{kind=link}

U.S. Highlights

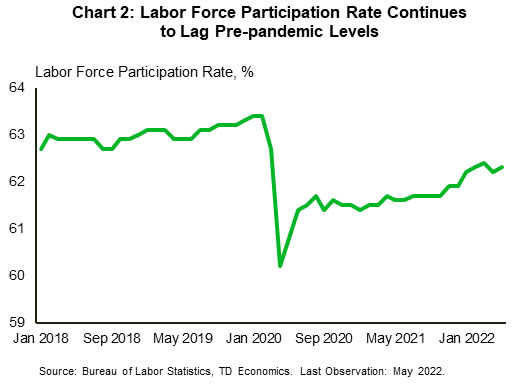

- The U.S. economy continued to add jobs in May, though at a slower pace than in the previous month. The unemployment rate held steady at 3.6% and the labor force participation rate edged up by 0.1 percentage point.

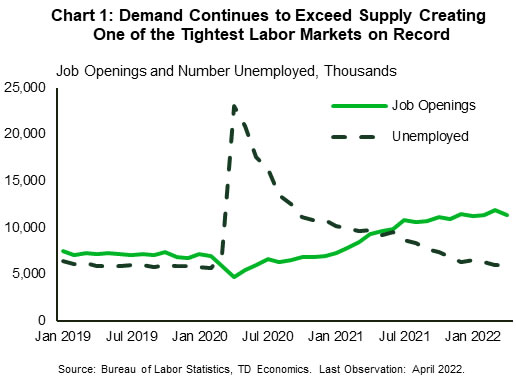

- Job openings remained elevated at 11.4 million, even while workers continued to quit their jobs. With job openings exceeding the number of unemployed workers, labor market conditions may remain tight for some time yet.

- Both manufacturing and services activity continued to expand in May, though services did so at a slower rate. Both sectors also felt the hiring pinch, as the availability of workers dwindled.

Canadian Highlights

- The Canadian economy posted a 3.1% annualized gain in the first quarter, disappointing expectations, but better than global peers like the U.S. and the European Union.

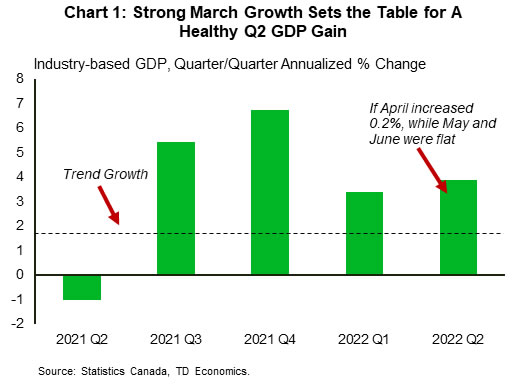

- There were some bright spots in the details of the GDP report that bode well for Q2 growth, including a 0.7% m/m gain in March. The household savings rate also increased, which adds some cushion for spending.

- The Bank of Canada lifted their policy rate by 50 basis points (bps) this week, taking it to 1.5%. The accompanying statement was aggressively hawkish, and we anticipate another 100 bps of tightening this year.

U.S. – Jobs Abound but Too Few Workers Around

This week marks the start of a new month and with it, the start of the Fed’s quantitative tightening program. As it tightens monetary policy to fight inflation, the Fed will allow up to $47.5 billion of its treasury and mortgage-backed securities holdings to mature this month without reinvesting the proceeds. The net effect should help to push rates higher and tighten financial conditions, helping ease price pressures.

The Fed’s Beige Book also reported that companies continued to struggle with rising prices and labor shortages during the spring, resulting in modest economic growth. The report notes however, that consumers are starting to push back on higher prices, thereby limiting companies’ ability to fully pass on cost increases. To deal with labor shortages some businesses implemented greater automation, offered more job flexibility, and/or increased wages.

Job opening data for April further reinforced the tight labor market narrative. There were 11.4 million job openings in April, a pullback from the 11.9 million record attained in the previous month, but still well above pre-pandemic figures. Churn in the market remained elevated with workers quitting their jobs 4.4 million times, little changed from the prior month. The number of job openings has exceeded the number of unemployed persons looking for work for much of the past year (Chart 1) as fewer persons are seeking employment relative to before the pandemic.

The trend is set to continue as the U.S. added 390k jobs in May, lower than the 436k in April but ahead of market expectations for 325k. Job gains were notable in leisure and hospitality, professional and business services, and in transportation. Notably, employment in retail trade declined. The unemployment rate held steady at 3.6% – close to the 50-year low of 3.5%. While the labor-force participation rate continued to recover at 62.3%, it was still below the 63.4% attained prior to the pandemic, thereby contributing to the labor supply slump (Chart 2).

The ISM manufacturing survey showed that activity in the sector continued to accelerate in May despite supply-chain and pricing challenges. The index came in at 56.1, exceeding April’s 55.4 print. New orders, backlogs of orders and the production index all rose, reflecting manufacturers’ struggles to keep up with above-trend demand for goods.

Conversely, while still in growth territory, activity in the services sector decelerated in May to 55.9 from 57.1. Despite new orders being higher on the month, business activity pulled back 4.6 points to a two-year low of 54.5. Services activity is expected to pick-up speed as summer progresses, though rising prices present challenges.

Despite current strong economic conditions, consumer confidence took a hit for the second consecutive month as high inflation soured the outlook. The Conference Board consumer confidence index dipped to 106.4 in May, from 108.6 in April, with both the present situation and the expectations index declining. Rising inflation, and measures to counteract it, may be putting a damper on consumers as they brace for the possible fallout.

Canada – GDP and BoC Headline Huge Week

It was huge week in Canada with the release of the first quarter GDP report, and the Bank of Canada’s interest rate decision. Canada’s economy managed a solid 3.1% annualized gain in the first quarter, supported by robust growth in household spending and surging residential investment. The gain was even more impressive when stacked against global peers, with real GDP contracting by 1.5% in the U.S. in Q1, and the EU squeaking out a 1.1% gain.

The print did disappoint market expectations, which called for even stronger growth. Still, there are plenty of signs pointing to another solid quarter in Q2. For starters, the household savings rate increased 1.2 ppts to 8.1%. This suggests a larger buffer for household spending to hold up in the face of inflation pressures and higher interest rates. In addition, service spending was restrained early in the quarter by lockdowns, and higher frequency data tracking lockdown-sensitive spending improved as the quarter progressed. In addition, GDP advanced 0.7% month-on-month in March – over three times faster than what is typically considered trend growth. If we assumed 0.2% growth in April (in line with Statistics Canada’s flash estimate) and flat output in May, and June, second quarter GDP would still be up more than 3% annualized (Chart 1).

Of course, not everything’s coming up roses in terms of second quarter growth prospects. The near 20% annualized surge in residential investment should give way to a decline in Q2, as higher interest rates have hit home sales hard. Meantime, net trade subtracted from growth in the first quarter. While exports declined, their monthly pattern indicates improving momentum heading into the second quarter. However, this story is even more pronounced for imports, suggesting they could outperform, which is negative from a GDP accounting perspective.

The Bank of Canada’s interest rate decision co-starred this week. To no one’s surprise, they lifted their policy rate by 50 basis points (bps) to 1.5%. What may have been slightly more eyebrow raising was the aggressively hawkish tone struck in the accompanying statement. Markets certainly took it that way, with bond yields climbing in the wake of the statement. Inflation was forecast to move even higher in the near-term. The Bank also noted that the risk of elevated inflation becoming entrenched had risen. On the economy, it was characterized as operating in excess demand with tight job markets leading to wage growth picking up and broadening out across sectors.

Policymakers didn’t mince words, noting that “interest rates will need to rise further”. We think another 50 bps of tightening will happen in July (even with some chatter of a possible 75 bps move), taking the Bank’s policy rate to the low end of its neutral range (Chart 2). Afterwards, a slower cadence is likely as the Bank assesses the impact of its tightening campaign.