgage rate now at 7.25%, buyer affordability has eroded to levels beyond the lows pre-dating the mid-2000 housing crisis. Demand continues to soften, with existing home sales falling 1.5% m/m to 4.7 million units in September and are now down 23% year-to-date. No reprieve appears to in sight, as leading indicators such as pending home sales and mortgage applications both point to further weakness in the months ahead.

Beyond the sales side, the combination of rising rates and elevated material costs has also heavily weighed on builder sentiment, with September housing starts falling 8.1% m/m in September. Declines were seen across both the single-family (-4.7% m/m) and multifamily (-13.2% m/m) segments, though the former has disproportionately accounted for most of the pullback year-to-date. Interestingly, the number of homes currently under construction remains at a historical high, as labor and building material shortages have significantly lengthen the time it takes to build a home (Chart 2). Perhaps most worrying is the fact that the number of single-family homes under construction currently sits at a 16-year high. With demand in this segment quickly receding, builders have already started reducing prices and adding additional incentives in an effort to attract buyers. However, with record amounts of new supply still in the pipeline, further declines in home prices are all but certain.

Canada – Inflation Leading to a Drop in Sentiment

It was a busy calendar for Canadian data this week. With CPI showing even greater persistence, we saw yields rise across the curve on changing expectations for the Bank of Canada (BoC). Adding even more colour to the inflation picture was the release of the BoC’s own surveys of business and consumer sentiment. Both showed heightened fears of a recession on the back of stubbornly high inflation. The BoC will have these reports in hand as it prepares for its forthcoming interest rate announcement next Wednesday.

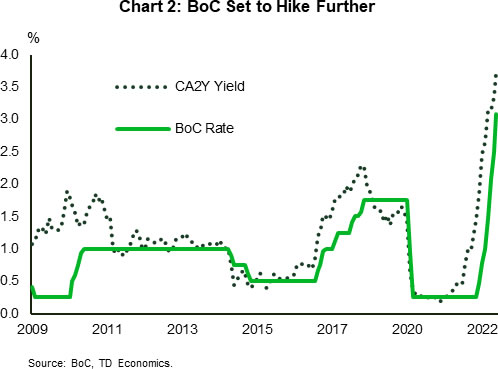

The release of the Canadian Consumer Price Index on Wednesday was the headliner on the economic calendar. As widely expected, the headline index declined on a year-on-year basis, reaching 6.9% in September, the lowest level since April 2022 (Chart 1). This decline occurred on the back of a 7.4% drop in gasoline prices. Though this was a welcomed sign, the underlying figures were not encouraging. On a month-on-month (m/m) annualized basis, the index increased by 4.8%, compared to 0.8% in August. This was driven by a 14.7% m/m gain in food prices and a 6.0% rise in shelter costs. Both of these factors are concerning. On the food side, there has been a re-acceleration in household staples like beef, poultry, and dairy products. Regarding shelter, the rise in mortgage interest costs is far outpacing the adjustment in house prices. Given the lags within the shelter component and the uncertainty regarding global food supplies, this raises the risk that inflation will take even longer to return to normal levels.

Inflation persistence has also had an impact on businesses. The Bank of Canada’s Business Outlook Survey showed a sizable drop in overall confidence, with the main index falling to a level of 1.7 in 2022 Q3, from 4.9 in 2022 Q2. Driving this was a deterioration in the outlook for future sales, with more than 50% of firms expecting a recession in the next 12 months. The culprit here is the belief that the BoC will go too far in its fight against inflation, with interest rates set to further dent housing activity and weigh on household consumption. This was echoed in the BoC’s parallel release of its Canadian Survey of Consumer Expectations. Here too, the economic outlook has dwindled, with most Canadian’s thinking a recession will occur sometime in the next year.

The BoC is set to hike interest rates by 75 basis points next week and provide an update to its outlook for economic growth and inflation (Chart 2). We will be keenly attentive to any change in the BoC’s inflation forecast given the impact this is having on sentiment. As we saw in both BoC surveys mentioned above, expectations for future inflation remain high. This should keep the BoC’s tone very hawkish as it needs to cement pricing for higher interest rates in order to bring down expectations for future inflation. Though the bank’s aggressive policy to date is starting to have an impact, as business inflation expectations are easing somewhat, there is still more to be done.