{kind=link}

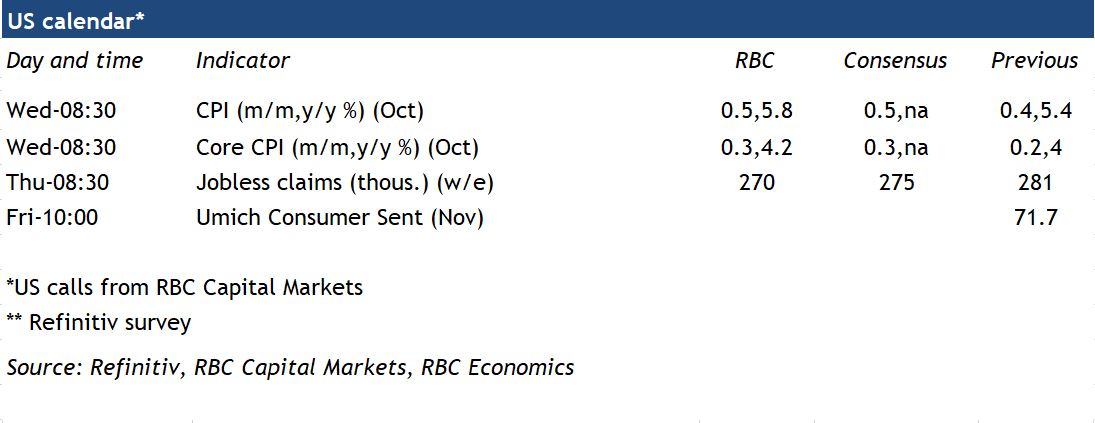

All eyes will be on US inflation figures next week during a quiet period for Canadian data releases. US CPI growth is expected to remain elevated—up almost 6% relative to October 2020—as growth in consumer prices continue to be affected by very low year-ago prices. Nearly half of the increase in the CPI relative to pre-COVID levels is being driven by a small number of components such as used cars and energy, both of which likely moved higher again in October. The more pressing concern in both the U.S and Canada is that price pressures are broadening as demand recovers and production is limited by global supply chain disruptions and labour shortages.

Shelter costs have been a larger CPI driver in Canada, with exceptionally tight resale markets pushing up realtor/broker fees and prices. They continued to rise in October with early market reports pointing to a reacceleration in home price growth. The Bank of Canada acknowledged more persistent price pressures and expects inflation to average 4.8% in Q4 before easing to average 3.4% next year. At its November meeting, the Fed said the rise in inflation is “expected to be transitory” and that vaccines and easing supply constraints should support continued job gains and a reduction in inflation. The Bank of Canada (with its single mandate focus on inflation) reiterated at its recent meeting that policymakers are watching inflation expectations and labour cost growth closely for signs that recent inflation pressures could be more persistent than they currently expect.

Week ahead data watch:

- We expect US Inflation remained elevated, growing by 0.5% in October from September, and up 5.8% year-over-year. Distortions to supply side factors such as port congestion, input and labour shortages will continue to put on floor on price growth. Looking beyond the pandemic base effects, the more important focus will be on the evolution of monthly price gains.