{kind=link}

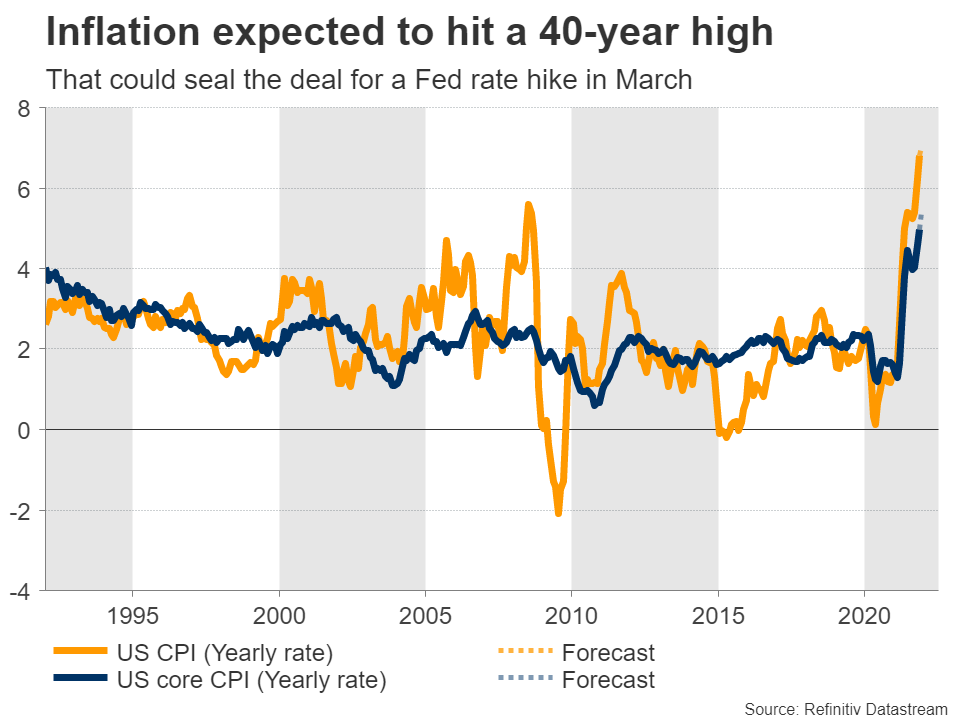

The latest US inflation data will be published on Wednesday at 13:30 GMT, ahead of the retail sales report on Friday. Consumer prices are expected to have risen at the fastest clip in 40 years, which could seal the deal for a Fed rate hike in March. That said, there is scope for disappointment in the spending numbers, so it could be a rollercoaster ride for the dollar.

Fed gets rolling

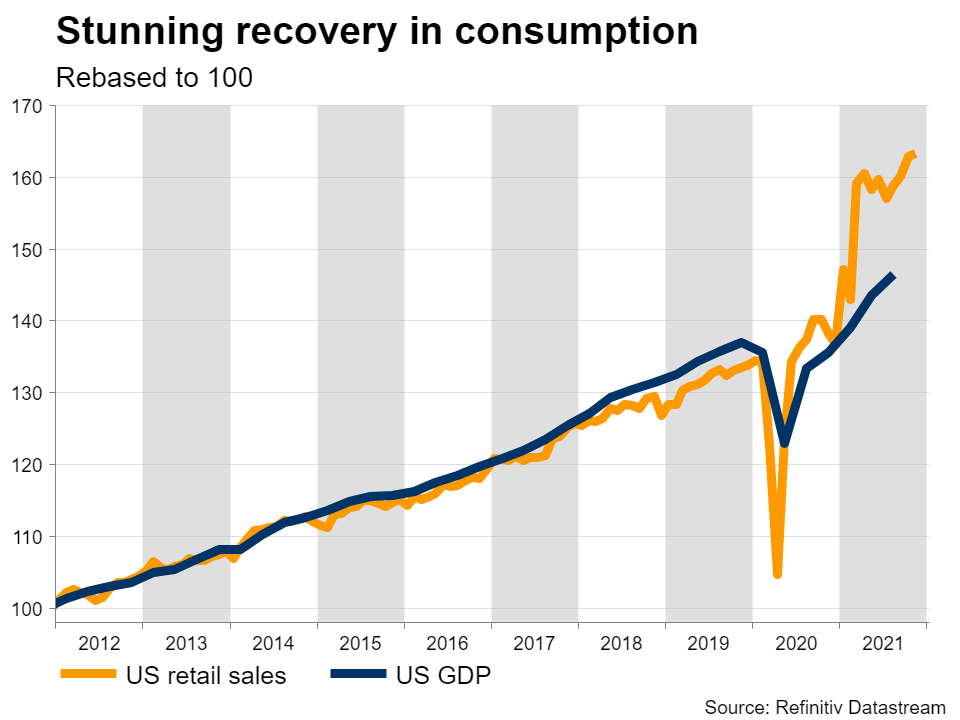

The US economy is firing on all cylinders. Consumption has been incredibly strong, economic growth in the last quarter is seen at 6.8% according to the Atlanta Fed’s GDPNow model, and the labor market is approaching full employment with impressive speed.

Most importantly, wage growth has fired up. When the Fed sees a tight labor market and accelerating wages, the conclusion is that this could lead to a wage-price spiral that feeds inflationary pressures. Since inflation is extremely hot already, Fed officials want to avoid that outcome. The solution is to tighten monetary policy.

As such, traders have brought forward the expected timing of Fed rate increases lately. The implied probability for a rate hike in March currently stands at 90%. In total, markets are pricing in three rate increases this year and equal odds for a fourth one.

Inflation to heat up

On the data front, forecasts suggest the annual CPI inflation rate hit 7% in December, up from 6.8% in November. The core rate that strips out volatile items like energy and food is expected to have risen to 5.4%, from 4.9% previously.

These projections are supported by the Markit PMI surveys, which showed that selling prices by companies “rose steeply”, although at the slowest pace in three months. That’s in line with the forecasts for the monthly CPI print.

Turning to retail sales, the tea leaves point to disappointment. The retail control group – which is used in GDP calculations – is expected to have risen by 0.1% on a monthly basis. However, credit card spending data from Bank of America and JP Morgan suggest a far weaker number, possibly negative, as worries around Omicron dampened consumption.

Dollar rollercoaster ahead

As for the dollar, it could be a volatile week. A strong inflation report may seal the deal for a rate hike in March and boost the reserve currency, before a potential disappointment in retail sales wipes out some of the gains.

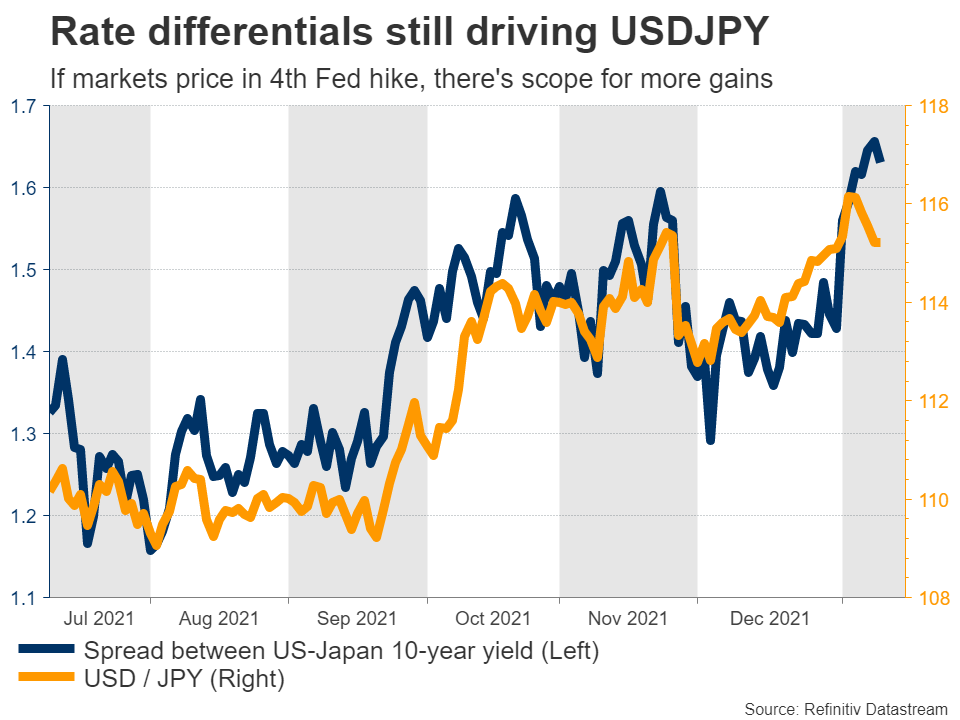

In the bigger picture, the outlook remains bright over the next few months. The economy is booming and there’s still room for markets to price in a fourth rate increase for this year. Beyond rate hikes, the Fed’s plans about shrinking its balance sheet could be an additional force that supports the dollar against low-yielding currencies like the yen.

The main risk to this view would be any signs that inflation has peaked moving forward. If investors sense the heydays of inflation are behind us now that energy prices are stabilizing and government spending is fading, they could dial back bets for Fed tightening. But that’s probably a story for April or later, as that’s when the year-over-year comparisons in inflation become much tougher.

Taking a technical look at dollar/yen, if the bulls manage to pierce above the 5-year high of 116.30, the next barrier to provide resistance may be 117.80, which was the inside swing high of December 2016.

On the downside, initial support to declines may be found at 115.00. A potential violation would turn the focus to 114.25, a region that overlaps with the 50-day moving average and the uptrend line drawn from the September lows.