{kind=link}

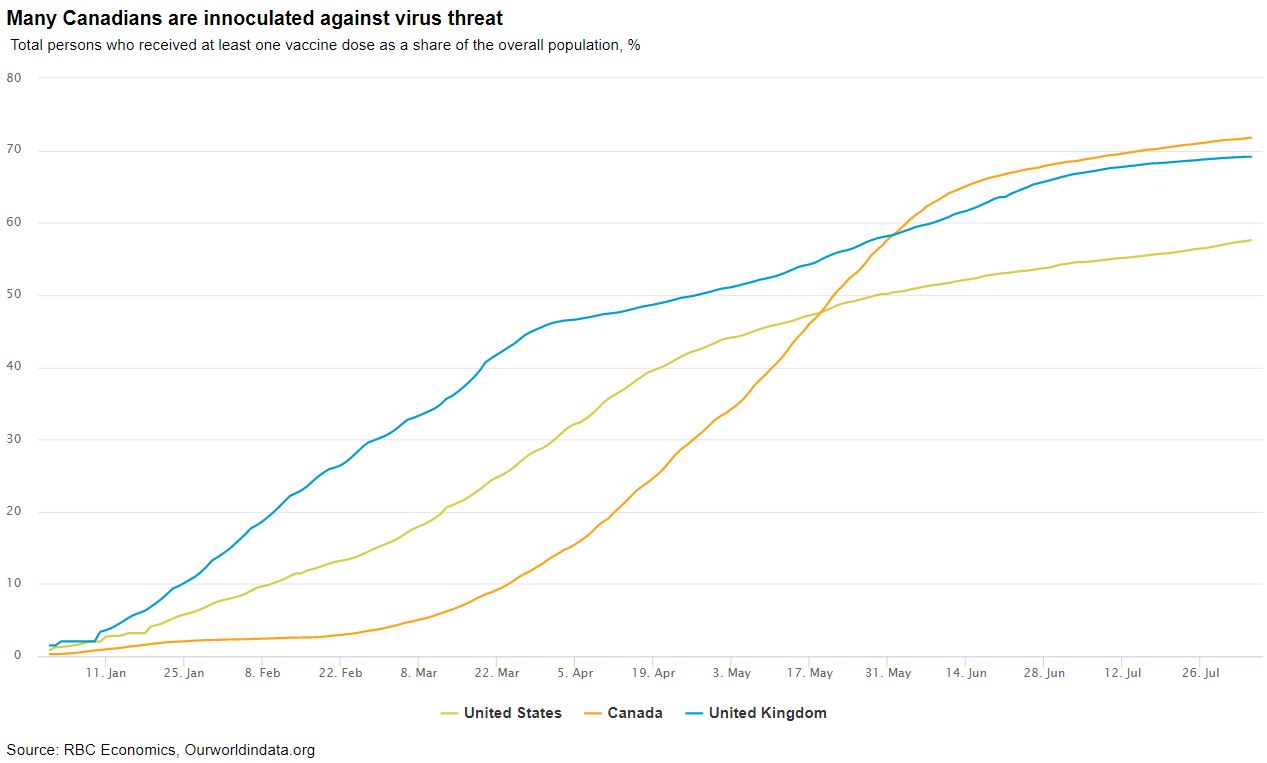

The recovery of the hospitality sector is progressing largely as expected. Businesses that were once shuttered are reopening, and green shoots have emerged. Our own data on card transactions shows spending on hospitality returned to pre-Covid (2019) levels in July as Candians ventured outside their homes. Next week Canada will take another step in the reopening process by opening its borders to fully vaccinated U.S. residents. There’s a growing concern that the rise of the delta variant could stall progress, particularly in parts of the U.S. where vaccination rates are low. Still, with over 80% of eligible Canadians at least partially vaccinated, another round of domestic lockdowns looks less likely – and much of the travel/tourism recovery to date has been driven by domestic tourists. Provided vaccines remain effective at protecting against new strains of the virus we expect a more sustained economic reopening over the remainder of this year.

The bigger concern is whether strong demand will fuel further price increases. We expect next week’s US CPI report to show the inflation rate held steady at 5.4% in July. To date, much of that increase can be attributed to ‘base effects’ – as prices for products like energy, clothing, and airfares bounced back after falling sharply this time last year – and supply constraints that have sent used vehicle prices soaring. Early evidence shows that price pressures have retreated from lofty highs – lumber prices have eased and the wholesale price of used cars appears to have peaked. As businesses iron out supply chain bottlenecks, we continue to expect that price pressures will recede over the coming months. Central bankers will continue to look through transitory price jumps and keep a close eye on underlying broad-based price growth.

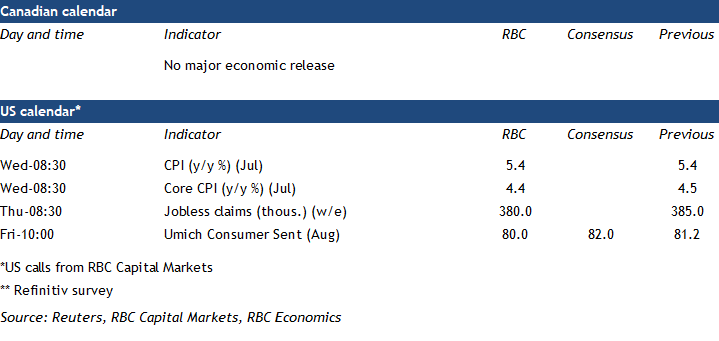

Week ahead data watch:

- Canada’s covid cases have edged up slightly over the past two weeks. A relatively high level of vaccinations is expected to limit the pass-through to hospitalizations in contrast to previous waves.