{kind=link}

- Soft US jobs indicators cool expectations for tomorrow’s NFP

- Dollar extends retreat, stocks hang on to record highs

- Oil prices ease as OPEC sticks to the plan, gold trades quietly

Investors on alert for NFP disappointment

Investors on alert for NFP disappointment

With markets buzzing about when the Fed will finally get the taper process rolling, the spotlight is squarely on tomorrow’s US employment report to determine whether the next FOMC meeting is ‘live’ or not. The tea leaves now point to a disappointment, as a series of labor market indicators have been underwhelming lately.

The ADP report fell short of expectations with only 374k jobs added in August, missing the forecast of 613k. This indicator is seen as unreliable because of its poor predictive power over nonfarm payrolls lately, but a similar weakness was also reflected in the ISM manufacturing and Markit composite PMI surveys, adding credence to the concerns.

As such, the dollar took some fire to hit a one-month low against the euro yesterday, as traders positioned themselves for a potential NFP miss that keeps the Fed from touching the taper button this month. That said, even an abysmal jobs report wouldn’t derail the tapering process – it would only delay it.

America is clearly on a path to a strong labor market. There are now more open jobs than people unemployed, which implies that millions of workers are waiting for the right opportunities. With federal unemployment benefits rolling off, the next few months could bring a hiring bonanza. Indeed, there is a universe where the US returns to full employment by year-end, considering that around 2.5 million people who retired early after the pandemic aren’t coming back.

Stocks waiting for the NFP storm

Over on Wall Street, things were awfully quiet. Stock markets kicked off the new month with a neutral tone, as concerns over economic momentum losing steam were overshadowed by hopes the Fed will keep the financial system overflowing in liquidity for a while longer.

With the earnings season fading into the rear view mirror, the most crucial element for equities will be the evolution of monetary and fiscal programs. In this sense, the picture seems promising. The Fed will avoid shocking markets at all costs during its normalization campaign and Democrats in Congress are trying to unleash trillions more in spending to juice up growth in the coming years.

The biggest issues facing this market are the exorbitant valuations in some sectors and the fact that options flow is now the name of the game, with some unreal gamma squeezes serving as jet fuel for the overall rally. The problem is that gamma squeezes can work in reverse too, on the way down, especially if valuations are so stretched.

Antipodeans, OPEC, and gold

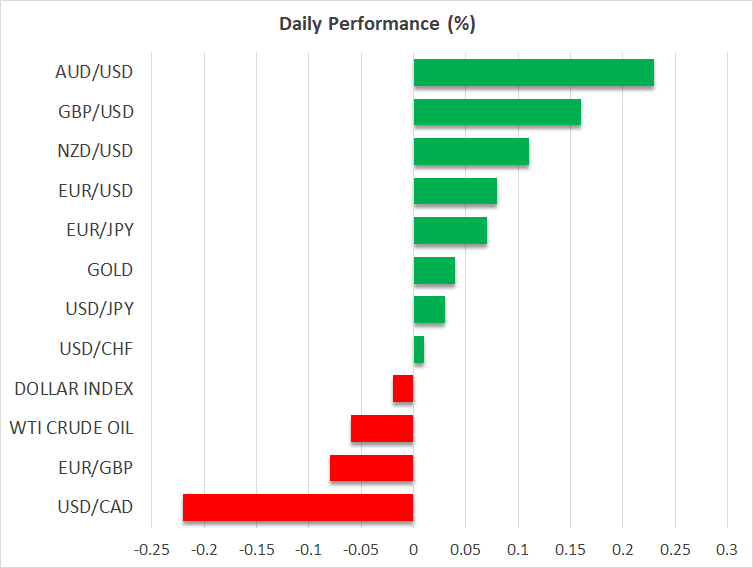

The antipodean currencies came back swinging this week, capitalizing on the softness in the US dollar. Markets have once again priced in a rate increase by the RBNZ next month. However, the rebound in the aussie will be tested if the RBA backpedals on its tapering plans next week.

In the energy arena, OPEC+ agreed to stick to its plans to steadily raise output. Oil prices fell initially after the Russian minister hinted that bigger supply increases may be on the cards, but managed to claw back most of those losses.

Finally, gold couldn’t take advantage of the pullback in the dollar this week, showing no signs of life. A potential NFP disappointment tomorrow could reawaken bullion and hurl it towards the $1835 region, but the longer-term outlook is turning darker with the Fed about to close the liquidity taps.