{kind=link}

A jam-packed week for central banks and economic releases is coming up as the inflation story continues to grip the markets. With the price data pointing up and bond yields fired up, investors are expecting nothing but hawkish talk from the Federal Reserve and the Bank of Canada. The latter could even go one step further and put words into action. In Europe, though, all eyes will be on the flash PMI readings where Omicron likely weighed on economic activity in January. Down under, CPI figures for both Australia and New Zealand should direct some of the rate hike buzz towards the aussie and kiwi.

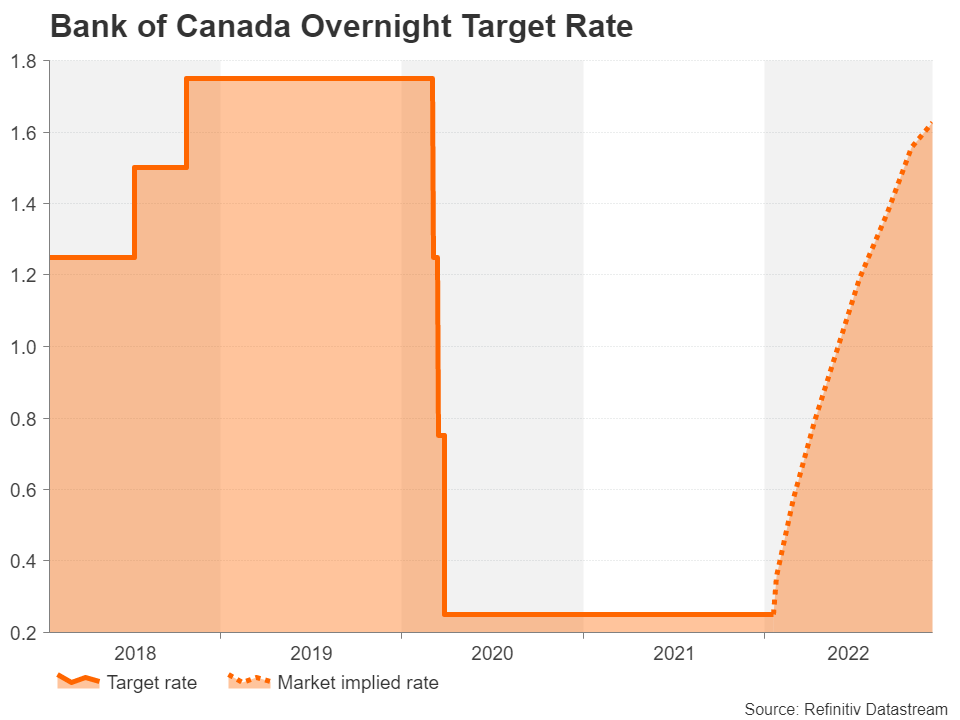

BoC rate hike: no point in waiting

The Bank of Canada will be the first major central bank to hold its first policy meeting of 2022 on Wednesday and it’s looking like it will be an exciting one. Rate hike bets have been intensifying all week and a 25-basis-point increase is now about 85% priced in. Expectations of a move as soon as the January meeting were reinforced by the latest CPI data that showed annual inflation hit a 30-year high of 4.8% in December.

At the last meeting, the BoC had reiterated its view that the first rate rise is unlikely to come before April. But now that inflation is clearly surging and perhaps more importantly, the Fed is now leading the hawkish camp and the BoC is no longer the lone wolf, there’s less of a danger that an earlier-than-projected rate hike would be seen as a misstep.

The problem for the Canadian dollar, however, is that a non-telegraphed rate increase might not provide much of a boost when it’s already been anticipated by most investors. If the BoC does indeed raise interest rates on Wednesday, it would need to back it up with some very hawkish forecasts to sustain the loonie’s rebound.

Fed meeting, GDP data and much more on the dollar’s roster

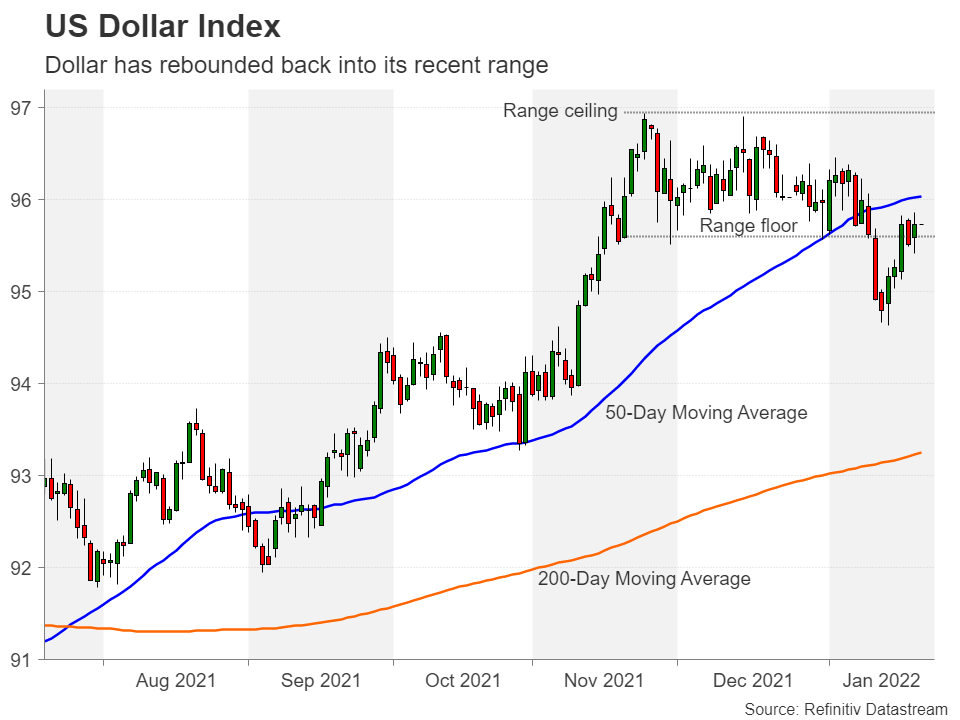

The US dollar has been rangebound since late November and after a short-lived bearish breakout, it’s back to being neutral again against a basket of currencies. However, it’s hard to see the greenback maintaining this posture in the coming week when apart from the all-important FOMC meeting, there’s a raft of data due on the health of the US economy.

The flash PMI figures for January by IHS Markit will start the week on Monday. The S&P CoreLogic Case-Shiller 20-city home price index is out on Tuesday along with the closely watched consumer confidence index. New home and pending home sales for December are released on Wednesday and Thursday, respectively. Durable goods orders are scheduled for Thursday too.

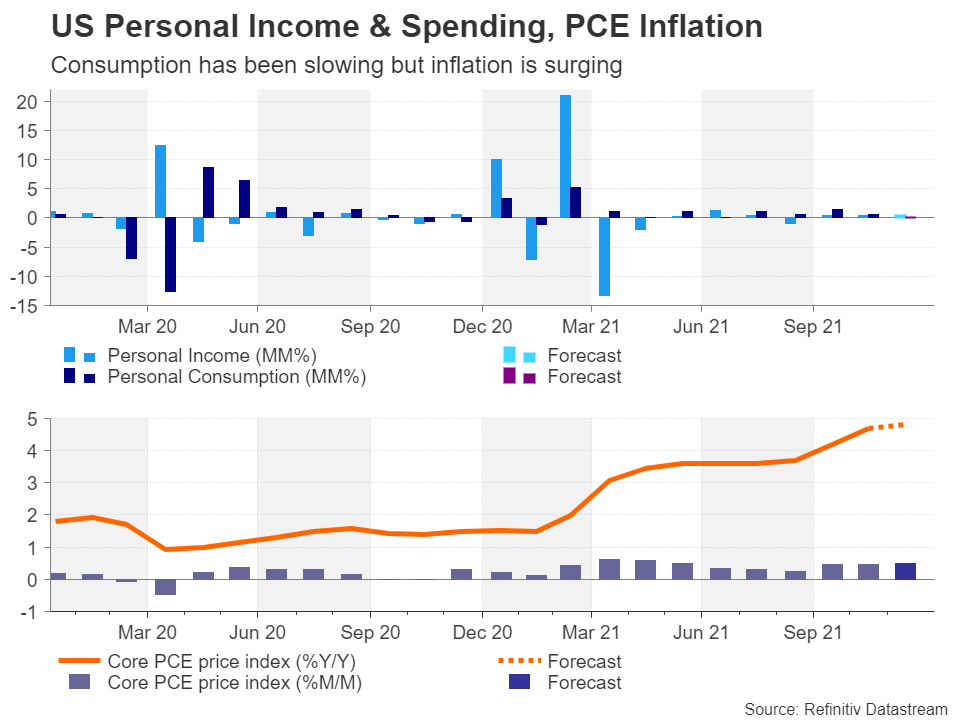

But the real focus will be on the fourth quarter GDP estimates on Thursday and on Friday’s personal income and outlays report containing the core PCE price index and the latest consumption numbers.

US GDP growth probably accelerated to an annualized 5.8% rate in the fourth quarter from 2.3% before, which would support the argument that the American economy is well and truly out of the woods and does not need any additional stimulus.

However, growth likely slowed towards the end of the quarter with personal consumption expected to have risen by just 0.1% month-on-month in December. Personal income is anticipated to have maintained the 0.4% m/m pace, while the core PCE price index is forecast to have inched higher by 0.1 percentage points to 4.8% year-on-year.

If the Fed’s favourite inflation metric meets expectations, showing signs of moderating, that could weigh on Treasury yields, which are currently taking a breather from the recent surge. However, next week’s data will have to play second fiddle to the Fed’s policy meeting.

No change in policy is expected from the Federal Open Market Committee on Wednesday but if policymakers want to get an early start on rate hikes, they will need to signal their intentions for March at the January meeting.

The other item at the top of investors’ agenda is the balance sheet runoff. It’s probably too soon for the Fed to go into too much detail about this but no doubt Chair Jerome Powell will be asked about it in his press conference and any revelations on the timing and speed are bound to spark a big response in the bond market, which in turn could roil FX and equity markets.

Will Eurozone PMIs add to euro’s woes?

The euro enjoyed some rare upside action last week but the bulls were unable to hold out for too long and the $1.14 handle proved unsustainable. Monday’s flash PMI prints will be important as they are often a reliable indicator for GDP growth in the euro area. Both the manufacturing and services PMIs are forecast to have edged lower in January amid a combination of tighter restrictions and heightened public caution due to the Omicron outbreak over the Christmas and New Year period. The overall composite PMI is expected to have fallen from 53.3 to 52.6 in January.

Such a drop would represent only a modest deceleration in growth and is unlikely to ring any alarm bells for the European Central Bank, which meets in the first week of February. The euro might even gain some ground if there’s a small positive surprise and the Fed isn’t quite as hawkish as feared.

Also of interest will be Germany’s Ifo business climate gauge (Tuesday) and the Eurozone’s economic sentiment indicator (Friday).

Is Boris about to quit?

Over in the UK, the PMI numbers will be the highlight of the week too, at least on the data front. A political storm is currently brewing in Westminster, though the markets have so far taken little notice of it. Pressure is growing on Prime Minister Boris Johnson to resign following a series of scandals, the latest one of which is ‘Partygate’. Downing Street staff allegedly held parties during the lockdowns of 2020 and 2021, one of which was attended by Johnson.

Most likely, the prime minister is safe for the time being. But should he resign, the markets would probably be comfortable with any of the current hotly tipped contenders to replace him.

A more pressing matter for the pound is what the Bank of England will do at its next meeting. Recent data out of the UK have been mostly strong, including the last CPI report. It’s possible Monday’s flash PMIs will buck the trend but that shouldn’t deter the BoE from lifting rates for a second time since the pandemic in February.

Nevertheless, some volatility shouldn’t be discounted for cable over the next few days, whether it’s sparked by Partygate or the Fed.

Antipodeans on CPI alert

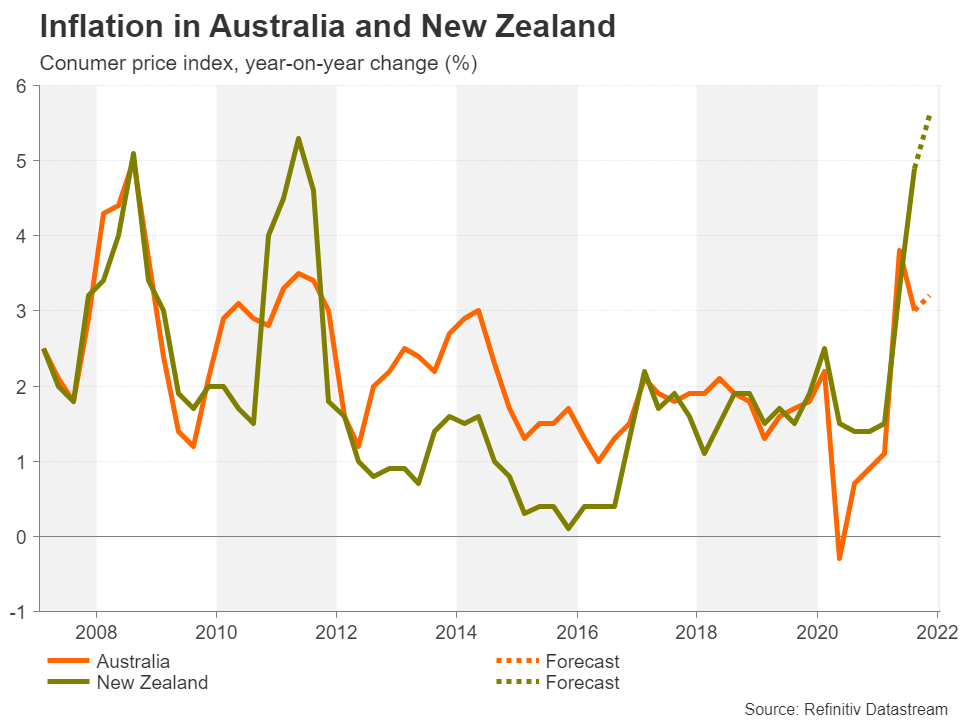

The Australian dollar got a significant boost in the past week from a much stronger-than-expected set of jobs numbers. With the fourth quarter CPI readings due on Tuesday, the aussie could enjoy a further lift if Australia’s inflation rate climbs higher as expected. The Reserve Bank of Australia convenes on February 1 and may decide to end its asset purchase programme early if there’s reason to worry about spiralling inflationary pressures. Ahead of the CPI report, the flash PMIs will be watched on Monday for more evidence that Omicron had only minimal impact on the Australian economy.

In neighbouring New Zealand, inflation will also be front and centre. The country’s quarterly CPI prints are out on Thursday and there could be another spike in headline inflation, which had jumped to 4.9% y/y in Q3.

The Reserve Bank of New Zealand doesn’t meet until February 23. But with a quarter-percentage point rate hike already fully priced in for each of the RBNZ’s meetings this year, the only thing that can be a game-changer for the struggling New Zealand dollar is if the figures are strong enough to open the door for half-point increases.