{kind=link}

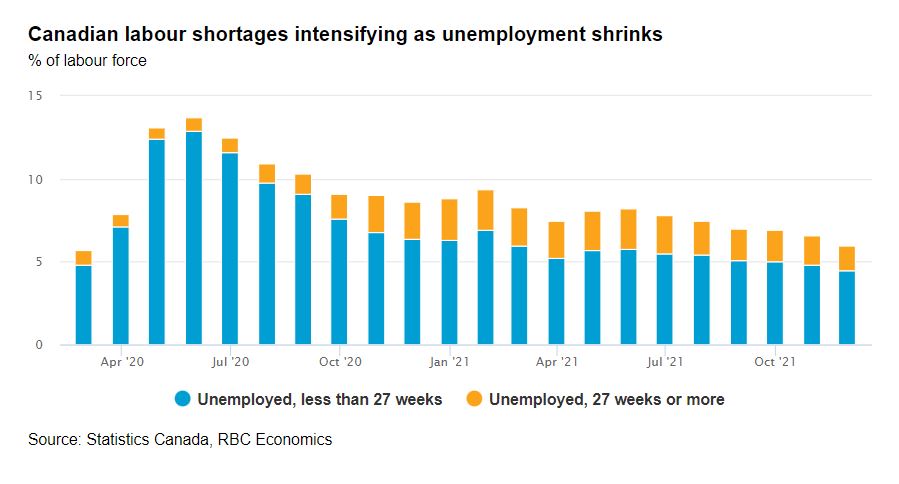

Virus concerns and inflation will loom over the final scheduled Bank of Canada policy decision of 2021. So far, economic data has been tracking close to the central bank’s expectations. The 5.4% (annualized) increase in Q3 GDP was almost bang-on with the 5.5% forecast in its October policy update. And though inflation is still running well above the central bank’s target, it’s broadly in line with the 4.8% Q4 CPI increase expected as of the October MPR. But labour markets have continued to improve with a much stronger than expected 154,000 jobs added in November, and at 6%, the unemployment rate is falling back closer to pre-pandemic levels.

The emergence of the Omicron variant has rattled financial markets and is a reminder that the pandemic is still not over. Inflation has also moved higher, labour markets look increasingly tight, and wage pressures are building. Demand and purchasing-power are not expected to be an issue with the household pandemic savings stockpile ballooning to nearly $300 billion as of Q3. Businesses are largely identifying labour shortages and higher input costs as more significant concerns than any shortfall in orders. The BoC might still be able to point to pockets of weakness in labour markets—long-run unemployment is still elevated, for example. But arguments to keep policy interest rates at emergency low levels are getting thin. The BoC is expected to reiterate that, barring significant further disruptions from the new virus variant, the economy is on track to fully recover by mid-2022, and that interest rate hikes will be warranted at that point. We expect the first rate hike next year to come in April.

Week ahead data watch:

- US headline CPI inflation is primed to rise to 6.6% from a year ago in November. We expect that higher fuel prices and stronger used autos prices will put upward pressures on the monthly reading.

- Canadian household net worth likely rose further in Q3 with rising asset values offsetting increases in mortgage debt and consumer credit. Debt service ratios and the closely-watched household debt-to-income ratio are expected to tick higher but to remain well below pre-pandemic levels.

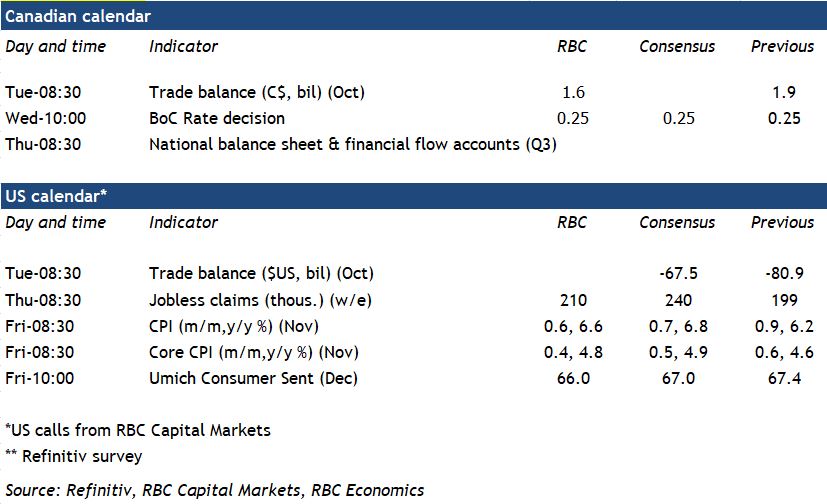

- We expect the Canadian merchandise trade surplus to narrow to $1.6B in October. A resumption of auto production after widespread shutdowns in September due to chip shortages should boost both exports and imports, while agricultural exports are expected to fall due to low crop yields in western Canada.