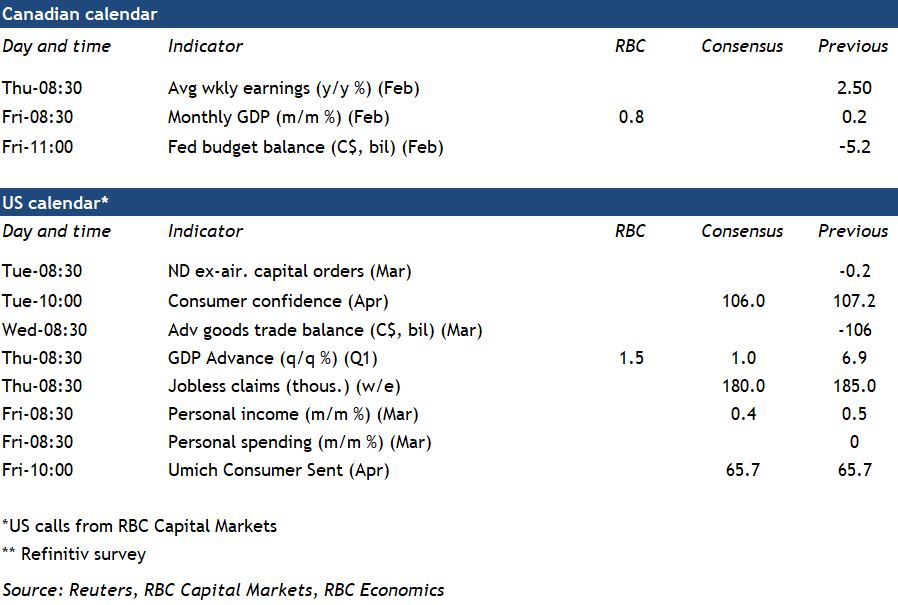

{kind=link}

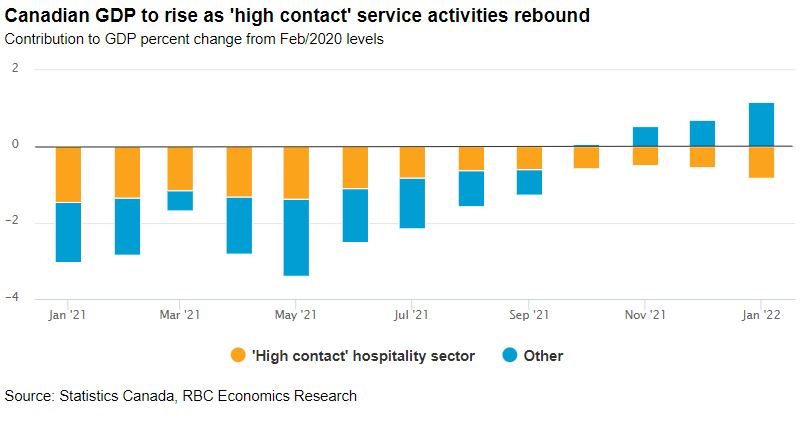

Canadian GDP for February is expected to post a month over month increase of around 0.8%—close to preliminary estimates. Retail sale volumes edged lower in February (down 0.4%), but the travel and hospitality sector rebounded sharply after slowing in January. Mining, quarrying and oil and gas extraction were also flagged as key drivers of growth in StatCan’s early estimate. Oil and gas drilling increased significantly in February and manufacturing sales volumes rose by 2.2% despite trade disruptions from border blockades.

The preliminary estimate of March GDP will also likely show another solid increase. Spending on travel and hospitality sectors continued to recover in March, coinciding with further easing in containment measures as well as periods of school breaks in provinces including Ontario and Quebec. Hours worked rose another 1.3% in March—and that’s after surging back 3.6% in February following a 2.2% drop in January. If anything, the 4.4% annualized increase in Q1 as a whole suggests an upside risk to our forecast for a 3.5% GDP gain in the quarter.

There‘s still some room for further recovery in those high-contact service sectors that were among the hardest hit during the pandemic. But for the most part, the rest of the economy is bumping up firmly against long-run production capacity limits. Labour shortages are exceptionally acute with the unemployment rate at its lowest level on records dating back to 1976. And inflation is surging higher. Pressure continues to grow for the Bank of Canada to ease off the monetary policy accelerator, with a 50 basis point rate hike in June (to follow up on the 75 bps over March and April) looking increasingly likely.

Week ahead data watch:

- Advance manufacturing sales (March): We expect a stronger 2.5% month over month increase for March’s advance manufacturing sales release next week. Oil prices are considerably higher but sales volume likely picked up as well, rising around 1% as auto production rebounded.

- We expect a 1.5% increase in US Q1 GDP – down from 6.9% in Q4 2021. Consumer spending is tracking a 4% increase and business equipment investment likely jumped higher. But a surge in imports and falling exports will leave net trade as a large subtraction.