{kind=link}

- Dollar remains king as Fed shockwaves reverberate

- Stocks caught in limbo, oil prices wary of supply risks

- Second-tier data coming up today, but could be crucial

Dollar reigns supreme

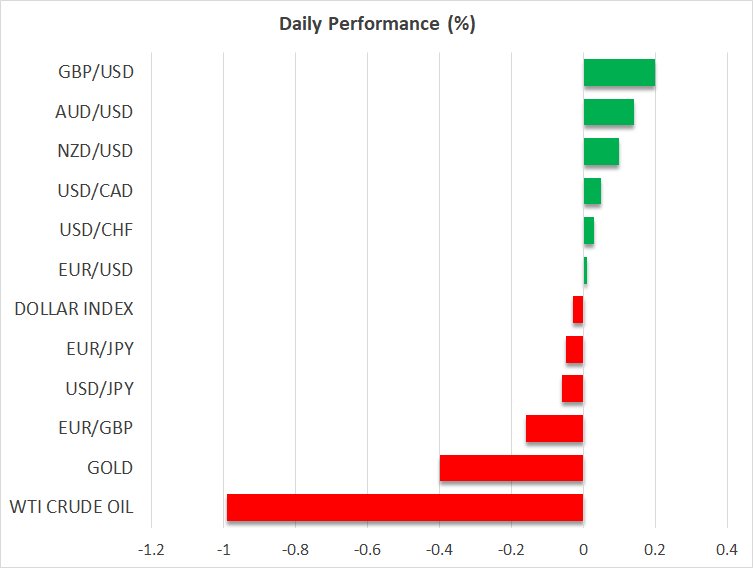

The trading week is coming to a close with the dollar ruling the skies over the FX battleground, after a shocking acceleration in US inflation reignited expectations for faster Fed rate increases and served as jet fuel for the reserve currency. Markets are currently split on whether the FOMC will hike rates twice or three times next year.

As such, next week’s retail sales could be crucial in tipping the scales. Credit card data from J.P. Morgan Chase points to a solid October for spending but an incredible November as some consumers may have started holiday shopping early, fearful of delayed deliveries. Therefore, there might be more good news on the way for the dollar.

In contrast, the euro is still grappling with several risks. The spiral in energy prices could squeeze European consumers, soaring covid cases in Germany have revived fears of stricter measures that cool growth, and China’s slowdown is bad news for demand in Europe’s largest export market.

Taken together, these suggest the ECB could disappoint market expectations for a minor rate increase next year while there’s still scope for a third Fed rate hike to be priced in, keeping the risks surrounding euro/dollar tilted to the downside.

Stocks in a dilemma

Wall Street didn’t do much yesterday. The Dow Jones was dragged lower by a sharp decline in Disney shares after the entertainment conglomerate reported disappointing growth in streaming, but some relief in mega-cap tech stocks pulled the Nasdaq higher. The S&P 500 was somewhere in the middle, closing almost unchanged.

Equity markets seem caught between opposing forces. Record low real yields, a frenzy in corporate buybacks, and fresh fiscal stimulus are colliding with fears over fading central bank liquidity, a slowdown in earnings next year, and weaker growth in China.

It’s a tough environment to navigate and sky-high valuations don’t make it any easier. The bottom line? The risk of a correction from such elevated levels is uncomfortably high, but any drawdown would likely be seen as a buying opportunity for many traders as there’s still no alternative to equities while real yields are so depressed.

Oil under pressure

In the energy market, oil prices remain on the retreat. There’s growing speculation that the White House could release the ‘kraken’ soon, or in other words the Strategic Petroleum Reserves, to cool oil prices and by extension inflation. Making a deal with Iran is another alternative.

The Canadian dollar is feeling the heat of softer oil prices and the stronger US dollar, but admittedly, the nation’s economy is just too strong to worry about a sustained downtrend. The Bank of Canada will likely be the leader among the major central banks in this normalization cycle, an assessment that markets agree with considering the five rate increases already priced in for next year.

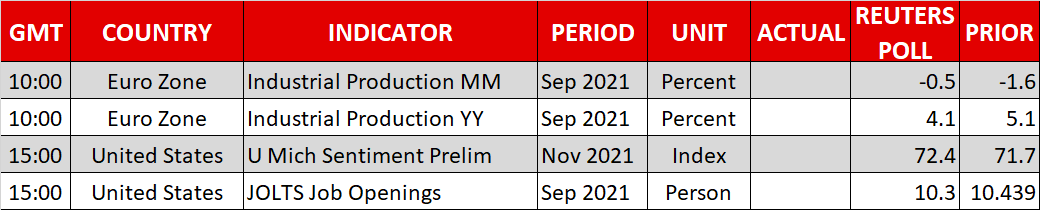

As for today, the highlights will be the University of Michigan consumer sentiment survey and the JOLTS labor market report. These are typically second-tier US economic data, but they could attract special attention this time with the spotlight falling on inflation expectations and the job quit rate. New York Fed President John Williams will also deliver remarks at 17:10 GMT.