{kind=link}

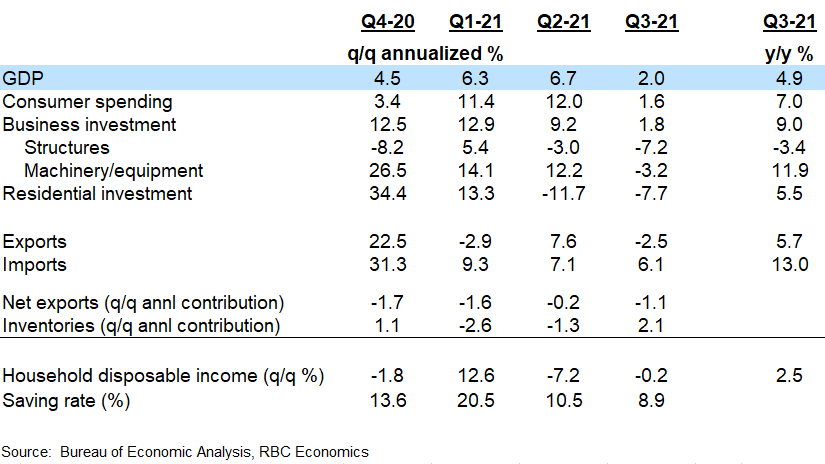

- GDP growth decelerated to 2.0% in Q3 from 6.7% in Q2

- Lack of availability of vehicles contributed to slower household and business spending

- Household purchasing power remains elevated, but much of the ‘easy’ growth to be had from the reopening of the economy is in the rear-view mirror

A large part of the slowing in US GDP growth in the third quarter can be attributed to supply chain disruptions limiting availability of products for purchase – particularly for motor vehicles. Consumer spending growth slowed to just 1.6% (annualized) after surging at double-digit rates in the prior 2 quarters when many parts of the country were reopening from earlier lockdowns. Most of the 9% pullback in spending on goods can be traced back to a sharp softening in consumer purchases of autos. A drop in business purchases of transportation equipment also contributed to a 3.2% pullback in business equipment investment, despite a big 11% increase in industrial equipment purchases.

Both of those declines have more to do with limits on the supply of vehicles available than underlying purchasing power. Household wages and salaries jumped almost 10% in the quarter. Overall disposable incomes were little changed as sizeable government supports continue to roll-off, but were still running 10% above pre-pandemic levels. And the household saving rate remained elevated at 8.9%. Spending on the high-contact services that have been among the hardest hit by lockdowns continued to recover. Overall spending on services was up 7.9% though remained 1.6% below pre-pandemic levels. Residential investment continued to come off the boil, with a 7.7% drop in Q3 that still left the level of activity running 13% above pre-pandemic levels.

The economy is expected to grow more quickly in the fourth quarter. Growth on the goods-producing side of the economy will continue to be limited by global supply chain disruptions and long-run capacity limits, including widely reported shortages of labour in some industries. But there is still room for further recovery in the services side of the economy. Still, it looks increasingly likely that much of the ‘easy’ growth to be had from the re-opening of the economy is in the rear-view mirror, and further gains will be harder to come by. We look for GDP to increase at a stronger 4.5% annualized pace in Q4.