{kind=link}

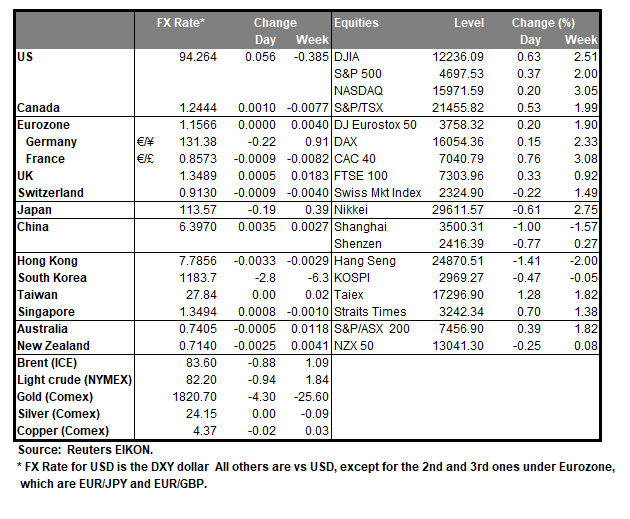

The USD despite getting some support from the solid employment data for October released on Friday, ultimately ended the day lower than what it began against a number of its counterparts as US yields dived to lower grounds. The next big bet for the markets after the release of the US employment data for October seems to be the release of the US CPI rates for October on Wednesday, while six Fed officials are scheduled to speak today, and we place some attention more on Fed Vice Chair Clarida. On the contrary the US stockmarkets gained on Friday, with Dow Jones, S&P 500 and Nasdaq reaching new record highs expressing the positive, risk on sentiment of the markets. Over the weekend, we note that Elan Musk’s tweet on whether he should sell 10% of his stake in Tesla was answered by a majority positively and that could have an adverse effect on the share’s price. Remaining on the equities front, Pfizer’s share price soared on Friday as it’s Covid pill study produced strong results, while competitors Merck’s and Moderna’s share prices dropped considerably. As for precious metals Gold’s price gained on the back of a weaker USD as well as dropping US yields. On the commodities front, oil prices were on the rise as expectations for strong demand remained elevated, especially after Saudi Aramco, raised its Asia prices for its light crude, while supply is expected to remain tight. The Looney on the other managed to remain steady against the USD as despite a lower-than-expected employment change figure for October the unemployment rate still ticked down in the Canadian October employment data, while higher oil prices tended to provide some support as well. On the other hand, the Aussie also remained stable despite China’s Trade surplus boom as imports seem to slow down.

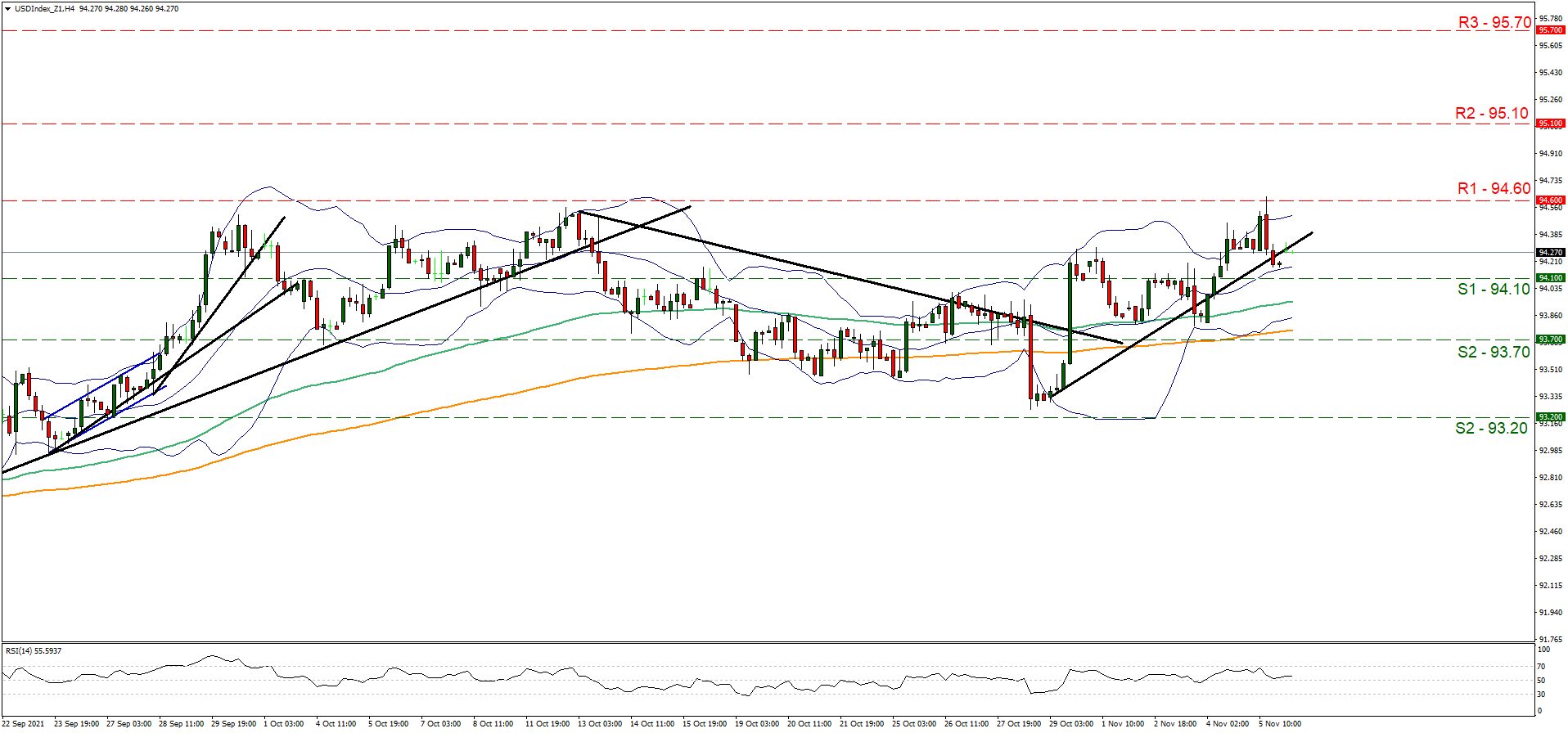

The USD Index dropped on Friday and maintained low volatility during today’s Asian session. We tend to maintain a bias for a sideways motion for the index currently between the 94.10 (S1) and the 94.60 (R1) level. Should a buying interest be expressed for the index we may see it breaking the 94.60 (R1) level and aim for the 95.10 (R2) resistance line. Should the market decide to sell the Dollar, we may see the index breaking the 94.10 (S1) support line and aim for the 93.70 (S2) level.

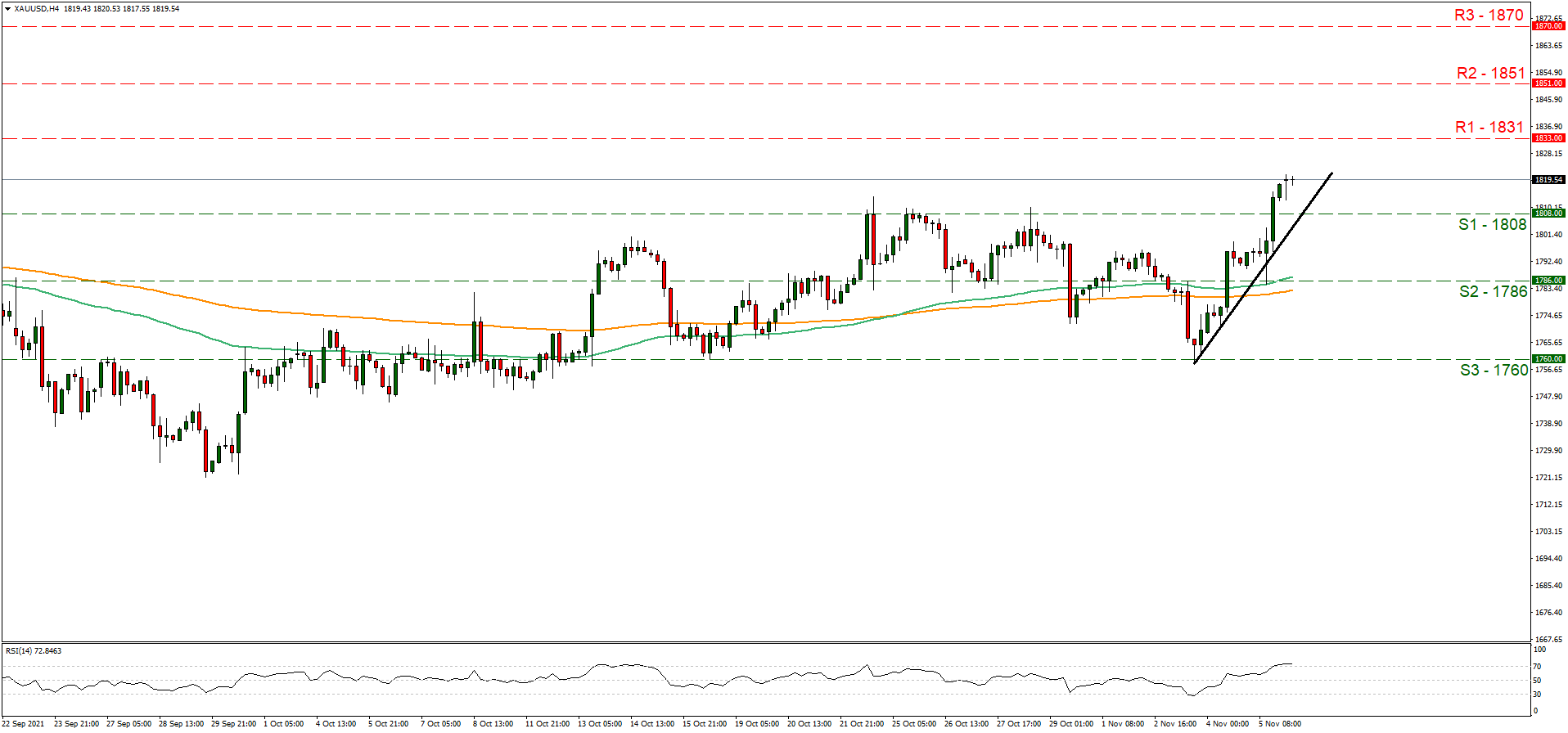

Gold’s price continued to rise on Friday breaking the 1808 (S1) resistance line, now turned to support. We tend to maintain a bullish outlook for the precious metal’s prices as long as it remains above the upward trendline incepted since the 3rd of November. Should the bulls actually maintain control over gold, we may see its price breaking the 1831 (R1) resistance line and take aim of the 1851 (R2) level. Should the bears take over we may see gold’s prices breaking the 1808 (S1) support line and aim for the 1786 (S2) level.

Today’s events and expectations

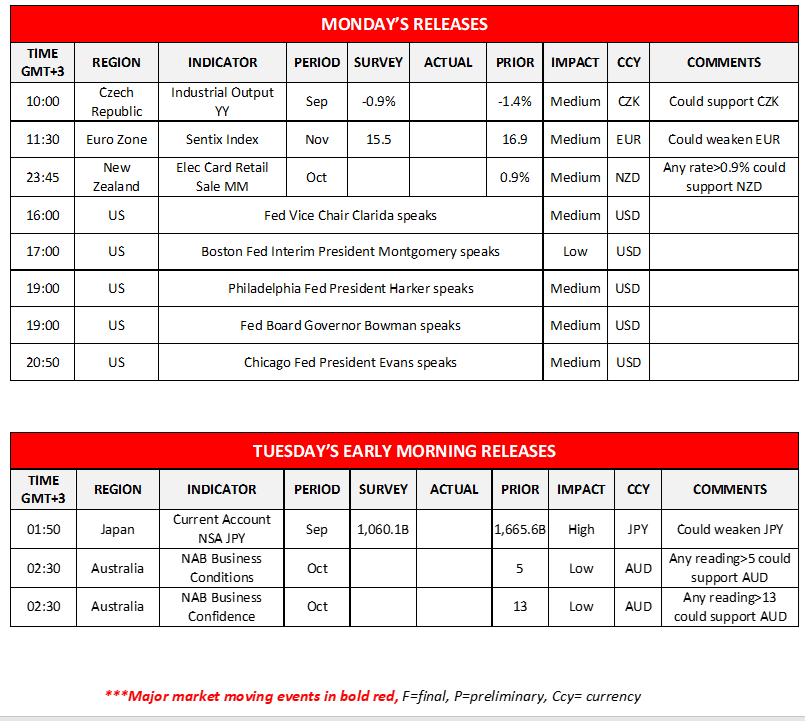

Today we get from the Eurozone the Sentix index for November and just before the Asian session New Zealand’s electronic card sales for October. During Tuesday’s Asian session, we get Japan’s current account balance for September and from Australia NAB’s October Business Conditions and Business Confidence.

As for the rest of the week

On Tuesday we get from Japan the current account balance for September and Germany’s ZEW indicators for November. On Wednesday we note the release of Inflation measures from China, Germany, Norway, the Czech Republic, and most importantly from the US, all being for the month of October as well as the US weekly initial jobless claims figure. On Thursday we get Japan’s Corporate Goods Prices for October, Australia’s employment data or October as well as UK’s GDP rates for September and Q3 and Manufacturing output for September. On Friday, we get Norway’s GDP rate for Q3, Eurozone’s industrial production for September and the preliminary US University of Michigan consumer sentiment reading for November.

USD Index H4 Chart

Support: 94.10 (S1), 93.70 (S2), 93.20 (S3)

Resistance: 94.60 (R1), 95.10 (R2), 95.70 (R3)

XAU/USD H4 Chart

Support: 1808 (S1), 1786 (S2), 1760 (S3)

Resistance: 1831 (R1), 1851 (R2), 1870 (R3)