{kind=link}

The euro is having a tough time as it remains heavily dependent on the risky Ukrainian war factor. Prospects for an economic recession are growing larger, but with inflation soaring at the same time, the European Central Bank (ECB) has recently talked more about higher interest rates. On Thursday at 12:30 GMT minutes from the March policy meeting could shed light on how keen the central bank is to switch to a tightening regime. The report, however, may not be surprising enough to erase the latest pullback in the common currency, but it could still set sentiment for the next policy gathering.

Inflation is the priority

Back in March, the ECB held its policy settings unchanged as widely projected given the confusing economic backdrop in the bloc. While everyone expected a huge emphasis on the Ukrainian war and its growth impact on the Eurozone, a majority of policymakers appeared relatively more nervous about inflation. The central bank raised its 2022 price forecast to 5.1% from 3.2% previously, citing the price shocks stemming from the Ukraine-led supply disruptions. In the worst-case scenario, inflation would jump to 7.1% but economic growth would shrink only to 2.3% from its already lowered baseline case of 3.2% expansion.

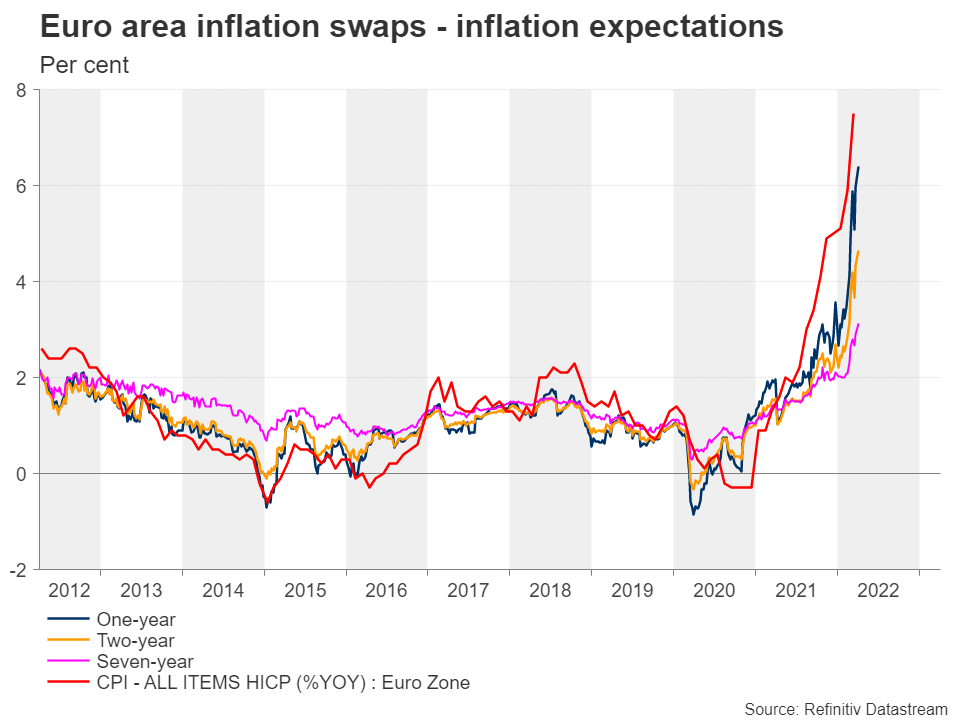

In addition to energy costs, prices in other essential sectors such as food and manufacturing are spiraling by more than 2.0% as well. Inflation swaps have already shown a record surge in price projections and the latest CPI report displayed a new all-time high of 7.5% y/y in March. Hence, sitting on its hands does not seem to be a safe option for the central bank anymore, and something needs to be done before consumers see their pockets emptying because of the higher cost of living.

ECB set to switch to a tightening regime

Apparently, hiking interest rates without notice could also damage business and consumption confidence amid rising growth anxieties. Hence, during the March meeting, the central bank took a safer path by presenting a quicker reduction in the regular APP asset purchase program to €40bln in April, €30bln in May, and €20bln in June, while strikingly signaling the end of the asset purchase program at some point in the third quarter. Consequently, the hawkish message bolstered expectations that a rate hike could be the next step in the tightening phase at the end of the year. However, when, and how fast the rate hike cycle will develop is still unknown and investors will carefully read the minutes for some clarity.

Perhaps the ECB will prefer to keep such information hidden for now to avoid any unpleasant sharp market movements. Nevertheless, some policymakers including the most conservatives ones in Germany, the Netherlands and Austria, are now openly discussing the possibility of scaling back the extraordinary stimulus, with the Belgian ECB chief Pierre Wunsch saying this week that interest rates could rise back to zero this year. Therefore, investors could still use any insightful details from the minutes to figure out how strong the hawkish voice is growing within the central bank and how real the scenario of five rate hikes priced by futures markets is.

ECB meeting minutes may not save the euro

The impact on the euro, however, could be negligible since the rate hike pricing is already too aggressive for the Eurozone given the Ukraine uncertainty, and the minutes could add little new information to that. Moreover, policymakers are not expected to vote for any rate increase unless the coming data proves that the economy can absorb higher borrowing costs.

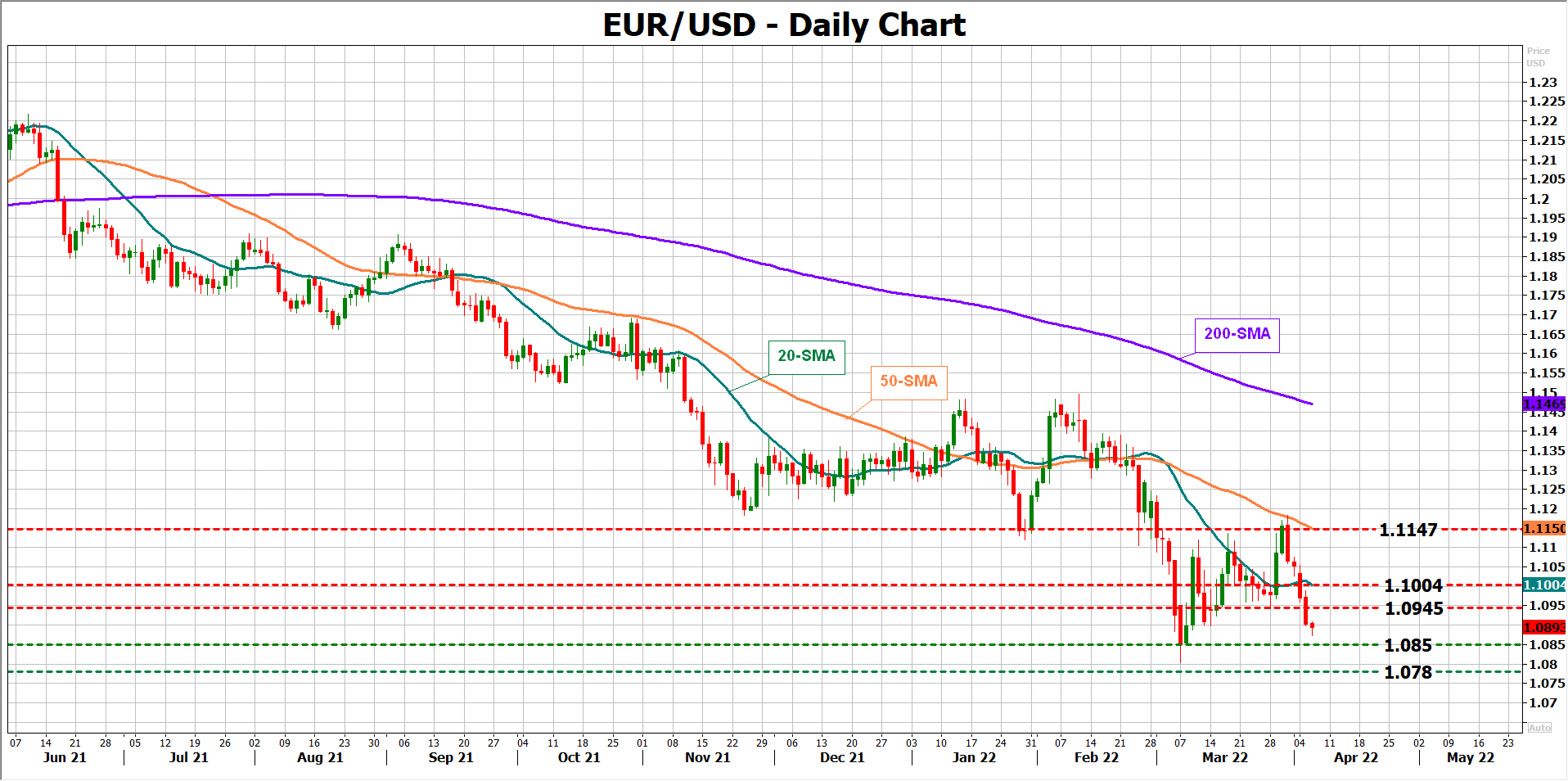

From a technical perspective, the outlook for euro/dollar is currently poor. The pair has already erased the sharp rebound at the end of March, sliding to a one-month low of 1.0873 early on Wednesday. The 1.0850 – 1.0800 area could be the last opportunity for a rebound before the broad negative trend extends towards the 1.0780 support level and then to the 2020 low of 1.0636.

Alternatively, the pair will need to pierce the 1.0958 – 1.1000 zone to gain access to the 50-day simple moving average (SMA) at 1.1147.