{kind=link}

It’s a packed week for UK economic indicators, starting with the labour market report on Tuesday, CPI figures on Wednesday and retail sales data on Friday, all due at 07:00 GMT. The pound is still licking its wounds from the Bank of England flip flopping on its rate hike decision, with the surge in the US dollar adding to the pain. But potentially upbeat numbers in this week’s trio of releases might turn out to be the reminder that investors needed that a rate hike is still on the agenda at the BoE.

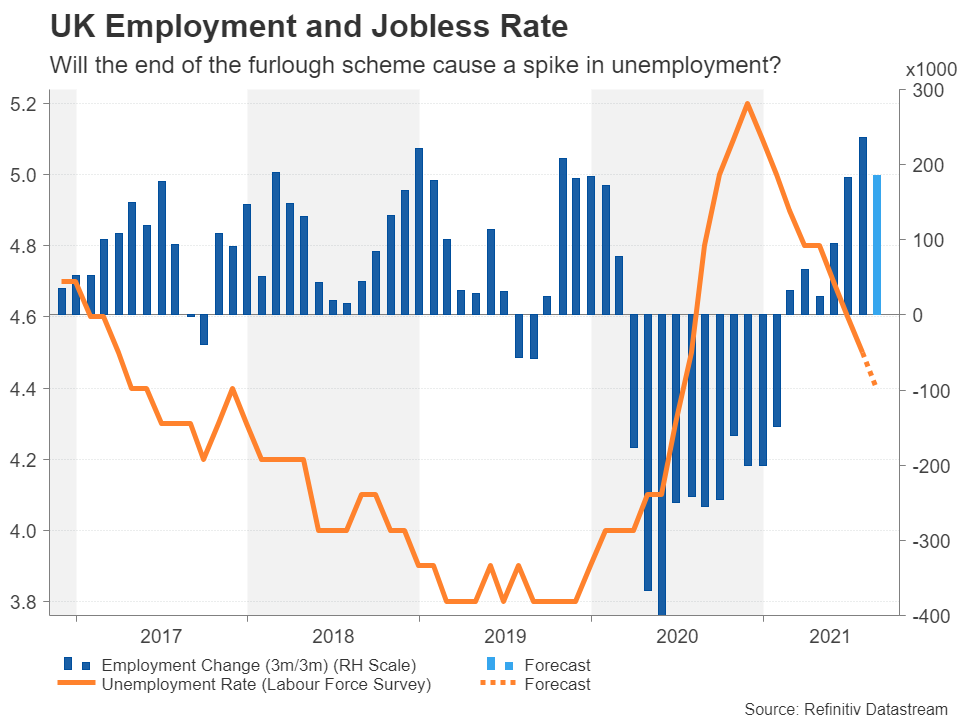

A tight labour market

Despite the UK economy taking a bigger hit from the Covid shutdowns than most other advanced economies, the pandemic has barely left a mark on the labour market. Locked down workers have the government to thank for being able to hold on to their jobs as Chancellor Rishi Sunak’s furlough scheme was one of the most generous in the world. However, that lifeline for millions of Brits ended in September and Tuesday’s data will be the first indication as to whether businesses held on to those workers who were being subsidized by the government.

The three-month employment change is expected to see a rise of 185k in September, slowing somewhat from the 235k gain of the prior month. That should lower the unemployment rate down a tick to 4.4% to a new post-pandemic low. However, what investors will really be looking at is the October data for the change in the number of people claiming unemployment benefits as a spike in this figure would suggest there were big job losses from the furlough scheme coming to an end.

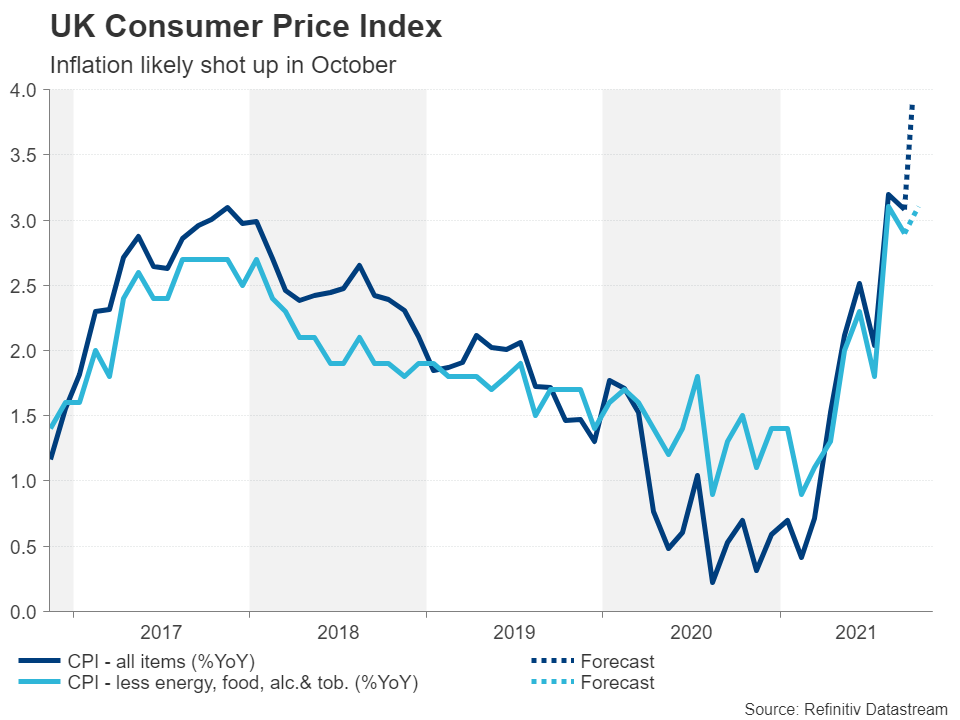

Is inflation about to skyrocket?

Average weekly earnings growth will also be eyed on Tuesday for possible signs that wage pressures are hotting up, though forecasts suggest they moderated in September. The big reveal on inflationary pressures will come from the latest CPI readings on Wednesday.

Britain’s consumer price index is expected to have jumped from 3.1% to 3.9% year-on-year in October. The core rate is projected to have climbed from 2.9% to 3.1% y/y. The Bank of England’s inflation target allows for the CPI rate to fluctuate within a one percentage point band above or below 2% so a number in the 4% vicinity would alarm the hawks at the BoE.

A strong recovery that could have been stronger

One of the concerns that investors have had ever since inflation started running wild and the BoE started to get edgy about it is whether the UK economy can withstand higher interest rates. Although, GDP has recovered strongly this year from the depths of the pandemic slump, the reopening effect wasn’t as powerful as many had hoped. More recently, fears that both business and household spending will be curtailed by the global supply-chain bottlenecks and the surge in energy prices have been weighing on the pound, offsetting some of the boost from rising rate hike speculation.

But consumption in the retail sector likely bounced back in October after several months of declines. Retail sales are forecast to have grown by 0.5% month-on-month, although the 12-month figure is expected to have stayed negative at -2.0%.

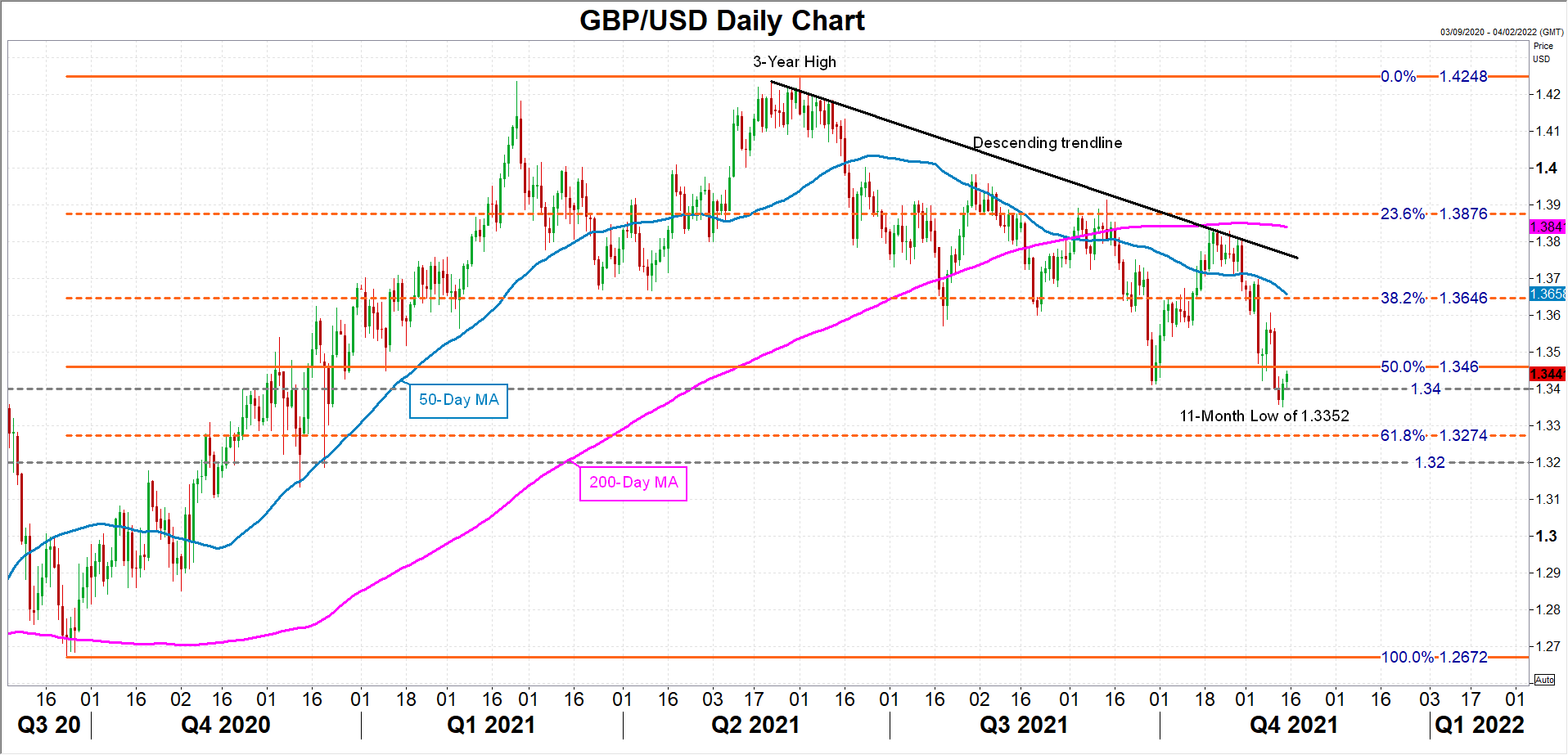

Battered pound hoping for data lift

Nevertheless, a positive trend in all three datasets could be enough to aid sterling’s rebound from 11-month lows against the US dollar as rate hike bets for December and February would be ramped up. The pair is currently trading below the immediate resistance of the 50% Fibonacci retracement of the September 2020-June 2021 uptrend at $1.3460. A break above this barrier could open the way for the 38.2% Fibonacci of $1.3646 just below the 50-day moving average (MA). However, reaching the 50-day MA would still leave cable some way off the descending trend line, which needs to be overcome if the bearish picture is to turn positive.

In the event that the data barrage disappoints and investors price in a reduced likelihood of an early move on rates by the Bank of England, sterling could plunge to fresh lows. If the recent trough of $1.3352 is breached, the 61.8% Fibonacci of $1.3274 would be the next major support, followed by the $1.32 level.