{kind=link}

The Fed signaled that it will avoid shock-and-awe rate increases, putting more emphasis on avoiding a recession rather than vanquishing inflation. Another round of US inflation data is on tap next week and the Fed might finally get some good news, as the yearly CPI rate may have peaked. Is this the beginning of the end for the dollar’s supremacy? Maybe not.

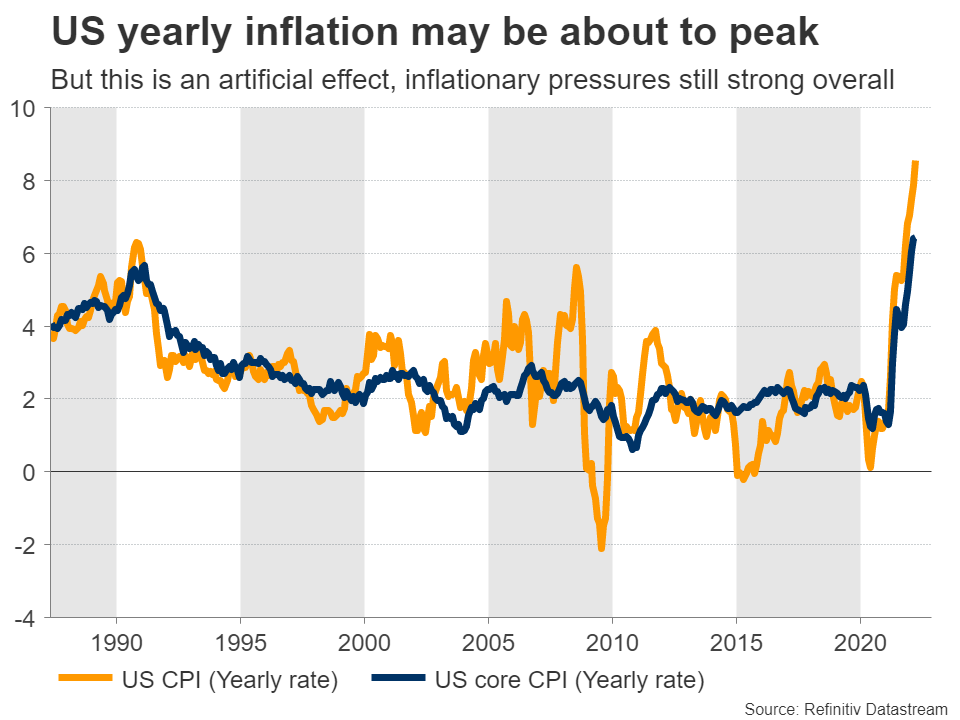

Inflation crest

The message from the Federal Reserve this week was much softer than feared. Chairman Powell shut down speculation for 75 basis point rate increases and even opened the door for a slowdown in the pace of tightening after the summer. The plan is to raise rates by a half percentage point another couple of times, and then reassess.

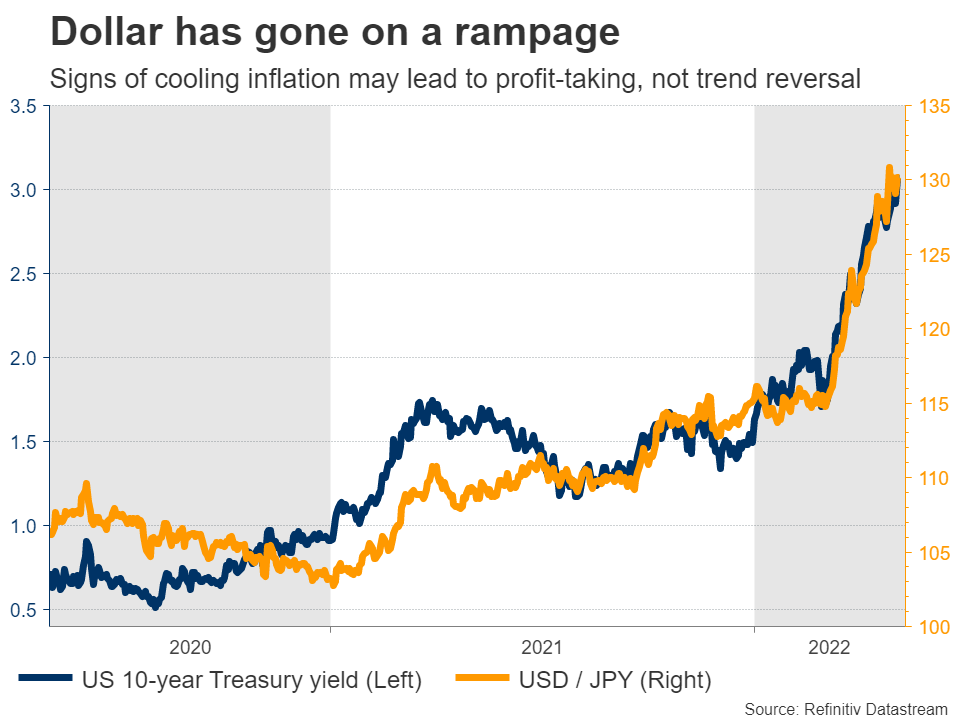

Money markets were priced for an even more hawkish trajectory, so this initially inflicted some damage on the mighty US dollar. However, the reserve currency quickly got back on its feet and started steamrolling the FX market again. The Fed told investors it will play it slow, as it doesn’t want to risk a recession by slamming on the brakes too hard.

Traders concluded that by not acting with sufficient force now, the Fed will need to do even more later to tame inflation. The market-implied probability for a 75 basis point rate increase in June, which Powell effectively ruled out, currently stands around 80%. Meanwhile, Treasury yields have stormed to new highs, particularly at the longer end of the curve. That’s the bond market telling the Fed that it is committing a policy error.

All this elevates the importance of the CPI inflation print for April, which will be released on Wednesday. Forecasts point to a monthly print of just 0.2%, which is far lower than recent months. It would be tempting therefore to believe that inflation has peaked, but this is not really the case.

Business surveys from Markit and ISM both suggest that inflationary pressures remained scorching hot in April, reaching new records in fact. Here’s the catch – this is when base effects from last year start to kick in. This period last year was when inflation really started to fire up, so as those strong monthly prints drop out of the 12-month CPI calculation, it becomes harder for the yearly rate to keep rising.

In other words, the monthly CPI forecast of just 0.2% seems like a lowball estimate from economists. However, any number below 0.9% – which is what will be dropping out of the calculation now – will still push the yearly CPI rate lower. It’s an artificial effect but it may be enough to calm some nerves around the inflation outlook.

As for the dollar, it has gone on a rampage lately, demolishing everything in its path amid a perfect storm of rising US rates, risk aversion, and slowing growth in the rest of the world. If incoming data dispel some concerns about inflation and traders dial back bets for rapid-fire Fed rate increases, the dollar could take a step back, but that’s unlikely to be enough to derail the overall uptrend.

An energy crisis has brought Europe to its knees, Chinese authorities remain committed to growth-crippling lockdowns, and the Bank of Japan has sacrificed the yen by doubling down on its yield curve control strategy. Until these dynamics begin to change and growth in other regions starts to pick up, it’s difficult to envision a trend reversal in the dollar.

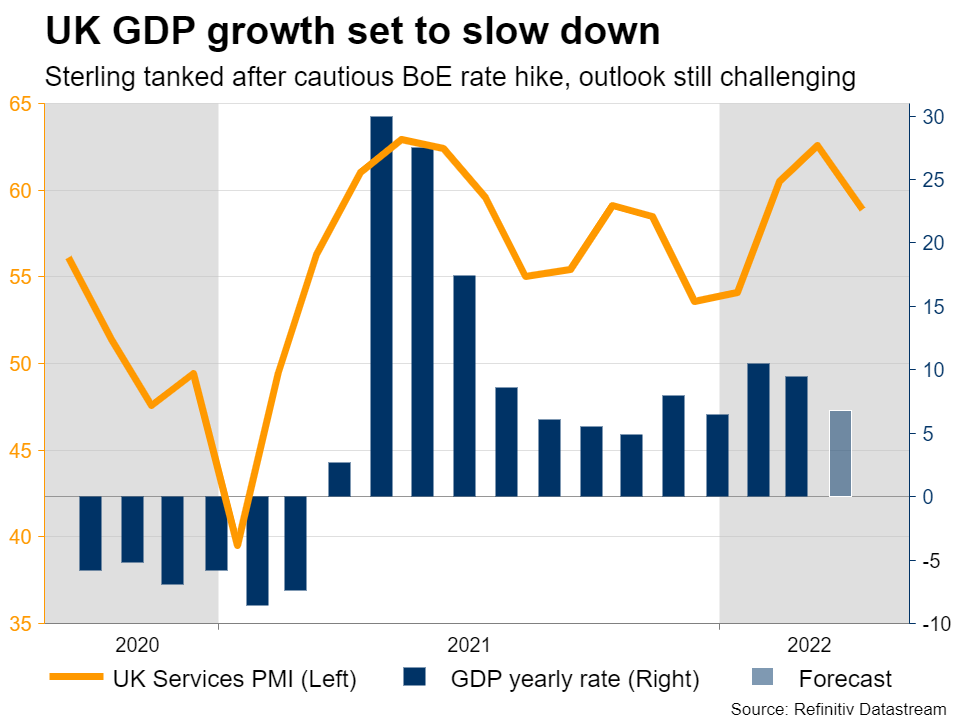

Sterling sinks ahead of UK GDP

In the United Kingdom, GDP stats for March and the entire first quarter are out on Thursday. The pound fell without a parachute this week after the Bank of England raised interest rates, but in a very cautious manner, opening the door for pausing the tightening cycle soon.

The overall takeaway was that downside risks around economic growth are intensifying, and the BoE is much more focused on avoiding a recession rather than fighting inflation. Markets responded by recalibrating the trajectory for UK interest rates lower, dragging Cable down to new two-years lows. The carnage in equity markets added fuel to this selloff.

Looking ahead, money markets are still pricing in another 5 quarter-point rate increases from the BoE for this year, which may be a little too optimistic considering the growing risk of a ‘pause’. In addition, volatility in stocks tends to hurt the pound given its sensitivity to global risk appetite, so the environment ahead seems challenging.

Chinese data in focus

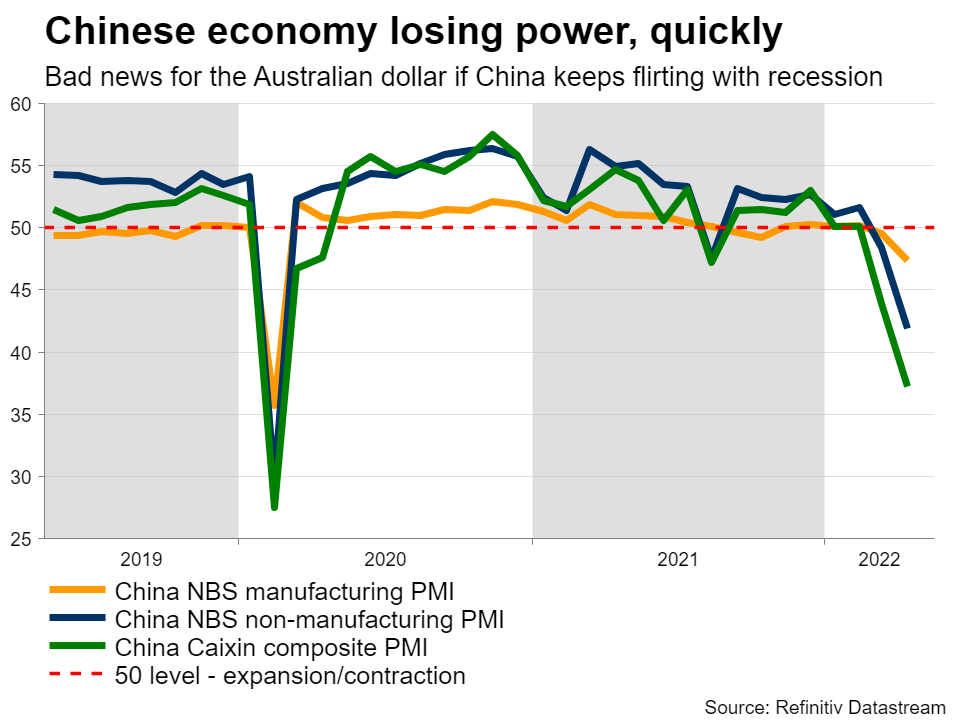

Crossing into China, trade data for April will hit the markets early on Monday ahead of inflation stats on Wednesday. Imports into the country imploded last month as major cities went into strict lockdowns and an even uglier print is expected this month, with imports set to fall 3% on a yearly basis.

This spells bad news for nations that rely on Chinese demand for their commodity products – most notably Australia. With the Chinese economy slowing down so dramatically, there will inevitably be some negative spillover effects on the Australian economy.

And yet, money markets are pricing in another 11 quarter-point rate hikes from the Reserve Bank of Australia this year. It would be a miracle if the RBA delivers anything close to that with China losing power, which suggests that the risks surrounding the Australian dollar remain tilted to the downside.

On a similar note, keep an eye on the Hong Kong dollar. It is currently testing the weaker band of its peg with the US dollar and local authorities will need to decide whether to defend that peg by burning through their FX reserves, or effectively abandon it. The Hong Kong economy is very weak, so following the Fed in raising interest rates is out of the question.