{kind=link}

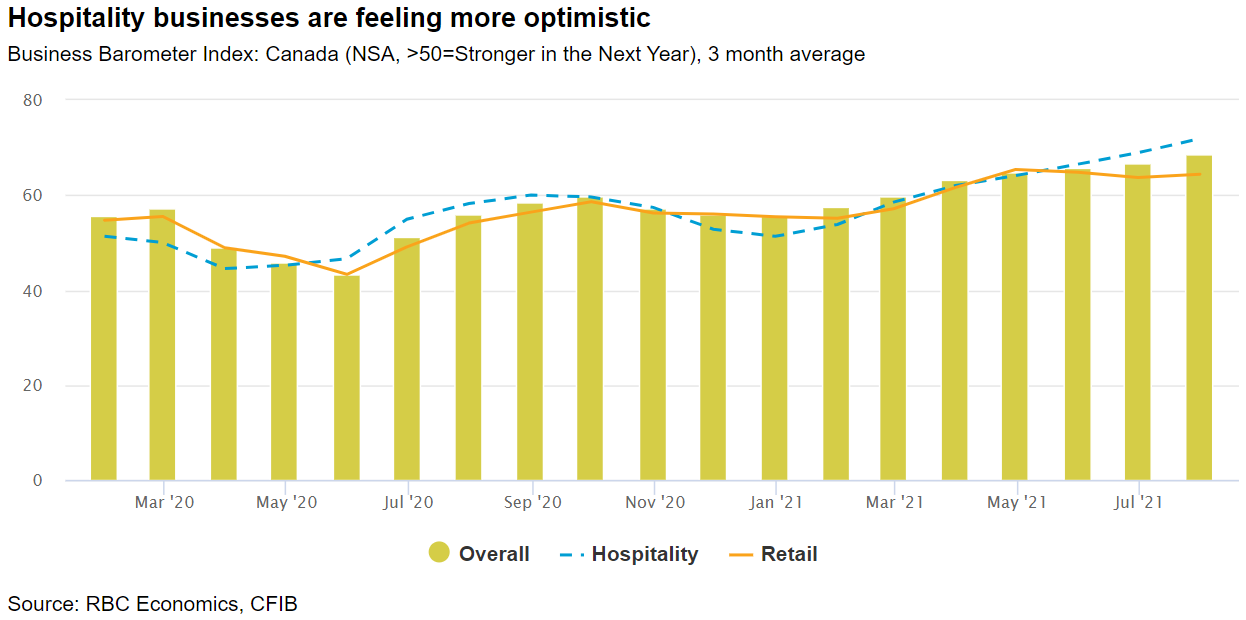

A quieter flow of economic data next week will highlight the ongoing recovery in hard-hit service sectors. Our own tracking of credit card transactions is pointing to an increase in food services sales that exceeds the 4.2% rebound in retail sales in June. And stronger gains likely took place in July as the economy emerged from spring lockdowns. The latest installment of the Canadian Survey on Business Conditions (based on responses collected from July 2 to August 6) should provide more optimism, including for badly-bruised travel and hospitality sectors. Still, even as business revenues pick up, firms will continue to raise concerns about rising input prices, supply chain disruptions, and persistent labour shortages. The Bank of Canada’s Q2 Business Outlook Survey showed that nearly half of firms expect labour shortfalls to intensify in the coming months. If this materializes, many companies may reach their capacity limits a lot sooner.

Notwithstanding recent improvements, many businesses likely remained heavily dependent on government support programs over the summer. Rising case counts have once again prompted some regions to pause reopening plans, but high levels of vaccination are expected to temper the negative health outcomes and prevent a return to widespread lockdowns. The virus remains the biggest current economic threat, but we expect the broader economic recovery to continue.

Week ahead data watch:

- The flash July Canadian manufacturing sales report is expected to build on the 2.1% rise in June despite ongoing supply chain disruptions. Hours worked in the manufacturing sector rose 3.1% in July.

- Backward-looking SEPH employment data for June will show a strong recovery driven by job growth in the hospitality and retail sectors.

- Weekly average COVID-19 case counts have doubled in the last two weeks and currently sit above 2000/day—up from an average of ~ 500/day in July.