{kind=link}

A barrage of economic indicators out of Europe and America will put the spotlight on the euro and US dollar next week. The data could further reinforce the diverging paths of monetary policy between the Federal Reserve and European Central Bank. European traders will additionally be keeping a watch on the outcome of the French presidential election, while RBA policy could come under scrutiny too as Australia publishes quarterly CPI numbers. But it is the Bank of Japan that could attract the most attention as it is set to keep policy unchanged even as the yen plunges across FX markets.

Euro hoping for inflation and Macron boost

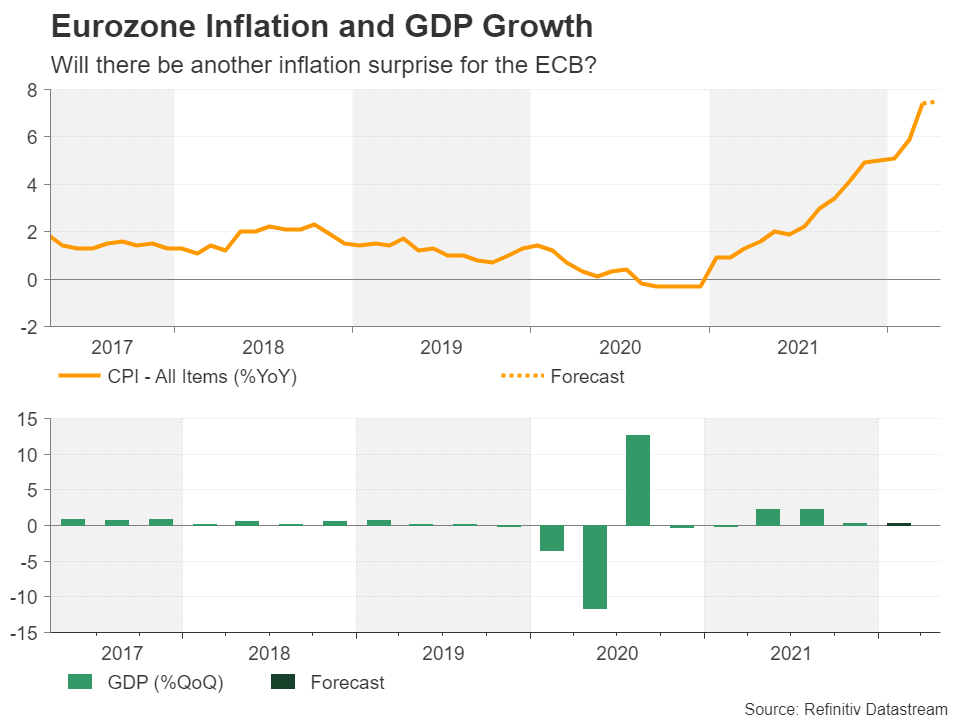

Inflation in the euro area hit the highest on record in March, jumping to 7.4% year-on-year. It is expected to have heated up further in April when the flash estimates are released on Friday. The preliminary readings on GDP growth in the first quarter are also out the same day. The Eurozone economy likely notched up moderate growth over the period, but investors will be sensitive to any unexpected weakness given the dimmed outlook for the rest of the year.

Earlier in the week, investors will look to Germany’s Ifo business sentiment gauge on Monday and the Eurozone’s economic sentiment index on Thursday for evidence that the decline in business optimism accelerated in April under the strain of the Ukraine and cost of living crises.

However, if the polls are right, there might be some good news for the euro on Monday when markets wake up to the result of the French presidential election. French voters will decide on Sunday whether incumbent President Emmanuel Macron should get to serve a second term or if it’s time for a change. Far-right leader Marine Le Pen saw her popularity surge in the run-up to the first round, but Macron’s lead has since started to widen again, suggesting a comfortable enough win.

The euro, which was temporarily bolstered in the past week by growing talk of a July rate hike by ECB policymakers, could catch a bid again if the CPI numbers are stronger than expected and Macron is victorious. But US data will be just as important for driving the euro/dollar pair.

PCE inflation to headline packed US data week

Durable goods orders for March will kick off the US agenda on Tuesday, alongside new home sales and the consumer confidence index for April. The closely watched survey is expected to slide for the fourth straight month in April, falling to 106.0. Pending home sales will follow on Wednesday and on Thursday, the advance GDP estimate for Q1 is due.

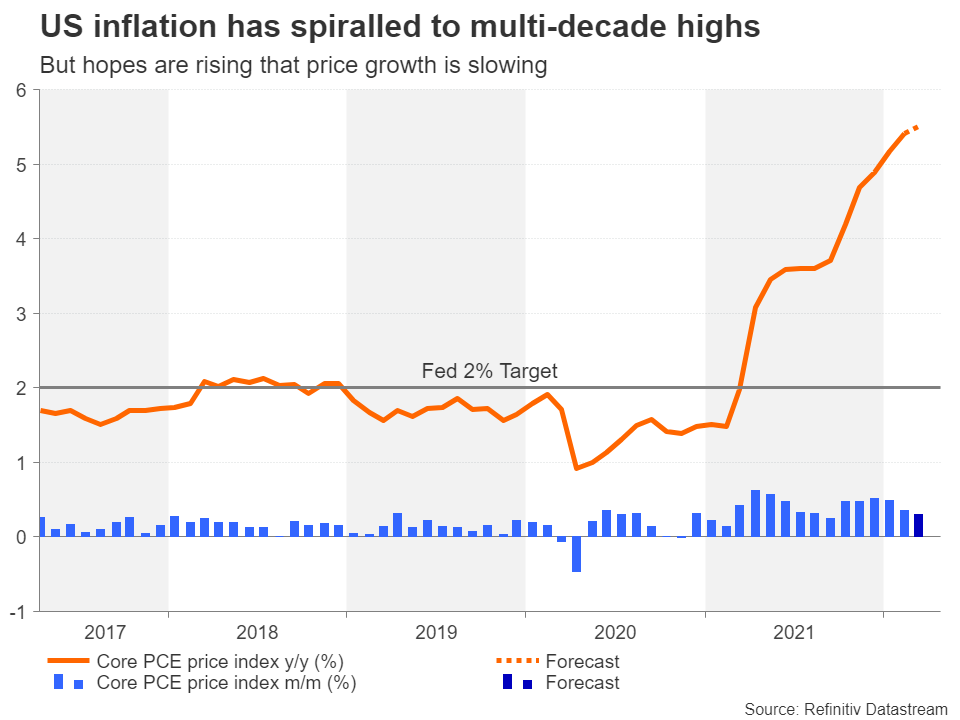

GDP growth likely slowed substantially in the first three months of the year, with analysts forecasting annualized expansion of 1% compared to 6.9% in Q4. However, Friday’s data on March personal income and spending, as well as the core PCE price index will be just as crucial for assessing the health of the American economy.

Consumption is expected to have picked up in March, rising by 0.7% m/m, which if confirmed, would suggest there was little impact from the heightened geopolitical tensions on US consumers. Moreover, the core PCE price index is projected to have edged up just 0.1 percentage points in March to 5.5%.

Following the slight miss in the core CPI print, a similarly softer-than-anticipated reading in the core PCE measure might add to hopes that inflation in the US has started to peak.

Such sentiment would probably be good news for Wall Street but could hurt the US dollar, which is back at two-year highs after Fed Chair Powell’s very hawkish comments.

Bank of Japan meeting could be a difficult one

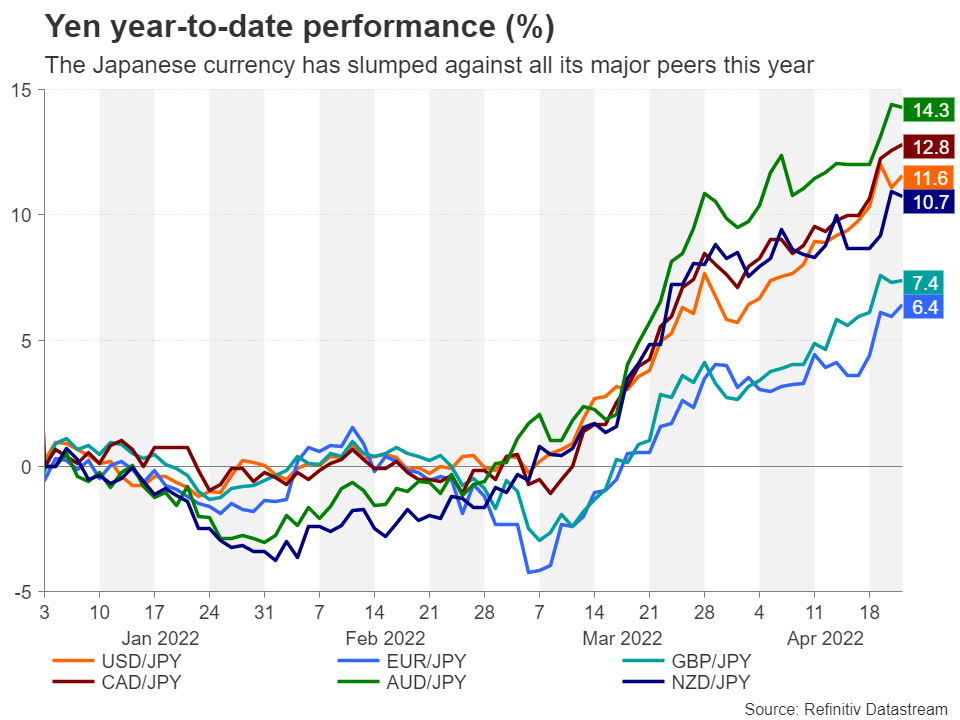

The Bank of Japan will announce its latest policy decision on Thursday and the meeting could be an important one even though the chances of a policy shift are remote. Inflationary pressures are slowly building up in Japan as input costs soar from higher energy and raw material prices. But the pain on businesses is being exacerbated by the yen’s dramatic slump over the past two months.

The government is increasingly edgy about the yen’s “somewhat rapid” decline, but investors aren’t as convinced by Governor Haruhiko Kuroda echoing the same concern. That shouldn’t come as a surprise when the BoJ’s response to the latest inflation scare has been to double down on its yield curve control policy rather than abandon it.

The Bank ramped up bond purchases at the end of March when its upper cap on the 10-year JGB yield came under attack. Not only that, but it also pledged to conduct additional market operations in the current quarter to defend its yield target.

The question now is how much longer the BoJ will be able to maintain this policy when the yen’s depreciation is fast becoming a hot political issue and there’s a real prospect of inflation overshooting the elusive 2% price target.

The Bank will probably revise up its inflation forecasts in its quarterly outlook report. But investors will be more interested to see what tweaks, if any, policymakers will make to their forward guidance and to the language on the exchange rate in the statement.

The yen could be in store for a major rebound if there’s any hint of the yield target band being calibrated soon.

On the data front, it will be quite busy with the jobless rate for March out on Tuesday, followed by retail sales and preliminary industrial output figures on Thursday.

Australian CPI to fuel RBA rate hike bets

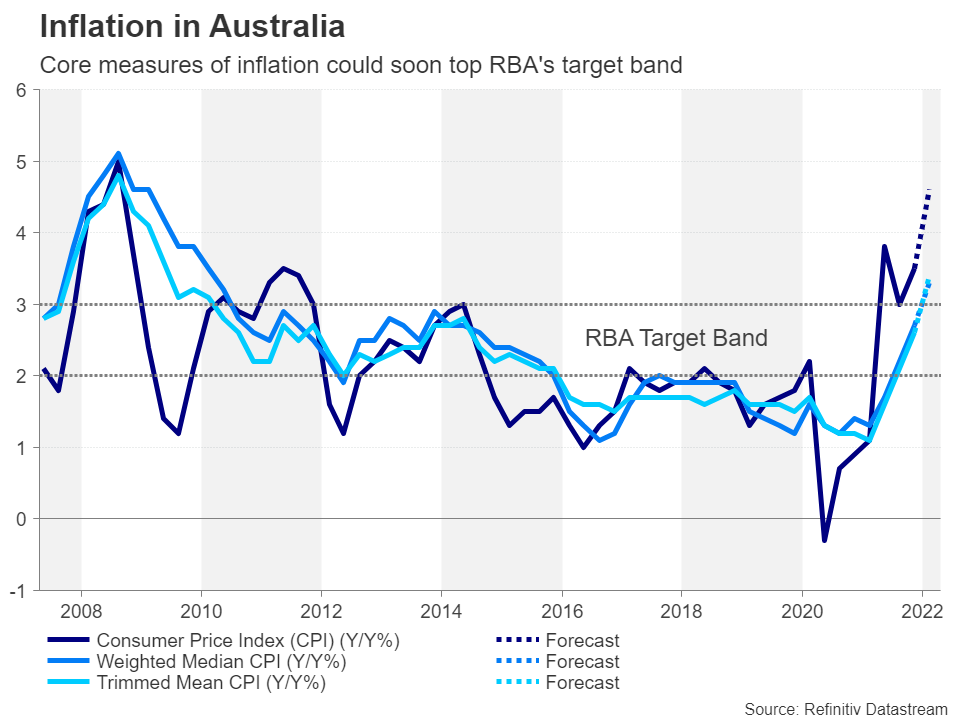

In Australia, the consumer price index readings for the March quarter are due on Wednesday. Both the headline and core rates are expected to exceed the Reserve Bank of Australia’s 2-3% target band. The last time the weighted median and trimmed mean CPIs were above 3% was in 2010 so this would be quite a significant development for the RBA.

Policymakers have only recently started to flag that a rate hike could be imminent, with markets fully pricing in a 25-basis-point increase in June. If the inflation numbers are much higher than expected, speculation of a rate hike as early as the May meeting could gather steam, boosting the Australian dollar.

However, even if there is a strong case for a move in May, the RBA will probably want to avoid taking any action before the federal election that’s been set for May 21.

The inflation theme will continue on Thursday and Friday with the release of export prices and the producer price index, respectively.