{kind=link}

There’s been a massive shift within the central bank world lately. Some have taken baby steps towards exiting cheap money and ultimately raising interest rates, but others have not. We seem to be entering a period where the economies that will be raising rates might see their currencies appreciate against those that won’t. The dollar, pound, kiwi, and loonie could shine, whereas the yen, franc, and euro may fall behind.

Fuel on the fire

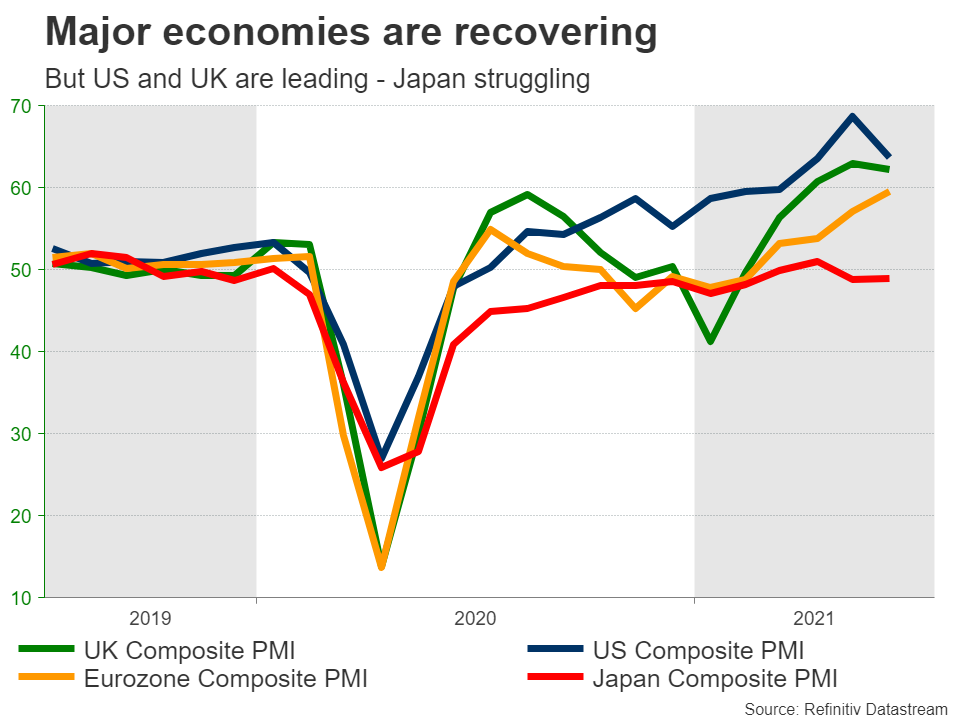

One year after the world economy almost collapsed, things are looking much better in many countries, so much so that some central banks are ready to take their foot off the accelerator. Tremendous government spending and infinite liquidity for the financial system seem to have worked wonders in preventing any lasting damage from the crisis.

It is now clear that the pandemic was mainly a supply shock, which was handled like a demand crisis. When an economy is facing production problems but the government keeps spending with force, the supply side can’t cope. The result is a booming economy, but at the cost of rising inflation.

It’s like pouring fuel on the fire. It risks overheating the economy. As such, some central banks are now trying to slowly exit their crisis-era programs to keep inflation under control. It’s better to step on the brakes gently now, than having to pull the handbrake later on.

But it’s not all central banks. Some are faced with economies that are still struggling, so they won’t be exiting cheap money anytime soon. This sets the stage for some powerful FX trends moving forward.

Carry trade

Higher interest rates are naturally beneficial for a currency. Investors can borrow in a low-yielding currency and then invest that money in higher-yielding assets abroad, earning a return on the difference and boosting demand for the high-yielding currency. This is called a carry trade.

When investors sense that a central bank will be raising rates down the road, they usually try to front-run this trade by buying that currency, expecting it will appreciate later on.

So who is raising rates?

In a nutshell, of particular interest for FX traders is that the central banks of America, Canada, the UK, and New Zealand have all taken the first steps towards normalizing rates. The markets think the Reserve Bank of New Zealand will act first, currently pricing in an 80% chance for a rate increase in November this year, with another one to follow by spring 2022.

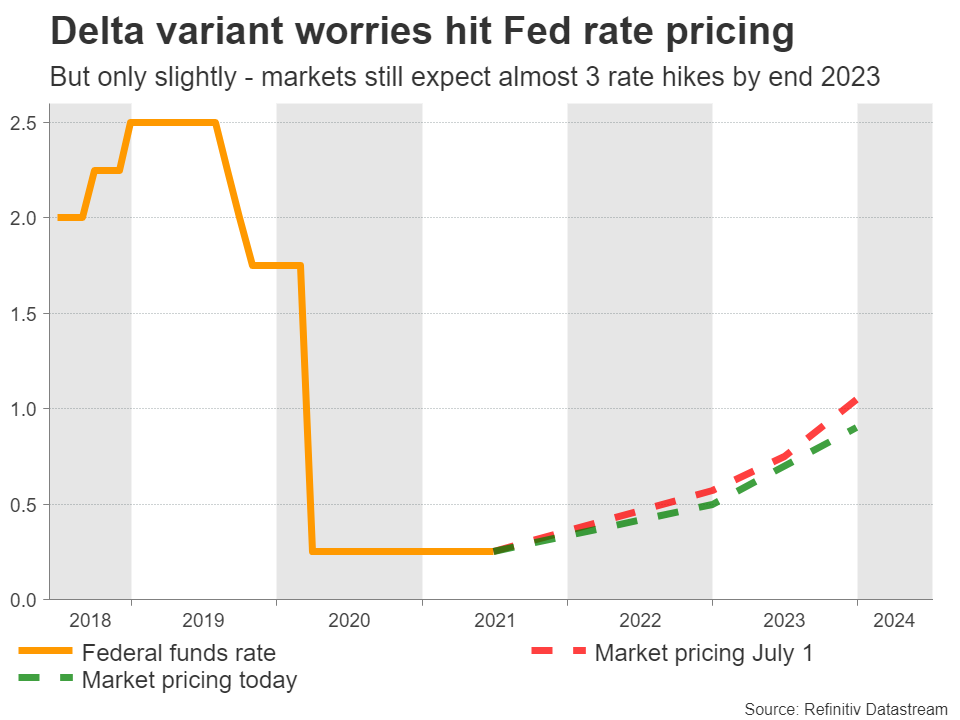

In America, the Fed is widely expected to announce that it will scale back its enormous asset purchase program in the coming months, which would be the first step towards higher rates. The first rate increase is priced in for December 2022, with almost another two in 2023. This pricing took a hit lately due to worries around the Delta variant, but not dramatically.

The Bank of England is a similar story, along with the Bank of Canada.

Who isn’t normalizing?

The Eurozone, Japan, and Switzerland won’t be raising rates anytime soon. Japan and Switzerland are still trapped in a low inflation regime and economic growth is far from impressive.

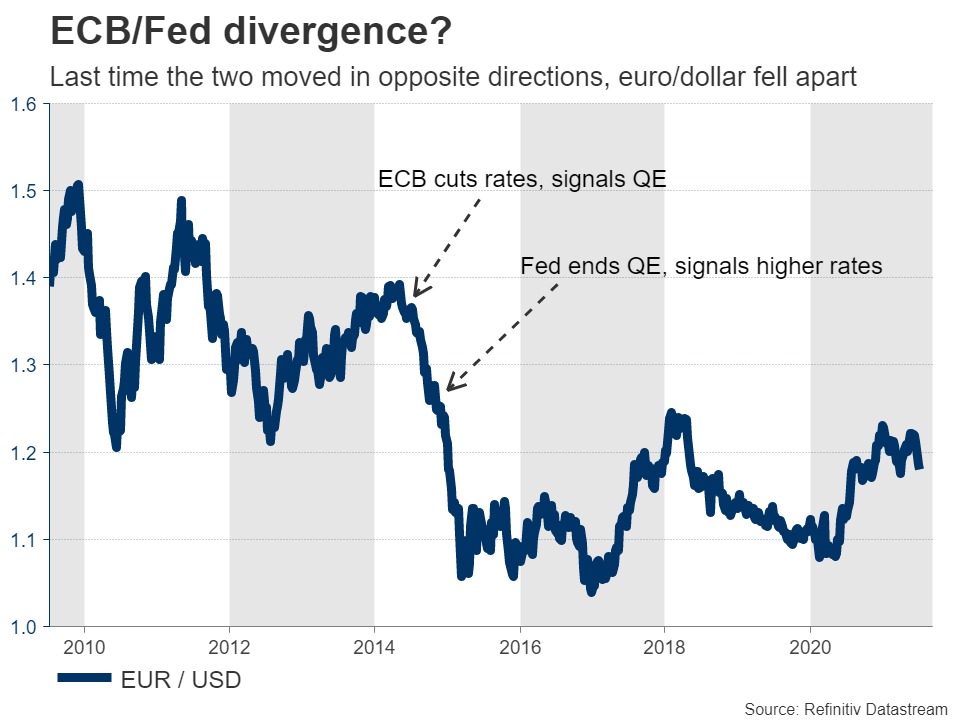

Europe is doing better so the European Central Bank might ultimately dial back its asset purchases, but it won’t raise rates for several years. The economy is just not that strong. In fact, the ECB recently raised its inflation target, essentially committing to negative interest rates for a longer period of time.

Winners and losers

Adding everything together, the currencies of nations that will enjoy higher interest rates are likely to outperform those that won’t be raising rates over the coming years.

Specifically, this implies that the US dollar, British pound, Canadian dollar, and New Zealand dollar might shine against the Japanese yen, Swiss franc, and to a lesser extent the euro. Pairs like dollar/yen or pound/franc could head higher over time as this theme crystallizes.

What’s the risk?

The main risk to this view would be some shock that hits global markets. For example, a new covid mutation that the vaccines are not effective against, which sees lockdowns return. That could slow down the pace of normalization in many countries, and also boost both the yen and the franc through safe-haven demand.

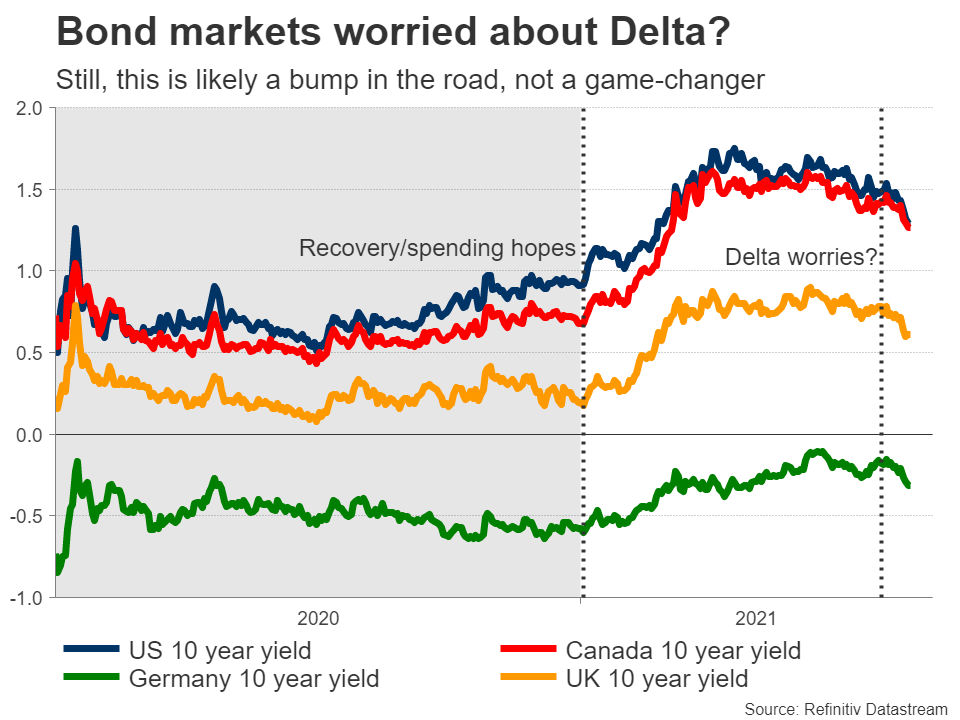

In fact, we have already seen this play out this week. Concerns around the Delta covid variant have seen rates decline as investors started pricing in a slower normalization path by the major central banks, boosting the yen and the franc in the process.

But ultimately, this is unlikely to last long. The Delta variant might slow down this trend, but it won’t derail it. It is mainly an issue for emerging markets, not the advanced economies that are mostly vaccinated already. It will take something much bigger to demolish the narrative of monetary policy normalization.