{kind=link}

- Dollar off highs but elevated after strong NFP puts September taper back on the table

- Gold plunges below $1,700 before rebounding as yields spike, but oil’s rout deepens

- Stocks undaunted by prospect of earlier Fed tapering as Wall Street sets new records

Taper speculation heats up after bumper US jobs report

Markets were left wondering just how much progress is substantial after the US labour market added another 943k jobs in July, while upward revisions to both the May and June numbers further fuelled speculation that the Fed is close to meeting its employment criteria for pulling back some of its stimulus.

The Fed has been adamant that it cannot make a decision on tapering until it has seen “substantial further progress” in the recovery, and in particular, in the jobs market. But after the recent rough patch, Friday’s blowout NFP report has left few doubting that the jobs rebound is on a solid footing again. The question is, will another month of strong jobs data be enough for the Fed to announce its taper plans in September, or will policymakers want to wait until November or December before reaching a decision?

If it wasn’t for the worrying uptick in US Covid infections and hospitalizations, a September announcement preceded by a taper signal in Jackson Hole would probably be seen as a done deal. However, the Delta variant may yet put a spanner in the works if the reopening of the economy is put on hold or even reversed in the coming weeks.

Opinions are clearly divided at the Fed with some FOMC members pushing for earlier tapering but a resurgence in virus cases could bolster the doves. Speeches coming up later today by Bostic and Barkin, and by Evans and George later in the week should shed more light as to which way they’ve been swayed by the July report.

Dollar and yields cool after Friday’s rally

In the immediate aftermath though, markets are leaning towards a September taper move and investors are also more confident about the first post-pandemic rate hike arriving in late 2022. Treasury yields have surged on the back of those shifting expectations. The US 10-year yield topped 1.30% on Friday before falling back slightly.

Nevertheless, long-term Treasury yields remain far below their peaks from earlier in the year, underlining how investors have steadily been unwinding their bets of a swift end to the pandemic. Growing expectations that Covid-19 will hinder economic activity for years to come even with vaccines in the picture have led investors to downgrade their more bullish outlooks. The latest consensus that seems to be emerging is that even if central banks are forced to raise rates sooner than expected because of spiralling inflation, they won’t rise much after that because the growth won’t be there.

This may not necessarily be bad news for the US dollar if the American economy is still outperforming all its peers. But in the short term at least, the greenback’s gains were more pronounced against currencies whose economies are not expected to fare as well.

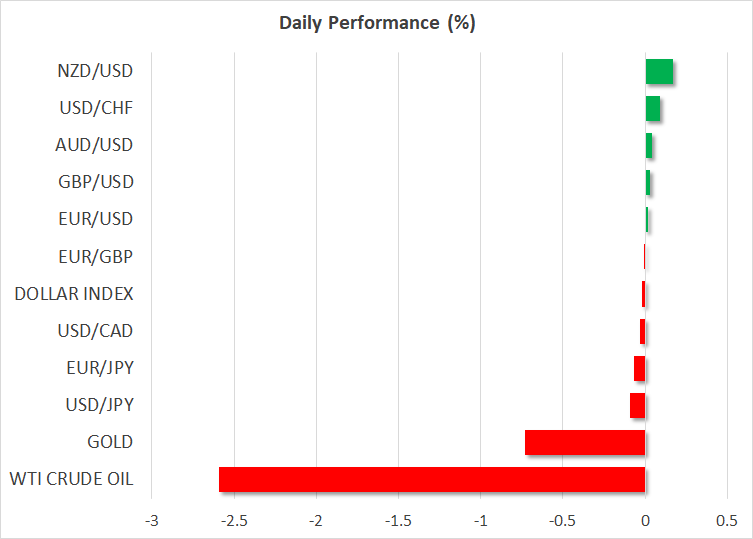

The euro slumped below $1.18 as the NFP data further widened the monetary policy divergence between the Fed and the ECB. The aussie slid below $0.74 as Australia’s lockdown woes continue to worsen. But the pound and loonie suffered only limited losses, with both the Bank of England and Bank of Canada on track to end their bond purchases in the coming months.

The dollar index climbed to a two-week high of 92.92 earlier today, extending Friday’s advances before settling slightly lower.

Gold and oil on the backfoot

In commodities, gold was desperately trying to halt its freefall after crashing to a 4-month low of $1684.37/oz at the start of Monday trading as the spike in Treasury yields triggered a global jump in sovereign bond yields. But the spot price managed to bounce back to around $1,745/oz when European markets opened. Still, the precious metal’s outlook has been severely dented after the Friday jobs report and there may be further selloffs to come.

It hasn’t been a particularly good start to the week for oil either, whose week-long slide just got worse. WTI and Brent crude futures were both down more than 3.5% amid renewed concerns about oil demand.

Fresh travel restrictions in China have added to oil’s downside as the Delta variant continues to delay the full lifting of virus-related curbs in most countries.

No taper panic in equity markets

However, despite all the volatility, things were pretty calm in equity markets on Monday. Asian stocks ended the session mostly higher, aided by fresh record highs on Wall Street on Friday. The Dow Jones and S&P 500 closed at all-time highs as traditional stocks were boosted by the encouraging jobs data even though higher yields dragged the tech-heavy Nasdaq Composite lower.

But Nasdaq futures were pointing to a slight rebound today, while Dow Jones and S&P 500 futures were marginally in the red. Aside from the upbeat NFP print, a robust earnings season is also supporting US stocks, with signs that Congress is edging closer to passing the $1 trillion bi-partisan infrastructure bill likely buoying sentiment as well.