{kind=link}

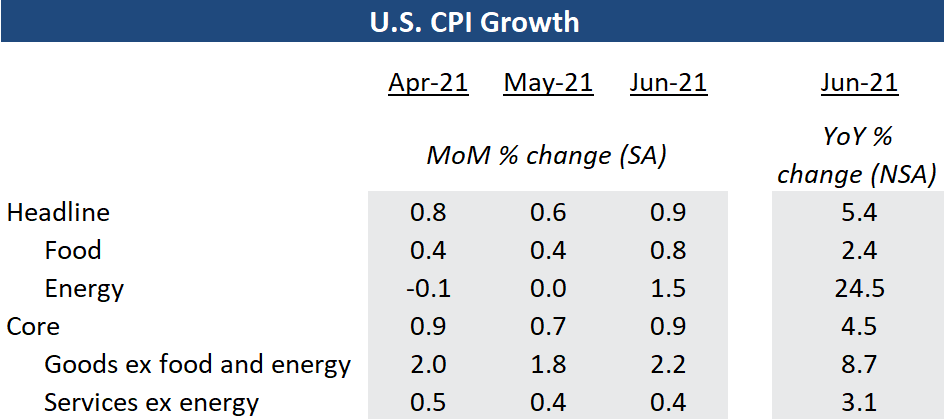

Headline inflation up 5.4% in June from year-ago and core (ex-food and energy) up 4.5%

Base effects continue to be at play; transportation related prices surged again

Price gain still relatively narrowly based; more guidance on tapering from Fed in August

US headline inflation in June beat consensus estimates for the third month in a row, posting a 5.4% year over year increase, or 0.9% from May. ‘Base-effects’ still account for much of the rise – energy prices were up 24.5% in June versus very low year ago levels, although that pace was slightly slower than the April and May increases. Prices for used cars and trucks also rose sharply again, accounting for a third of the month over month gain.

Travel demand in the US, by road and air, bounced back more quickly than expected as virus containment measures eased. Passenger volume on inter-state highways rose to pre-pandemic levels by early June, and TSA throughput showed air travel back at over 85% of pre-pandemic levels as of last week. That’s all leading to a surge in prices for transportation related goods and services beyond just higher gasoline prices. Airfares, despite still below pre-pandemic levels have made big gains recently, and prices for used cars and car rentals have surged around 40% and 70%, respectively, ahead of pre-pandemic levels.

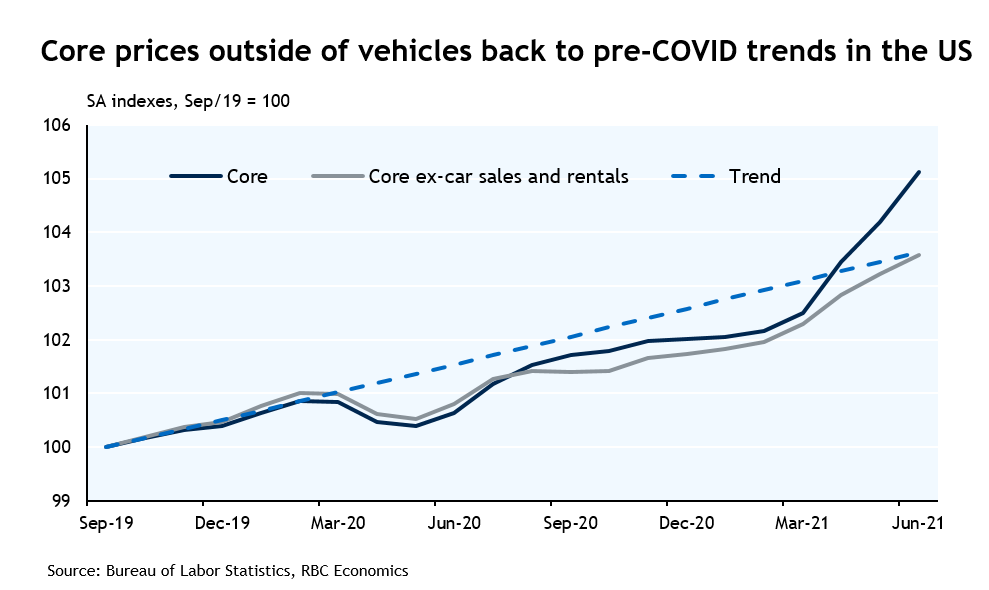

Indeed, vehicle prices accounted for more than half of the 4.5% year-over-year ‘core’ (ex-food & energy) price gain in June. Excluding those, the core index is only now catching up to pre-pandemic trend levels. The fact that price growth has not been particularly broadly-based is why Federal Reserve policymakers will probably continue to look through firmer headline CPI growth as ‘transitory’ for now. In the meantime, a stronger footing of the economic rebound is more likely to be what had prompted the Fed to start early discussion on tapering, with further guidance possibly coming at the Jackson Hole gathering next month. Market based inflation measures ticked up slightly this morning after the CPI release.