{kind=link}

U.S. Highlights

- GDP growth slowed to 2.0% quarter-over-quarter (annualized) in the third quarter of this year, down from 6.7% in the second quarter.

- The shift in the composition of consumer spending away from goods and into services signals some long-awaited relief for congested supply chains.

- While third quarter economic growth disappointed, early October data point to a healthy start to the fourth quarter of the year.

Canadian Highlights

- The marquee event this week was the Bank of Canada rate announcement. The Bank struck a hawkish tone, ending its quantitative easing program and pulling forward the timing of when it expects the output gap to close.

- An earlier closing of the output gap combined with higher inflation opens the door to an earlier liftoff in the policy rate. We expect the Bank to raise rates three times next year, starting in the second quarter.

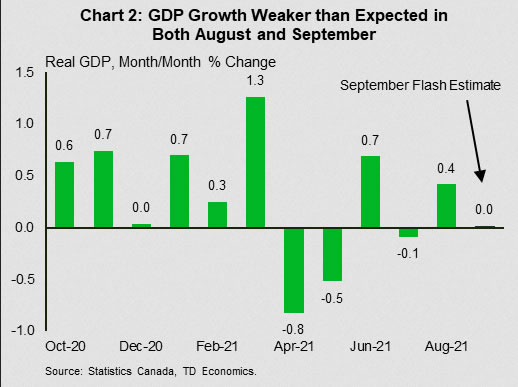

- GDP growth in August was healthy at 0.4% month-over-month, but the flash estimate for September showed no growth in the month. This puts GDP on track to rise by 2.0% annualized in Q3.

U.S. – Things Are Slowly Getting Back to Normal

As expected, GDP growth dipped in the third quarter of the year. Granted, the slip to 2.0% quarter-over-quarter (q/q, annualized) from the 6.7% pace in the second quarter was steeper than the market consensus expected. Though a small surprise to the downside, the slowdown aligns with the notion that the headwinds from strained supply chains and a surge in Delta variant cases were enough to meaningfully hold back growth.

An interesting piece of information was the pull-back in goods imports. For the first time since the second quarter of 2020 goods imports growth registered a negative print, albeit at a small one at -0.1% q/q rate. This falls in line with ports data for the quarter (Chart 2). Using monthly data from the four busiest ports in the United States, inbound container volumes are 17.4% lower in August than they were in March (on a seasonally adjusted basis). This is part of a broader trend, as loaded inbound volumes for the three months through August were 10% lower than the prior three-month period.

Relief on supply chains was expected as consumer spending started shifting back to services. For the quarter, the ratio of services to goods spending ticked up 3.6%, the biggest move since the pandemic started. Even stripping out the troubled automotive sector, services spending growth still won out. Circumstances are still a long way from normal but, combined with the easing of port volumes, the rebalancing in expenditures is a sign that some of the supply chain pressures may be set to ease. This was perhaps most evident in the prices of imported goods whose increases slowed to 5.8% q/q (annualized) from the over 14% pace registered in each of the prior two quarters. Import prices are still growing well beyond what would be considered a normal range, but at least moving in the right direction.

In another sign of spending normalization, September’s income and spending data showed that while disposable income contracted for the second month in a row, consumer spending continued to advance as households devoted less to saving. The personal savings rate is now back in line with where it was in December 2019 (7.5%). It will likely go lower still as households begin spending the savings accumulated over the course of the pandemic.

Other data released this week were mixed. The September Chicago Fed National Activity Index dipped its toe below the cutoff line for trend growth, dragged down by the production and income component. The pending home sales index also pulled back 2.3% from August. On the plus side, September home sales popped 14% (annualized) and the October reading of the Conference Board’s Consumer Confidence Index rose for the first time since June.

An improvement in the consumer outlook for October squares with the IHS’s Flash PMI release from last week that ticked up to a three-month high. Combined with initial jobless claims that have declined for four consecutive weeks, this paints a picture of the recovery picking up speed into the fourth quarter. Growth in the third quarter may have disappointed, but the economy is putting its best foot forward heading into the end of the year.

Canada – The Bank of Canada Signals Earlier Rate Hike

The marquee event this week was the much-anticipated Bank of Canada rate announcement. With inflation running hot and indications that supply chain disruptions will prove longer lasting, markets have shifted expectations for policy rate hikes forward in recent months, placing an even greater focus on this week’s communication.

In the event, the Bank struck a hawkish tone. It ended its quantitative easing program, moving into a reinvestment phase, and pulled forward the timing of when it expects the output gap to close. From a previous expectation of the second half of 2022, it now expects economic slack to be absorbed “sometime in the middle quarters of 2022.” Relative to the Bank’s July’s projection, supply disruptions were deemed to weigh more heavily on the economy’s productive capacity, resulting in an earlier closure of the output gap possible despite lower expectations for economic growth in 2021 and 2022.

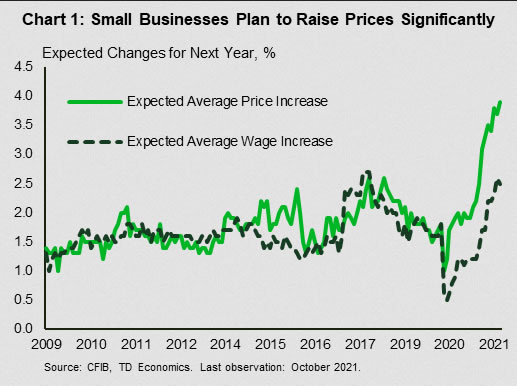

Those changes were accompanied with the significant upgrade to the inflation outlook, with prices now expected to grow by 3.4% in 2021 and 2022 (up from 3.0% and 3.4% pace in July). Inflation has surprised on the upside in recent months, and surveys of inflation expectations suggest that consumers and businesses alike are expecting higher inflation in the near-term. This week’s CFIB Business Barometer survey echoed this. Small businesses planned to increase their prices by 3.9% in the next twelve months, marking an all-time high for the survey (Chart 1). Encouragingly, longer-term inflation expectations so far remain anchored and wage growth is still modest. Nonetheless, the Bank is keeping its eyes on “inflation expectations and labour costs to ensure that the temporary forces pushing up prices do not become embedded in ongoing inflation.”

An earlier closing of the output gap combined with a higher inflation profile opens the door to an earlier liftoff in the policy rate. We expect the Bank of Canada to raise rates three times next year, starting in the second quarter, taking the overnight rate to 1% by the end of 2022. Removing monetary stimulus as the economy continues to recover makes sense. Still, the last leg of the recovery could be challenging. As the Bank acknowledges, there is significant uncertainly when excess slack will be fully absorbed.

Indeed, this week’s monthly GDP report implies a wider starting point for the output gap than the Bank had assumed. Growth in August was healthy at 0.4% month-over-month, but the flash estimate for September showed no growth in the month (Chart 2). Taken together, this puts GDP on track to rise by just 2.0% annualized in Q3, well below the 5.5% forecasted gain in this week’s Monetary Policy Report. Activity could well be made up in the fourth quarter and early next year as economic reopening continues. As long the recovery continues, interest rates will continue to head higher.