{kind=link}

- New records for Wall Street as cooling energy prices pull yields down

- RBA plays down early rate increases, torpedoes Australian dollar

- US dollar, British pound, and oil prices await crucial events

New highs

The US stock market continues to trade like a runaway freight train. All three major indices on Wall Street closed at new record highs to kick off the new month, basking in the glory of a solid earnings season and some signs that the worst of the energy crisis may be over.

Coal prices have fallen back to earth after China fired up its internal production to counter the shortages, allowing natural gas prices to come off the boil in sympathy. In turn, falling energy prices have halted the relentless rally in inflation expectations, pushing yields on short-dated government bonds lower amid hopes that central banks won’t have to wage total war against inflation.

Another encouraging sign has been the cooling in transportation costs lately, with the Baltic exchange dry index falling substantially while container shipping costs from China have stabilized, signaling that paralyzed supply chains may be healing at last.

While the energy crisis may have peaked and some early signs suggest the same is true for transport costs, the market still has to get through the Fed meeting tomorrow, where the tapering timeline could be accelerated.

RBA sinks aussie

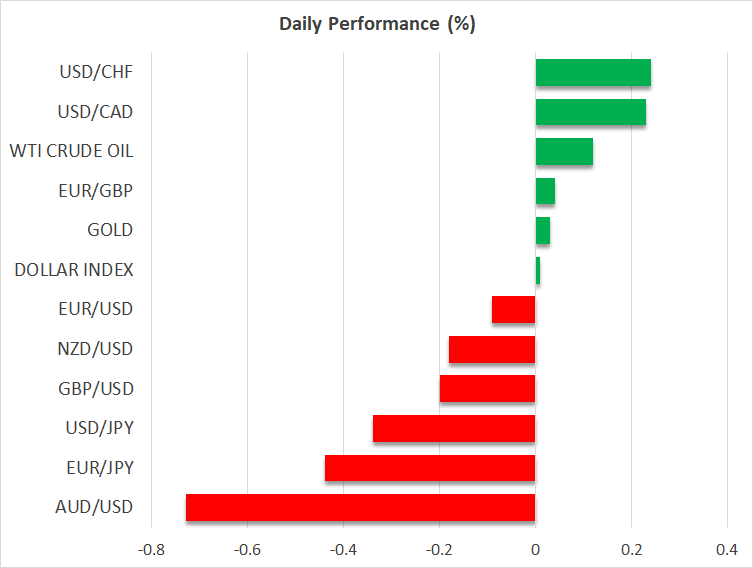

Over in Australia, the Reserve Bank managed to do what the ECB couldn’t last week – convince the markets that pricing in multiple rate increases for next year is unrealistic. Even though the RBA abandoned its yield curve control strategy and opened the door for raising rates before 2024, the aussie still tanked on the news.

Governor Lowe made it clear that rates probably won’t rise until 2023 and that investors overreacted to the latest spike in inflation. With the market pricing in four rate increases for 2022 ahead of the meeting, that sparked a decent repricing that weighed on the Australian dollar.

Nonetheless, the risks surrounding the currency remain tilted to the downside. Even after Lowe’s explicit signals, money markets are still pricing in three rate increases for 2022, which is a bridge too far for an economy that is just emerging from a lockdown and could suffer serious collateral damage from a slowdown in China.

Yen shines, crucial events in focus

In the broader FX sphere, the yen is enjoying its moment in the spotlight. The yen is closely linked to foreign bond yields thanks to the Bank of Japan keeping a ceiling on Japanese yields. As such, it shines whenever global yields retreat as its interest rate disadvantage shrinks. The yen is essentially at the mercy of energy prices and supply chain disruptions at the moment, as those factors are driving inflation expectations and by extension bond yields.

The US dollar and British pound have been relatively stable ahead of their respective central bank meetings on Wednesday and Thursday. Most of the intrigue is on whether the Bank of England will raise rates and how split the Committee might be on that decision, but the Fed could also spark fireworks as the tapering process may need to be expedited if rates are to be raised next summer.

Last but not least, oil prices will be under the microscope when OPEC meets on Thursday. There’s a lot of political pressure on the cartel to open the supply taps wider and counter the price rally, but even if that happens, any extra production boost would likely be only symbolic. Their own forecasts point to a supply surplus next year, so pumping much more now would risk flooding the market.