{kind=link}

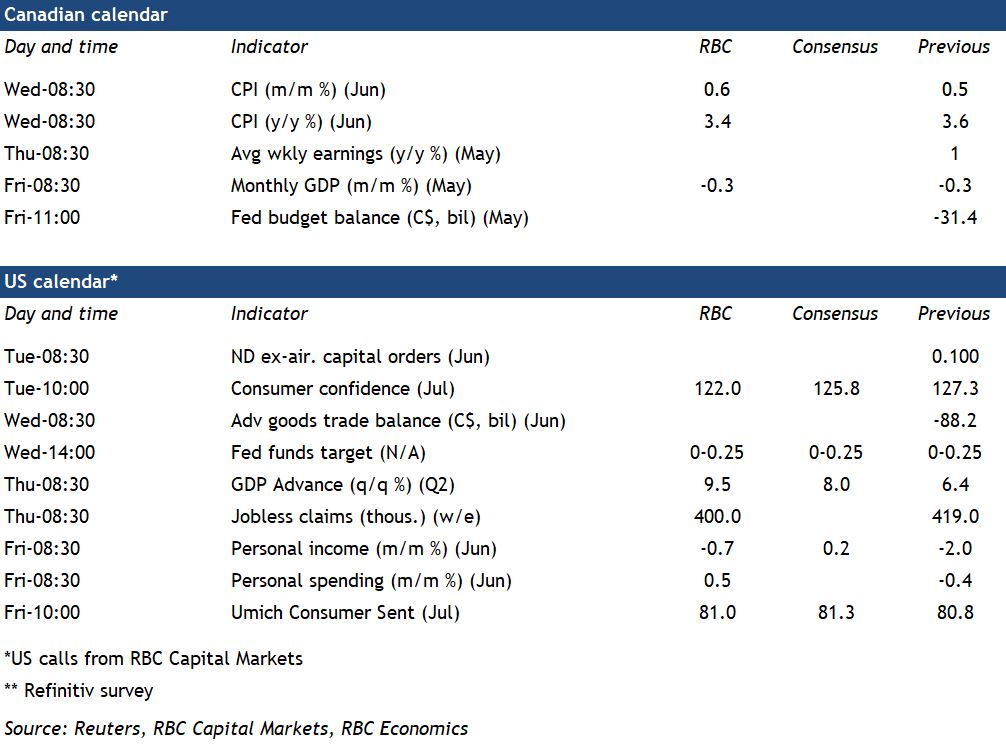

We expect next week’s June consumer price inflation report to show the inflation rate held above the Bank of Canada’s 1% to 3% target range—for the third consecutive month. There was likely a slight moderation in the annual increase in June, to 3.4% from 3.6% in May. That was probably driven by gasoline price growth that slowed to 33% in June from 43% in May and 62% in April. Much of the surge in inflation reflects base effects, as prices (including energy) rebound after falling sharply during the initial pandemic shock in Q2 2020. Though supply chain bottlenecks continue to push prices up for things like car rentals and home building, we look for some price pressures to ease in coming months as real-estate markets cool, lumber price futures fall, and global chip makers work hard to boost production.

Still, even if the inflationary impact of near-term supply disruptions fades, consumer demand, particularly for services, is set to surge over the second half of 2021. Consumers are poised to spend more on travel and hospitality sectors as the economy reopens. A sharp strengthening in that demand could stoke a more broad-based inflation that would be difficult for central banks to dismiss. Statistics Canada’s reweighting of the CPI basket to reflect 2020 household spending patterns means that for some products, like airfare and travel tours, the shares were so small last year that prices were almost removed from the CPI altogether. As a result, any inflation generated as those hardest-hit sectors rebound will be significantly underrepresented in the consumer price index in the near term. It also means that headline CPI readings won’t necessarily reflect actual household spending patterns as the year progresses, making alternative inflation measures like the BoC’s preferred ‘core’ measures—which control (to varying degrees) for larger swings in prices for individual products—a better indication of price pressures.

Week ahead data watch:

- We expect Friday’s May GDP report to confirm Statscan’s preliminary estimate of a second straight 0.3% drop, with the early read on June output likely to show an increase that retraced all of the decline in the two prior months.

- As the economic reopening gets going, we expect US GDP to grow by 9.5% in Q2 driven by exceptionally strong consumer spending for the quarter. We look for US personal income to fall by 0.7% in June following a combined 14.8% drop in the prior two months as pandemic-related assistance continues to taper off.

- The Federal Reserve will likely maintain its policy rate at next week’s meeting. Markets will watch for any hints about plans to taper their asset purchases program.

- Canada’s COVID case counts remain low but have edged higher, on balance, in recent days and infections are rising in several advanced countries. Canada continues to lead in the percentage of the population receiving one dose and the share of fully vaccinated Canadians now surpasses the US.