{kind=link}

The US dollar is just reeling from unexpectedly weak consumer sentiment data but there could be more trouble on the way as retail sales numbers due Tuesday (12:30 GMT) are not anticipated to impress. However, none of that may matter if there are further hawkish soundbites coming from the Fed’s way when Chair Jerome Powell speaks on Tuesday (17:30 GMT) and the July FOMC minutes are published on Wednesday (18:00 GMT).

Will there be another hawkish lean by the Fed?

It’s proving to be a bit of a rollercoaster summer for the greenback even if the broader trajectory for the currency is an upward one. Fed speakers have been out in droves lately, making the case for a reduction in the US central bank’s massive monthly dose of asset purchases. The change in tone follows a series of strong labour market indicators that took the Fed several steps closer to achieving “substantial further progress” towards its goals.

However, investors have yet to hear from Powell after the last unquestionably solid NFP report so any remarks on the economy on Tuesday will be heeded by the markets. Similarly, the minutes of the July meeting are expected to disclose more detail about how much taper discussions have progressed. After the recent run of upbeat US data and Fed views, it would be far too easy to assume that a further hawkish shift is in order this week. But the constantly evolving virus landscape means the Fed isn’t about to throw caution to the wind just yet.

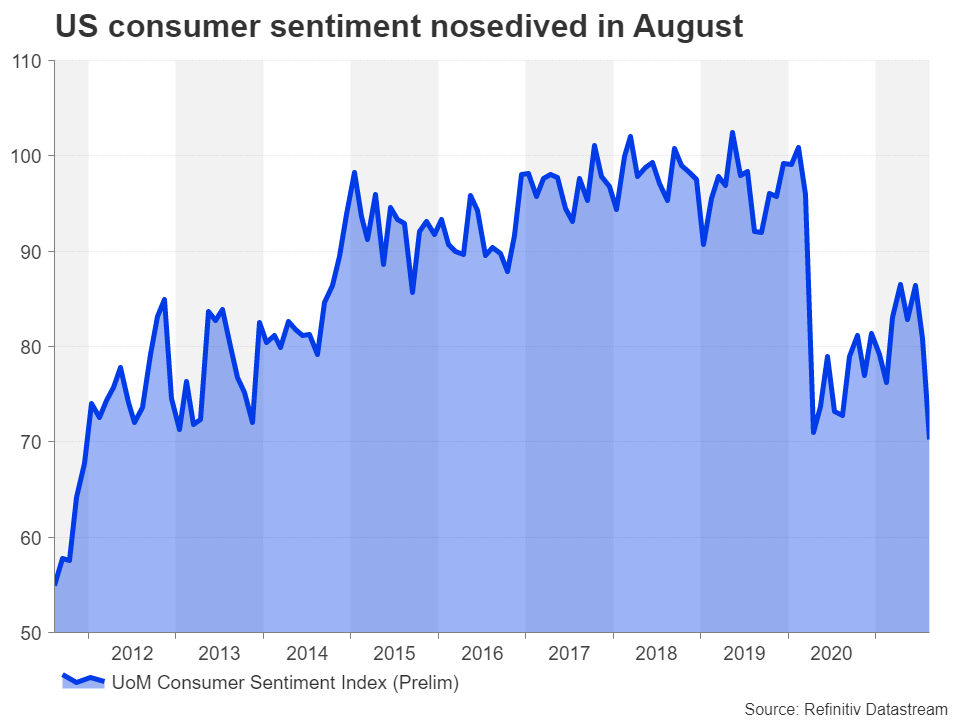

Plunge in consumer confidence muddies the outlook

The drop in the University of Michigan’s closely watched consumer sentiment gauge to a post-pandemic low in August is a stark reminder that the Covid nightmare is far from over. The Delta-led surge in US infections appears to be significantly denting confidence among consumers. Although disappointment that even with vaccines the virus threat is still present may be magnifying the downbeat sentiment.

Hence, policymakers will probably not put too much weight on the August figure, especially seeing as it’s the preliminary reading and might get revised higher. The same can be said for the July CPI print, which raised hopes that the spike in inflation may be easing. However, these ‘outliers’ in the data in an otherwise improving trend may bolster the argument for the Fed doves who are maintaining their stance that they’d like to see “a few more” strong jobs reports before making a decision on tapering. Powell likely falls within this camp and there’s a good chance he will push for an end-of-year move than a September one, which the hawks are calling for.

Retail sales data may help the doves

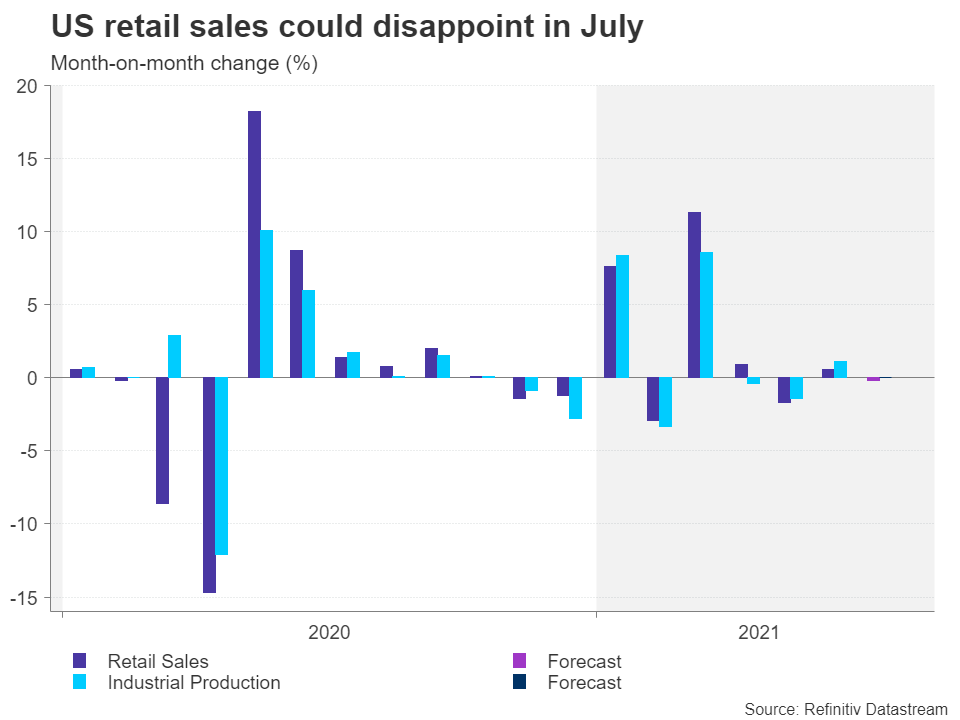

If the upcoming retail sales figures underwhelm, it will add to the number of reasons for the Fed to stay overly cautious a while longer. Retail sales are expected to have fallen by 0.2% month-on-month in July after rising by 0.6% in the prior period. The control group of retail sales, which is an alternative core measure that excludes automobiles, gasoline, building materials and restaurants and tracks GDP much more closely, is forecast to have stayed unchanged.

Industrial production readings due later in the day at 13:15 GMT is anticipated to be more positive, growing by 0.5% m/m in July.

Strong obstacles for dollar advances

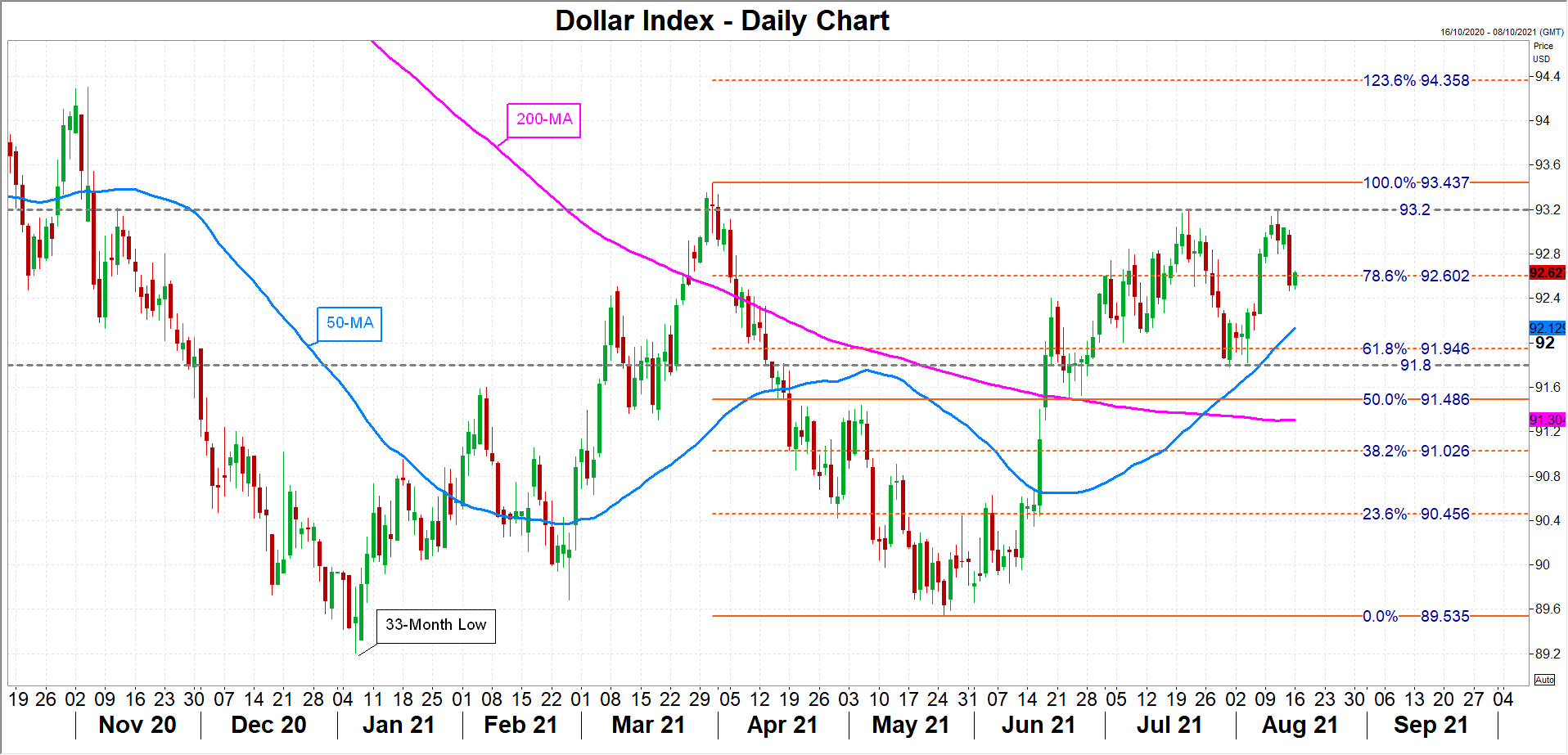

Nevertheless, while the data releases are bound to bring some volatility to the dollar, it will be the message coming from Powell and the minutes that ultimately decide its fate this week and possibly until the Jackson Hole conference next week. The dollar index has formed a short-term trading range between 91.80 and 93.20, with the 93 handle proving quite challenging to reclaim. If Powell or the minutes hint that a September taper announcement is more likely than a delay, the dollar index might just be able to power through this resistance area and make a push towards the March 31 peak of 93.44.

However, should Powell & Co fail to send clear signals this week and the minutes underscore the divisions within the Fed, the dollar index could slip towards its 50-day moving average, currently at 91.13, taking it closer to the bottom of the range. Breaching the recent troughs around 91.80 would pave the way for the 50% Fibonacci retracement of the March-May downtrend at 91.49.