{kind=link}

US stocks rebounded on Tuesday after having their worst trading day on Monday. The Dow Jones rose by more than 550 points while the Nasdaq 100 and S&P 500 rose by more than 1.5%. These gains narrowed in the futures market after Netflix released weak numbers. The company lost 430,000 customers in the US and Canada in Q2. Analysts were expecting the company would add 5.9 million new customers in the quarter. In its guidance, the company said that it would add more than 3.5m members in the third quarter. In the earnings call, the firm dismissed the idea that competition from companies like Disney and AT&T were behind the disappointing results.

The price of crude oil stabilised after it declined sharply on Monday. The price of Brent and West Texas Intermediate (WTI) are trading at $68.90 and $66.73, respectively. This is almost 10% below their highest level this year. The decline happened after Saudi Arabia and its OPEC+ allies agreed to gradually increase production to take advantage of higher prices. The news coincided with the reportedly rising number of Delta variant cases in countries like Australia, US, and the UK. Some of these countries have even started adding travel restrictions to curb the spread. Meanwhile, data published yesterday by the American Petroleum Institute (API) showed that the number of inventories increased by 806k barrels last week. Analysts were expecting a drawdown of more than 4.16 million barrels. The EIA will publish its official numbers today.

The US dollar retreated slightly as worries of the Delta variant subsided. The currency also reacted to the latest building permits and housing starts numbers. The data showed that the number of building permits declined from more than 1.683 million in May to 1.59 million in June. This decline was worse than the median estimate of 1.70 million. Housing starts, on the other hand, rose from 1.545 million to 1.64 million. Later today, the top numbers to watch will be the US mortgage data and South African inflation numbers. The earning season will continue, with companies like Johnson & Johnson, Harley-Davidson, and Coca-Cola expected to publish.

XBRUSD

The XBRUSD pair stabilised at the 69.00 level, which was close to this week’s low of 67.69. The price is also slightly below the neckline of the double-top pattern at 72.68. On the four-hour chart, it has moved below the 25-day and 15-day moving average while the commodity channel index (CCI) has moved from the oversold level. The pair has also formed a bearish flag pattern. Therefore, there is a possibility that it will resume the downward trend ahead of the US inventories data.

EURUSD

The EURUSD pair remained in consolidation mode as traders focused on the upcoming ECB decision. The pair is trading at 1.1770, which is close to the lowest level this week. It moved below the 25-day moving average and is still inside the descending channel. The Relative Strength Index (RSI) and the MACD are also neutral. Therefore, the pair will likely remain inside this range ahead of the ECB.

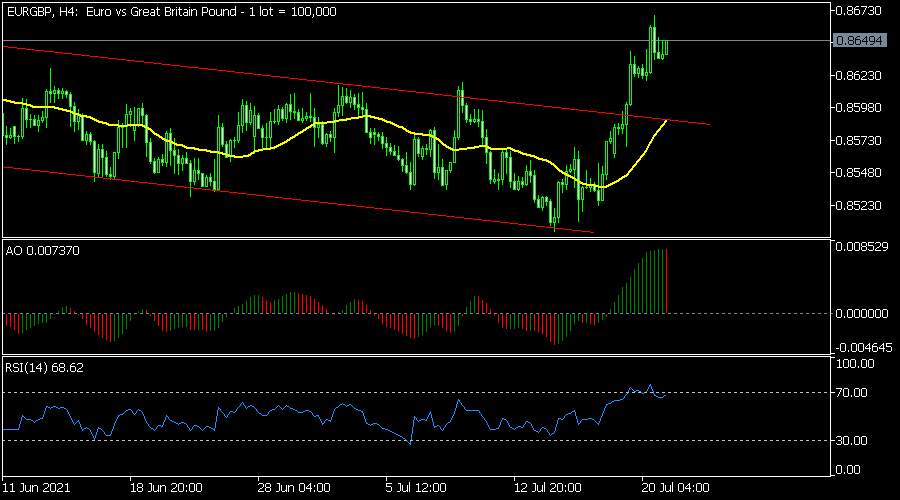

EURGBP

The EURGBP pair rose to a multi-week high of 0.8670 as the UK reopened. On the four-hour chart, the pair managed to move above the upper side of the descending channel shown in red. The pair also moved above the 25-day moving average while the MACD has moved above the neutral level. The pair will likely keep rising, with the next key resistance being at 0.8700.