{kind=link}

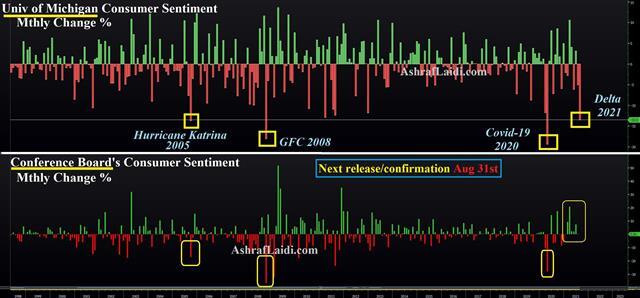

As the situation in Afghanistant accelerates from chaos to outright mass danger to human lives, focus turns to US president Biden’s imminent speech on the situation. But for now, let us weigh in Friday’s UMich consumer sentiment survey, showing the 4th biggest decline of the last 30 years. The report reminds us we’re in an unprecedented era and that predicting economic behaviour in the months ahead will be perilous. Also today, the Empire Fed manufacturing survey fell from 43 to 18.3 vs expectations of 28.5. The chart below shows the other 3 times when UMich sentiment fell by more than it did last Friday. This should raise further debate on the timing of the taper as well as upcoming sentiment surveys.

This decade so far has been completely unpredictable starting with a global pandemic followed by unprecedented stimulus leading to a remarkably quick recovery. Since then, a strong consensus has emerged that the recovery will continue with the main question about how inflationary it will be.

Friday’s UMich sentiment survey was a reminder that the consensus can be badly wrong. The survey plunged to 70.2 from 81.2 in a move no economist came close to forecasting. Shockingly, sentiment was even worse than in April 2020 at the height of the pandemic.

Many market watchers were simply in disbelief but the survey takers pointed to delta risks and reality that the grand reopening has turned into a stumble in the US as hospitalizations and cases surge. New questions about safety and schools have soured great hopes and the political situation (which the UMich survey unfortunately tracks better than consumer spending) remains bitterly polarized.

Is the optimism misplaced? Probably not. Kids are at threat to delta but the numbers with serious illness are staggeringly low. In Europe, the Stoxx 600 rose for 10 straight days through Friday. The recovery may unfold more slowly and covid will remain a risk for years but consumer and business balance sheets are strong.

The numbers will give the Fed some pause and that diminishes the chance of a September taper or a quick taper once it starts. Because of that, selling the dollar was the right reaction for now.

With regards to Afghanistan, any sort of US military resurgence into the country is unlikely to weigh on markets. But if persistent news of escalating US hospitalisations and school closures emerge from the Delta variant, then this is likely to bring up other variables as a valid catalyst for risk-off, namely the Fed taper and Afghanistan.