{kind=link}

The Bank of Japan concludes a two-day monetary policy meeting on Thursday and even though no changes are anticipated, its language on the exchange rate might prove decisive for the yen. As other central banks race to normalize policy amid the global spiral in inflation, the BoJ has stuck to its ultra-accommodative policy, stepping up its purchases of Japanese Government Bonds (JGBs) over the last month. But this has come at a cost as the yen has plunged to 20-year lows against the US dollar. Will the BoJ make any attempt to sound less dovish this week?

No inflation panic at the BoJ

Although Japan is not yet experiencing the same inflationary pressures as the United States and other countries, there is no question that prices are on the rise. The consumer price index hit 1.2% year-on-year in March – the highest since October 2018. Core CPI that excludes fresh food prices and is targeted by the Bank for its 2% goal rose by a more modest 0.8%.

This partially explains why the BoJ is a lot more relaxed about surging prices than its peers. Not only has inflation yet to reach 2%, but policymakers can afford to let it rise above target for a while after decades of deflation. The other reason is that Governor Haruhiko Kuroda is now the lone central bank chief that still thinks this episode of excessive inflation will be temporary. Only last week Kuroda reinforced his view that inflation in Japan is being driven mainly by the cost-push shock due to supply factors and therefore “lacks sustainability”.

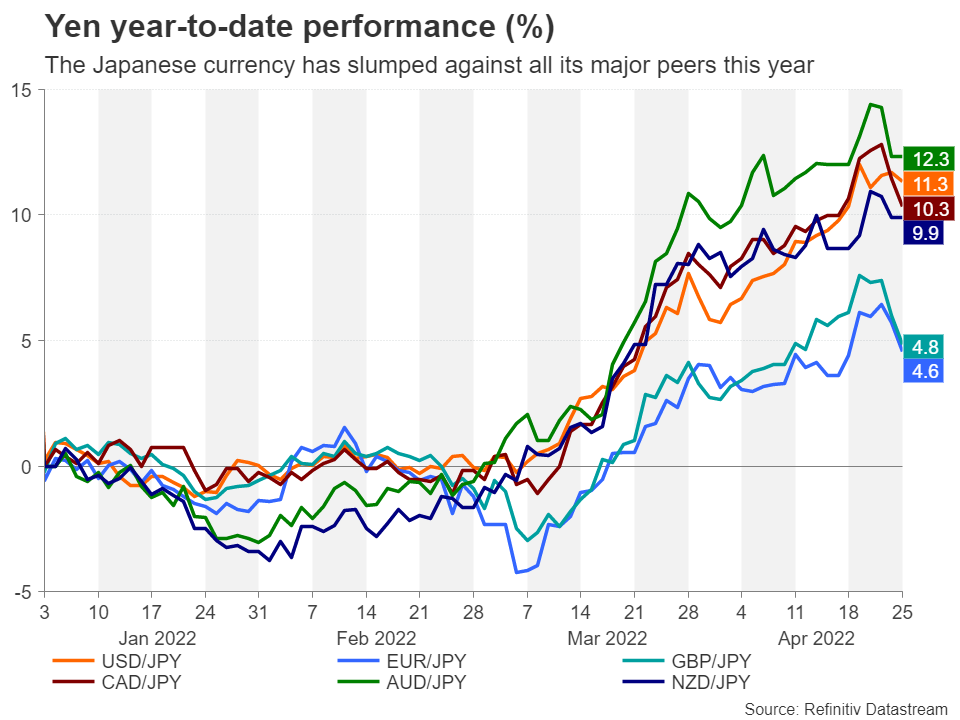

Weak yen: a new headache?

Until there is more evidence that higher inflation is becoming embedded into the economy, Kuroda is unlikely to change his stance. But if that risk alone is not enough to alter policy course at the Bank of Japan, another might. The yen has come under intense selling pressure since early March when the sanctions against Russia sent inflation expectations soaring and the government bond yields of major economies to multi-year highs, except of course for JGB yields.

The widening yield differentials, especially with the US, have been an unexpected headache for the BoJ. Kuroda is not particularly mindful of a weaker yen but the Japanese government is, putting him at odds with Finance Minister Shunichi Suzuki who decides on exchange rate policy. Japanese businesses have also been complaining about the slump in the value of the yen. Although exporters tend to benefit from a devalued currency, any benefits from cheaper exports are being negated by the increased cost of imports, which is additionally being exacerbated by the huge jump in energy and raw material prices.

All eyes on the forward guidance

It’s possible the BoJ will add something about the yen in its statement, to demonstrate that it is worried about a rapid fall in the currency. But what would send a more convincing signal to the markets that the Bank isn’t prepared to let the yen slide much further is an updated forward guidance that is less dovish.

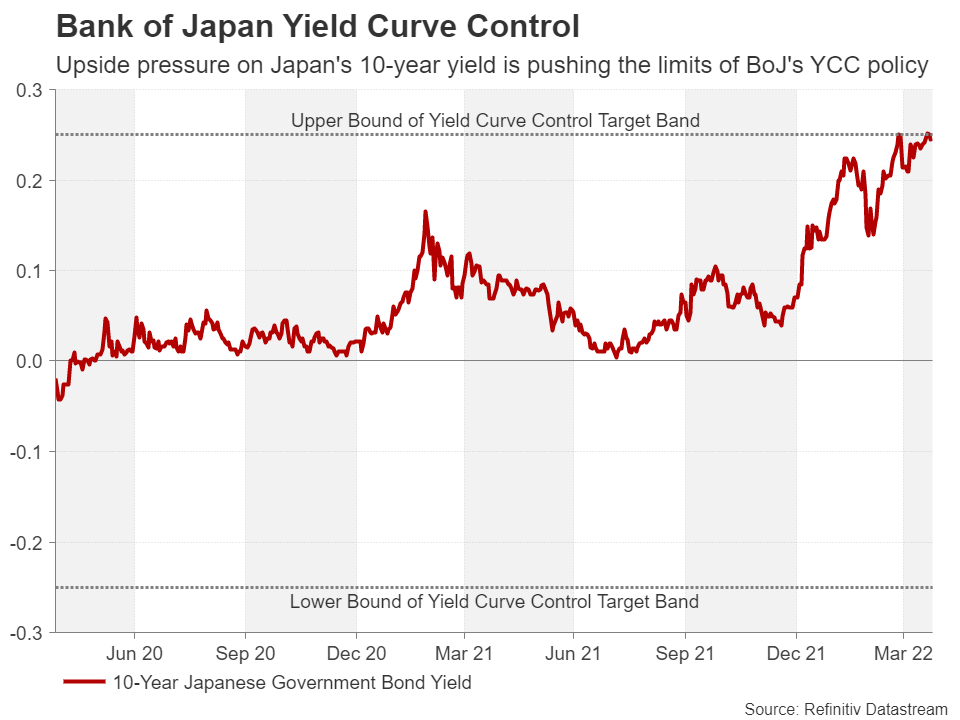

Even if Japan has some way to go before inflation turns into a big problem, it may not be feasible for much longer for the BoJ to pin the 10-year yield near zero per cent. Liquidity in the bond market is drying up fast as the central bank snaps up all the available JGBs. So maintaining its yield curve control policy in its current form may become impossible if yield spreads keep widening in favour of the dollar and other rival currencies.

Yield curve control may be tweaked

The BoJ may hint that it is open to allowing the 10-year yield to fluctuate within a wider range than the current target band of 25 basis points above or below zero. Another option is to switch the target from 10-year JGBs to shorter-dated bonds.

Although such policy tweaks would still leave the BoJ miles away from hiking its benchmark lending rate, which is stuck at -0.1%, they would nevertheless be a significant step towards normalization. Hence, there is scope for the yen to make notable gains on the back of a policy shift.

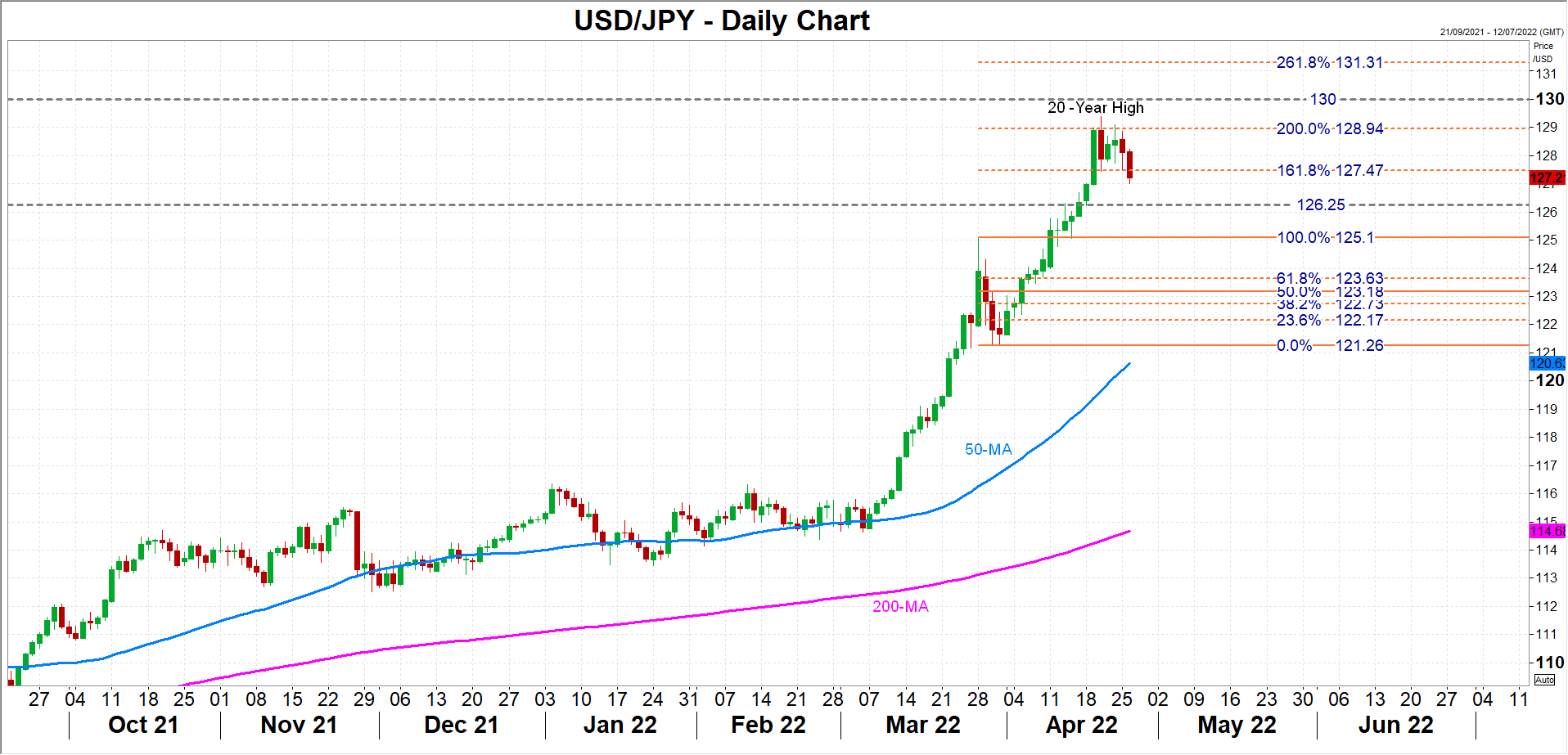

Yen has steadied, but 130/dollar remains within reach

The dollar has eased to just above the 127-yen level, as the Japanese currency has benefited from some safe-haven flows in the last few sessions. Should the pair retreat further, the 126.25 mark is a potential support area, otherwise, the decline could stretch until the March peak of 125.10.

However, if the BoJ decides to wait until its June or July meetings before telegraphing or announcing any policy changes, dollar/yen could resume its rally and aim for the crucial 130 level. The 200% Fibonacci extension of the March downleg just below 129 could obstruct any advances before reaching this point, while above it, the 261.8% Fibonacci of 131.31 would be the next target for yen bears.

Inflation forecast to be revised up

In the absence of any explicit signals, investors will have to search for clues in the BoJ’s latest quarterly outlook report. The Bank is expected to revise up its forecasts for inflation but will probably cut its projection for economic growth for the current fiscal year. However, what will matter more is whether policymakers put greater emphasis on the upside risks to inflation than on the downside dangers to growth as this would be a better indication on the pace of future policy tightening.