{kind=link}

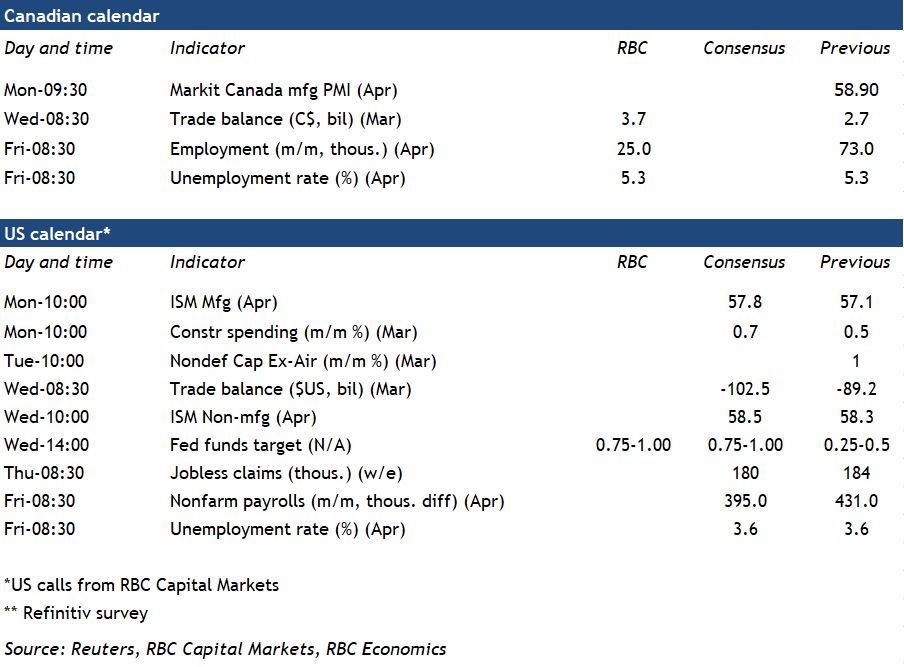

Canada’s April labour market report will top a flurry of data releases next week. We look for job growth to slow to 25,000 in April after a 409,000 surge over the last two months. Demand for workers remains exceptionally strong—job openings are running 70% above pre-pandemic levels—but the supply of available workers has shrunk dramatically. The unemployment rate hit its lowest level since at least 1976 in March at 5.3%. We expect a further pickup in employment within the hospitality sector from what are still very low levels. But as the pool of available workers dwindles, additional labour demand will have a greater impact on wage pressures than on employment counts.

Canada isn’t the only country battling a labour crunch. The U.S. unemployment rate is also very low and employment is expected to rise another 400,000 in April. A tighter squeeze in labour markets will add more fuel to the inflation fire as firms bid up wage prices to secure scarce talent. There are already clear signs that strong household and business demand is outpacing the U.S. economy’s domestic production capacity, further broadening inflation pressures. Against that backdrop, the U.S. Fed is expected to accelerate the withdrawal of monetary policy stimulus. A 50 basis point increase in the fed funds target range is expected following next week’s FOMC meeting, building on the 25 bp hike in March. We expect that to be followed by an additional 150 bp in rate hikes this year—with the risk that those hikes come sooner rather than later.

Week ahead data watch:

The April Canadian manufacturing PMI will be watched for signs that the Russian invasion of Ukraine and pandemic lockdowns in China are exacerbating global supply chain disruptions. Early flash estimates out of Europe and the US have held up reasonably well.

Canada’s merchandise trade balance likely improved in March, benefitting from an 18% surge in oil prices, with some offset from rising imports of consumer goods.