{kind=link}

- All eyes on US inflation today, dollar’s fortunes hang in the balance

- Stocks pull back after massive rally, bond market in gloomy mood

- Oil prices jump, iron ore slumps, gold rallies but not impressively

Another inflation shock?

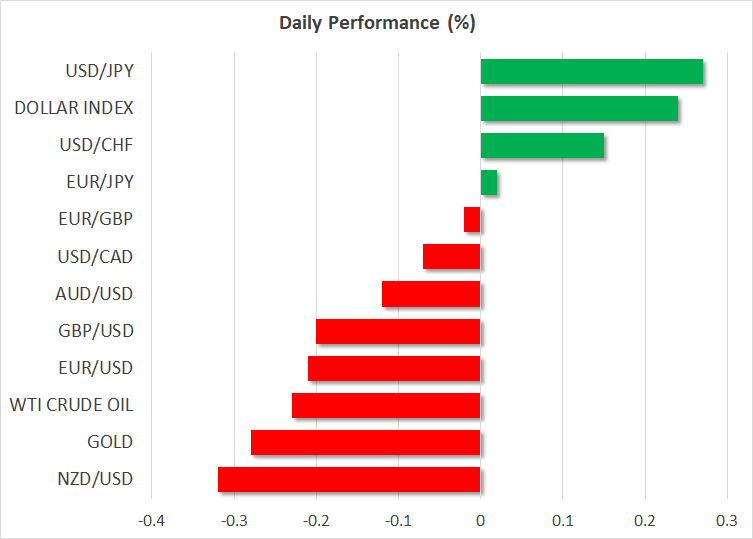

The spotlight today will fall on the latest US inflation report, which could unleash turmoil in the markets if there are any meaningful surprises. The annual CPI rate is expected to have soared to 5.8% in October, a pace not seen in three decades.

If anything, the risk might be for a positive surprise considering the signals from various business surveys. Companies raised their selling prices “at the fastest pace on record” during the month according to the Markit PMIs, while both the ISM surveys showed a sharp increase in prices paid by firms for supplies.

As for the dollar, it will likely move in the same direction as any inflation surprise. Whether inflationary pressures are broadening out into different sectors such as rents will also be crucial as investors try to decipher how many times the Fed will push the rate hike button next year.

Markets are pricing in two Fed rate increases for next year, which allows scope for a hawkish repricing towards three if inflation keeps firing up. In contrast, market pricing for rate hikes next year in the UK, Australia, and Eurozone seems too aggressive and allows scope for disappointment. Hence, those currencies may be vulnerable against the dollar, which also offers protection against stock market drawdowns.

Stocks retreat, bonds worry

Wall Street snapped its incredible winning streak yesterday, with a 12% loss in Tesla dragging the overall market down, but only slightly. There’s also a sense of technical exhaustion as momentum indicators were stretched in overbought territory. This market lives off momentum, with options flows running the show lately.

But the real puzzle is the bond market, which is transmitting some alarming signals as inflation-protected Treasury yields have fallen back near record lows. There are multiple ways to read this. Normally it would suggest investors expect slower growth, but in this environment, traders could be piling into these bonds to hedge their inflation exposure.

Either way, the signal is worrisome for the longer-term fortunes of the economy. It suggests low growth potential but high inflation prospects, playing right into the ‘stagflation’ narrative. On the bright side, record low real yields are usually a blessing for assets like growth stocks and gold.

A glance at commodities

Gold should be absolutely thriving with real yields getting blasted, so even though the yellow metal has enjoyed some solid gains lately, the magnitude of the rally has been quite disappointing. The $1835 region has been an impenetrable fortress in recent months, therefore, a powerful breach is required for buying interest to intensify.

Meanwhile, oil prices came back swinging yesterday after the Energy Information Administration reaffirmed its forecasts that the market will swing into a supply surplus next year. This would typically be a negative sign for oil prices, but the market saw it as diminishing the chances that the White House releases the Strategic Petroleum Reserves to counter high prices.

Finally, iron ore prices are in freefall thanks to slowing demand from China and growing inventories. While the Australian dollar has been rather resilient so far, the risks keep accumulating with a tsunami of credit downgrades in China that has sent junk bond yields through the roof and the RBA unlikely to live up to the market’s rate hike expectations.